Certainly the history of capitalism has seen bigger bubbles than Australian property. There have been stranger bubbles too.

But none is more dumb.

Today there are ten reasons why you should be mulling an asset-wrecking implosion of the above over the next couple of years.

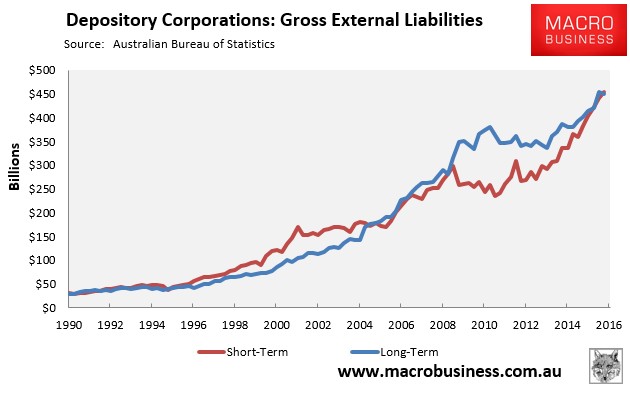

1. The dumb bubble was foreign funded and in an environment of rising international interest rates for borrowers exposed to the US and China we are seeing banks having to hike rates out of step with the RBA:

Advertisement

2. Australia is close to running out of monetary ammunition to support its bloated household balance sheet, either to grow through the accumulation of more debt or to see off another shock. 40% of the Australian private debt pile is sourced internationally adding not just local credit risk to the equation but also wider liquidity risk.

This shows that a big Australian housing short is quite possible without the RBA raising interest rates. Indeed, it is quite possible to see mortgage rates rise (or at least not fall) despite RBA cutting interest rates, if global markets get jumpy enough about commodity producers in the current global shakeout.

Advertisement

There are only 150bps of cash rate cuts left (maybe less given the CAD must be funded by some positive yield spread) and half of that will be held back by the banks, yielding households just 75bps of real easing versus 300bps in the GFC.

That will not be enough to get households borrowing again during the next global shock.

