Make no mistake, commodity prices are still years from the bottom. Fundamentals are terrible in most, and getting worse in the case of Australia’s crucial bulks and gas, but none of that matters today. The Fed is on hold and the Pavlovian response is to buy dirt.

We saw this earlier this year when the Mining GFC knocked the Fed back and accompanying it was a monstrous mining bear market rally. We’re running an echo episode now with iron ore futures through the roof, base metals flying and oil pouring it on above $50. Let’s run through the charts. The US dollar was soft:

Even so, yen and euro were weak:

Advertisement

Commodity currencies launched, the Aussie the least of it:

Gold held its gains:

Oil hit new highs:

Advertisement

Base metals jumped:

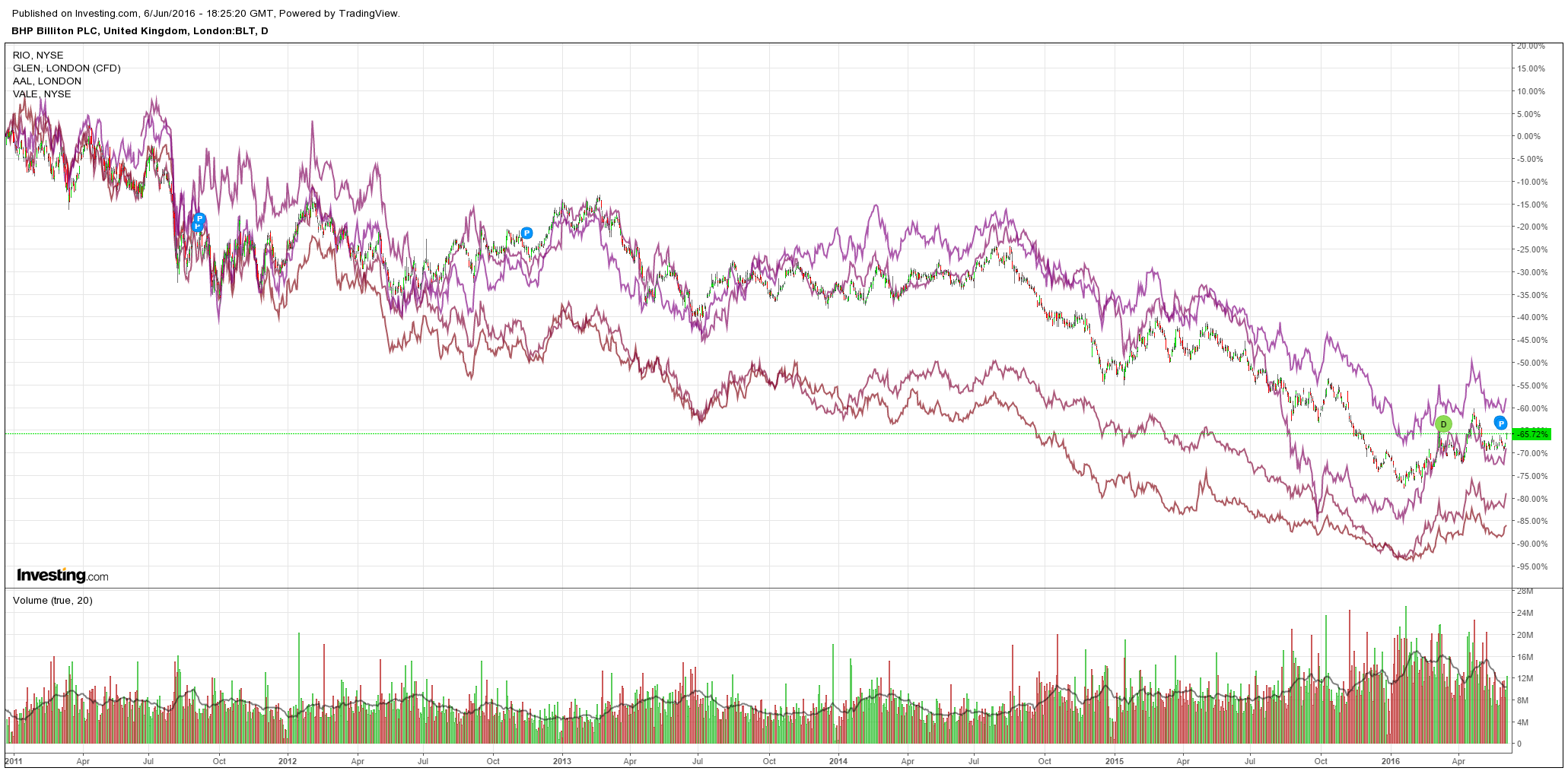

Big miners too:

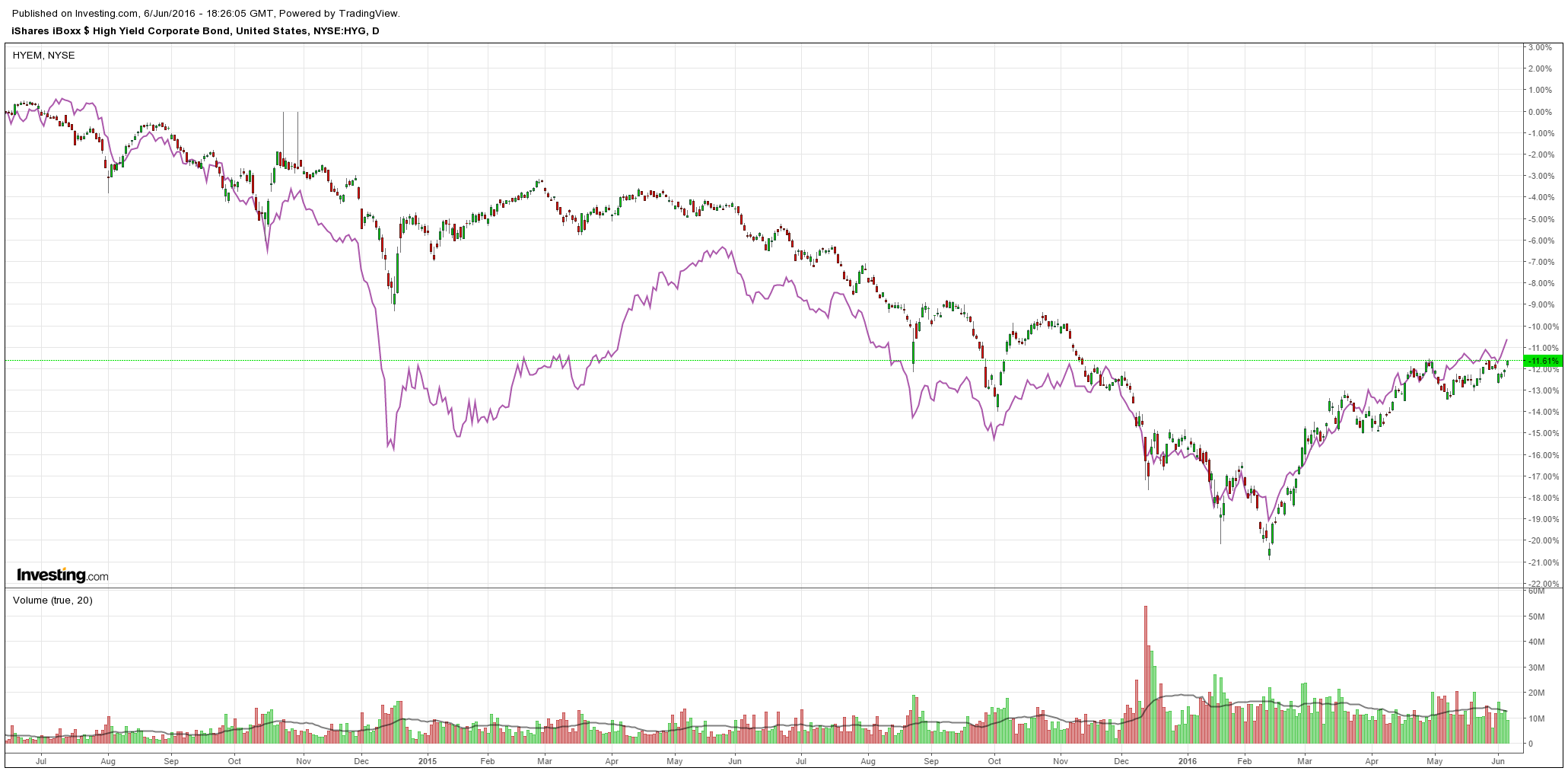

EM high yield broke out and US is poised to follow:

Advertisement

For now the Mining GFC is over. As I say, the fundamentals are still weak but let’s not confuse that with the reality of markets. In today’s market milieu, Fed tightening is bullish but Fed not-tightening is wildly bullish. Stocks and bonds are both breaking higher.

I can’t see this commodity reflation getting terribly far. The world does not need more dirt and China is going to slow through H2. As well, the US dollar can’t fall far with all other major currencies in much worse shape.

Advertisement

That said, I can’t see it falling much, either. With the Fed now on the sidelines for the rest of the year, the US dollar is not going to rise. The Fed is not going to ease barring some shock like Brexit but all commodities have become gold, that is the automatic undollar, even dirt as abundant as iron ore, so financialisation will support them regardless of underlying demand.

Oil was always the key to the Mining GFC thesis – that the commodity rout was big enough to destabilise global credit – but with the paused Fed pushing high yield debt up for more US shale production there is increasingly less stress. Sure, the world does not need the oil but that is secondary to the monetary pulse.