3. Australia is close to running out of fiscal ammunition.

Advertisement

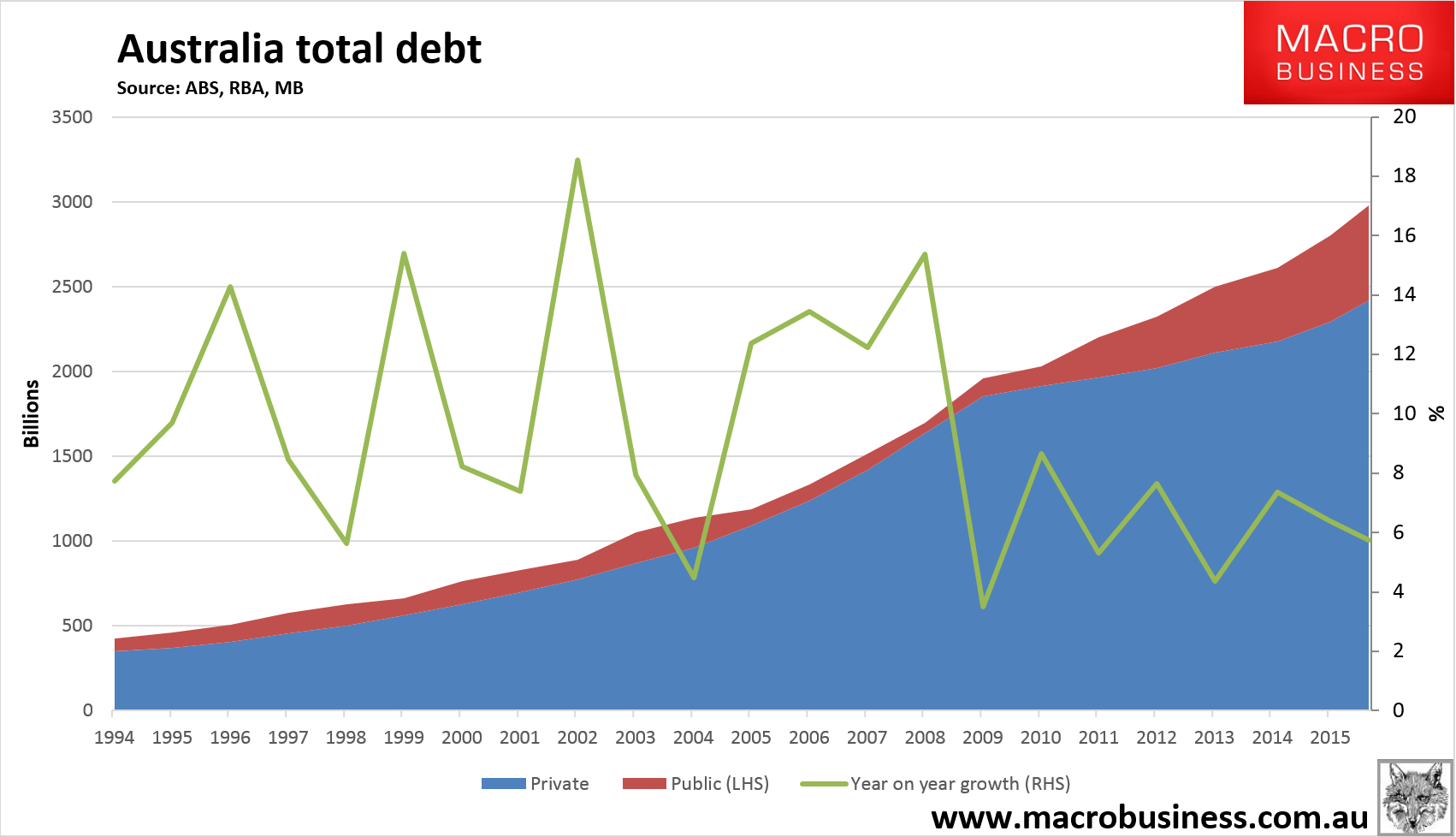

Because of the liquidity risk embedded in Australia private debt, any division between public and private debt in Australia is academic. The public guarantees the private via its offshore borrowing guarantees so it’s all one pool, really, with bank and Budget credit ratings fatally linked come what may.

Australia has dodged recession for so long because the combined total has climbed without interruption:

Advertisement

Thus, when mulling how sustainable Australian debt is one must also ask how sustainable is the Budget and the sovereign rating? The answer is not reassuring. Public debt is already growing at levels worrisome for the rating outlook. And if private debt slows then public debt will have to keep growing even faster or economic growth will stall, unless we suddenly get a surplus in the external account but that ain’t going to happen. Yet at 21% net debt to GDP (on S&P measures), fiscal policy is already stretched given 30% is the threshold for downgrades. Thus any further stimulus packages for Australia will be much smaller than the GFC effort given one good shock will be enough to send the ratio straight through the AAA ceiling unleashing all kinds of political and funding cost chaos mid-crisis.

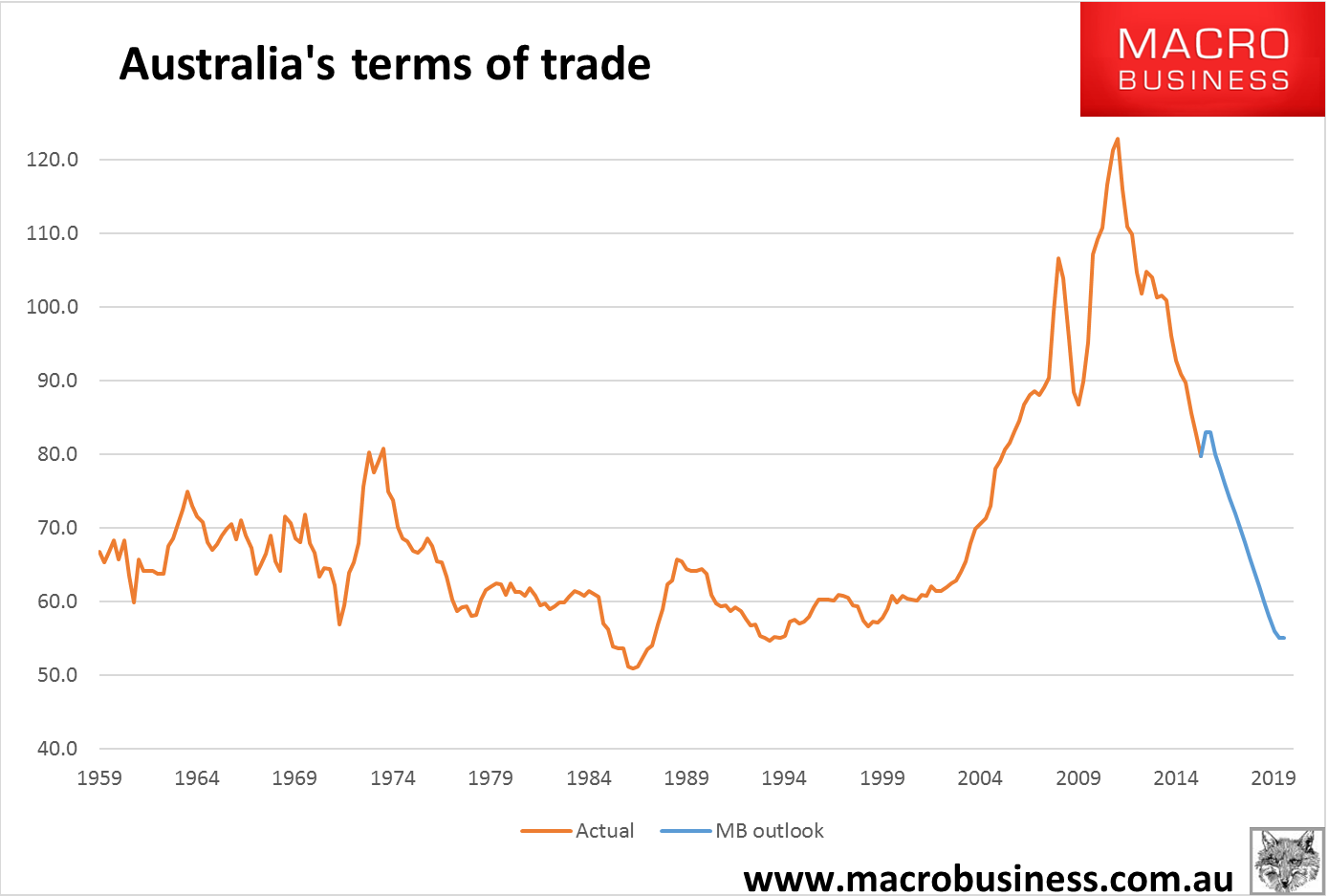

4. The commodities crash is not over. The Office of the Chief Economist (formerly BREE) announced Friday that the commodities bottom was in by upgrading its iron ore price outlook. It is horribly wrong as usual. MB sees iron ore bottoming in the teens eventually owing to massive oversupply and the ongoing deflation of the great Chinese construction boom. The same goes for coal and LNG. Thus Australia’s terms of trade will keep falling until they revert to mean:

Advertisement

That will leave Australia denuded of income growth for years yet, and continue unrelenting pressure on wages and the Budget.

5. Australia’s political economy is now a full blown facsimile of a Banana Republic so no economic reform will be pursued to prevent the imbalances worsening until they bust:

the central bank has a history of historic corruption for which there has been no public accounting and is the prime mover in the blowing of the dumb bubble rendering it unable to question it;

the fiscal executive likewise signed off on blowing the dumb bubble and is equally unable to question it;

a chronically unstable legislative executive is laughably unable to formulate good policy and it is highly questionable it even understands what it is;

there is mad rush on right now by some individuals and regulatory bodies to cover their butts by pointing to the very offending imbalances they allowed to evolve, indicating that some know things are much worse than they are letting on.

Advertisement

6. There is an unfortunate convergence of economic headwinds coming as the construction boom associated with the dumb bubble slows in concert with the ongoing mining capex cliff and the exit of the car industry. This combined capital expenditure cliff will hit services, mining and manufacturing all at once beginning in the second half of this year. It is probably not enough to bust the dumb bubble on its own given we can still lower interest rates and increase fiscal spending to ease the landing but it will render the economy chronically weak for years and exhaust the last of the stimulus ammunition over time.

7. Australia is approaching a tipping point. Some commenters on MB have recently noted that Australia’s fiscal and monetary capacity is still sufficient for one last cycle of stimulus. This is probably wrong because markets are not linear. Unlike stoned media commentators, markets shift ahead of the “time to worry”. This is speculative but it is my view that Australia is close to such a tipping point, drawn from a number of observations:

the unprecedented global debate about the sustainability of Australia debt;