It appears that the global business cycle is itself now dead. By that I mean that any kind of cycle is dead not that this cycle is dying. I can’t see any cause for it to end any longer this year. Perhaps next if the Fed resumes tightening but a slowing China is very likely to prevent that. Even so, there’s no obvious crisis coming in China, either, if the Fed is quiescent. It’ll keep its glide slope intact with more zombie credit while the yuan can grind lower without crisis. Political risks are real in Europe around Brexit then Fraxit. Likewise in the US, a Trump Administration launching a trade war would sure rock the boat. But one can’t base an investment strategy entirely around political black swans. Quantitative failure looks like a myth when markets salivate at the tiniest hint of Fed largess.

Advertisement

So, the global business cycle will slouch on, zombie-like, refusing to clear mal-investment, making more of it, oversupplying everything, then oversupplying it some more, with more deflation then bouts of central bank liquidity. Rinse and repeat into stagdeflation.

BofAML agrees:

What perhaps the market has for now decided to overlook the following alarming statistic- during the heat of the early year selloff there were 21 important indicators. Of those 21 indicators, 16 of them are the same or worse today (Table 1). Interestingly, 3 of the indicators that are better today are related to the manufacturing sector (Factory Orders, Durable Goods and ISM Manufacturing). Personal Spending is also modestly improved (though Personal Consumption is worse) and New Home Sales is modestly improved (Existing Home Sales is much worse). With manufacturing still struggling, despite slightly better data, and a weaker consumer, we would argue that the macro landscape is as bad or worse than when investors were forecasting imminent recession (we were not in that camp).

We find it incredible that 76% of the most important economic indicators from the selloff are worse today but yields are about 200bp lower. Perhaps this suggests central bank policy will move the cycle deep into extra innings and that they are able to slow the path to a late 2017 or 2018 recession. Perhaps we’re wrong and the market this year has a healthy return as it takes a breather from what could ultimately become the most gradual global slowdown in the history of the world. Perhaps low rates spur capex investment and continued labor force gains. Perhaps corporate profits increase as consumers continue to repair their balance sheet and the best part of the cycle is just beginning.

Alternatively, perhaps the Fed overlooks this last month’s data and Chair Yellen sounds (and acts) more hawkish than pundits expect. Perhaps the British referendum results in a leave vote. Perhaps the general election this November causes market panic. Perhaps global growth wanes and the deflation/disinflation fears once again take hold. Perhaps, we awake in October with a hike in the bag, oil back to $39 and our first negative jobs print. Perhaps oil spikes and damages households. Perhaps corporate earnings fall after their decent Q1, economic growth continues its decline and the consumer begins to rein in spending.

… we continue to believe that the linkage between corporate earnings, Capex, credit conditions and labor productivity is not fully appreciated and will take many by surprise when companies begin to lay off more than they hire to save costs and try and expand equity multiples and the bottom line. We have likened this business and credit cycle to that of the late 1990s, and after Friday’s data we find yet another intriguing similarity- the pace of job growth has accelerated and decelerated nearly in concert with that period of time (Chart 1). Notice as well that in the late 1990s, corporate profits and payrolls declined roughly in tandem. In the post crisis years, however, EBITDA growth has been anemic throughout. This may suggest that the industries that are hiring (healthcare, food and service companies) are low profit, labor intensive industries.

It also may suggest that with margins high and borrowing costs low, the inevitable fall to negative payrolls may take a bit longer. In fact, we think there is a distinct possibility that we could live through a period of time when companies could even fire more than they hire without being in a recession, as consumer balance sheets are relatively healthy. In fact, without a banking crisis and housing crisis, we think the driving force behind the next leg in the economic slowdown is likely to be driven by households pulling back on spending as job security becomes an issue.Only unlike housing, which unraveled quickly, the consumer boom/bust cycle is likely to be slower and longer as the negative feedback loop of lower employment to reduced spending, reduced corporate profits, and more layoffs and liquidations may look less Fisherian than “glacierian”.

In the short term I can see a trade in stocks hitting new highs but my outlook for Aussie investors remains much the same. The Australian dollar will keep falling as commodity prices do, even if it is slower and no outright crisis comes with it. As I’ve been saying for six months and we saw yesterday, gold miners look a great pair trade with any kind of Aussie short. Australian bonds will win, win and win again as rates keep falling, at least until the next black swan confronts Australia’s current account deficit.

David Llewellyn-Smith is Chief Strategist at the MB Fund and MB Super. David is the founding publisher and editor of MacroBusiness and was the founding publisher and global economy editor of The Diplomat, the Asia Pacific’s leading geo-politics and economics portal.

He is also a former gold trader and economic commentator at The Sydney Morning Herald, The Age, the ABC and Business Spectator. He is the co-author of The Great Crash of 2008 with Ross Garnaut and was the editor of the second Garnaut Climate Change Review.