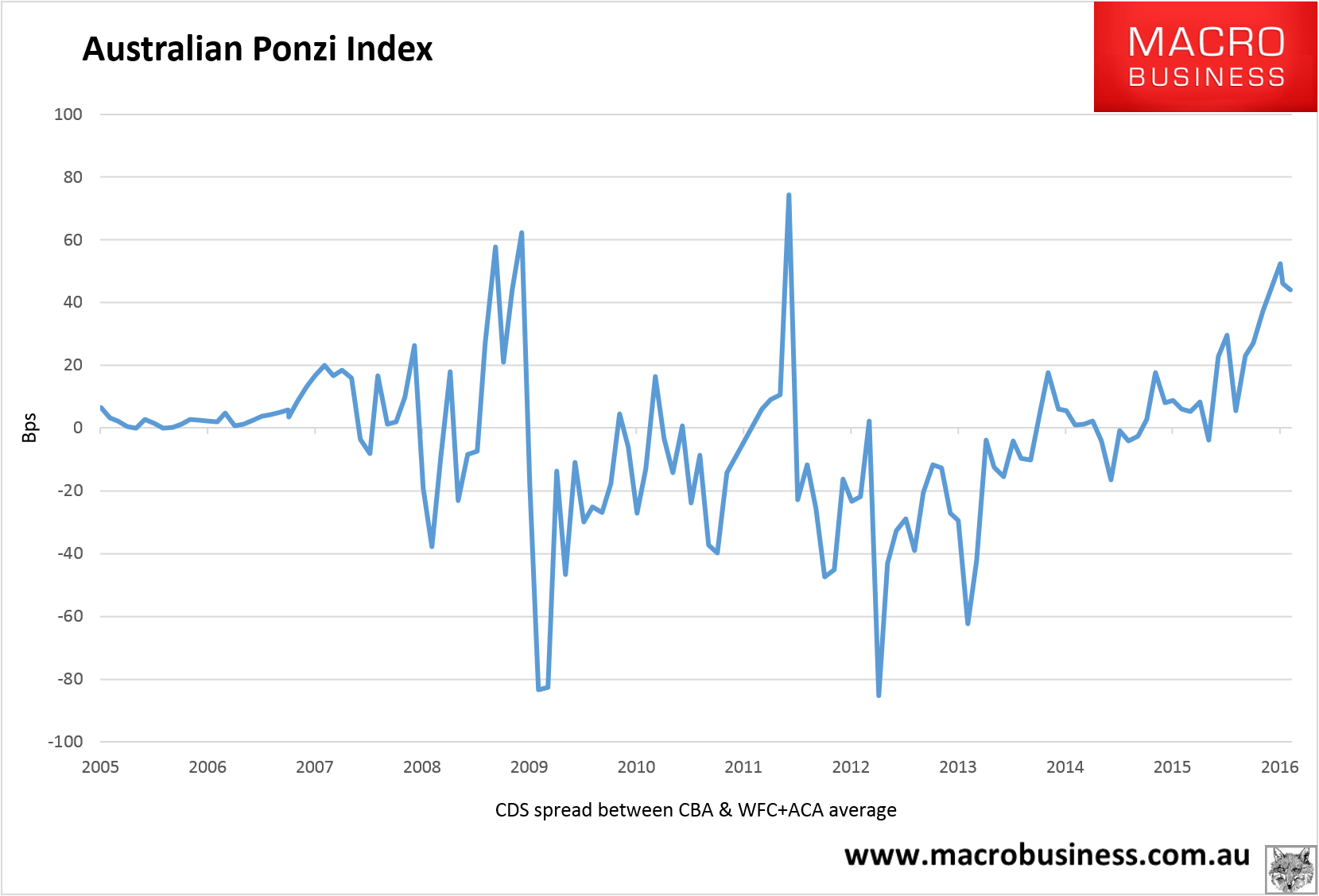

the chronic weakness in bank share prices;

that Australian banks are leading developed world funding costs higher:

Advertisement

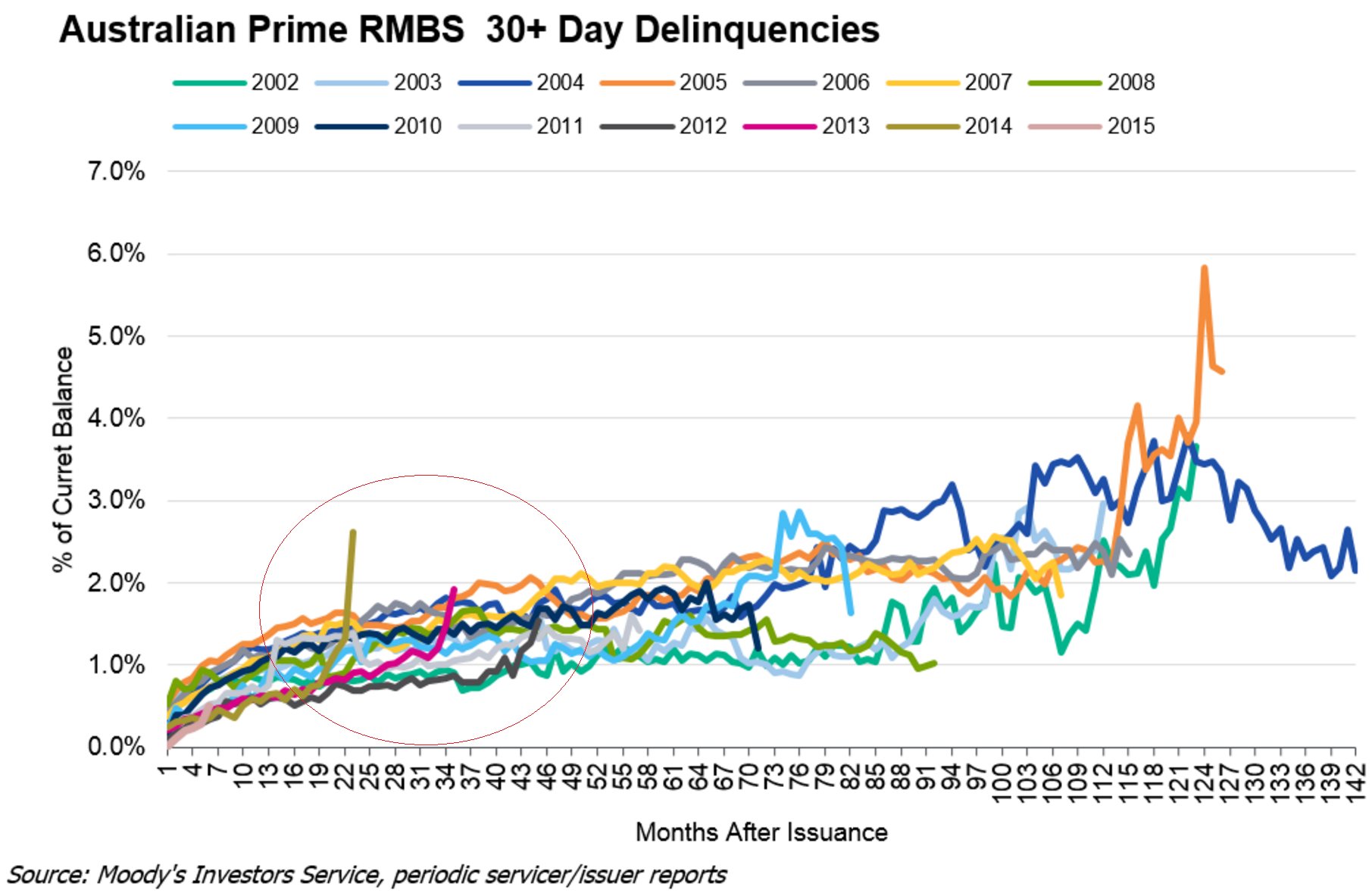

and, that real bad loans are now appearing quite swiftly in the pipeline in mining delinquencies and dumb bubble mortgage vintages:

Advertisement

8. A housing glut is fast approaching as population growth falls, as Goldman says:

Birth rate is at historical lows and deaths at historical highs

Australia’s birth rate is declining at its fastest pace on record and the growth in deaths is at a cyclical high, resulting in a marked slowdown in ‘natural increase’…Net migration has supplied 60% of population growth in recent years. However, our proxy for net migration suggests migration is now falling sharply. We show that over half of all net migrants are directly looking for a form of employment and over two-thirds enter Australia looking for either education or employment. As such, relative labour market conditions are a key determinant of net migration growth, and on this score the outlook is for further deterioration in net migration trends.

There are two crucial consequences of such a change. First, we reduce our estimate of ‘potential’ economic growth from 2.9% to 2.5% over the 2015-2017 period. Second, we change our estimate of underlying demographic demand for housing from a 140k underlying deficit for established homes by the end of 2017 into a 75k underlying surplus. Both adjustments complicate the outlook for monetary policy.

9. This is clincher, a global shock is coming. One can never say when and what form it will take but it appears to be playing out in the Mining GFC which is a toxic combination of developed economy monetary failure and emerging market excess production. If this shock hits a chronically weak Australia with limited stimulus firepower, inept management, a housing surplus and teetering at a tipping point then the dumb bubble is going to bust.

10. What other fate would one expect for the dumbest bubble in history? Again from last year:

So what makes Australia’s current property bubble so unique? Three reasons.

First, no other property bubble has ever had such a clear warning in advance of its blowoff. Just six years ago, the world writhed as a multitude of property bubbles spectacularly imploded. We saw it and it scared the bejesus out of us. Yet here we are, well short of a half generation later doing exactly the same thing.

Second, we have only just had the same long term property bubble bailed out by the biggest mining boom in history. Post GFC we rebuilt denuded savings and reliquified banks as mining poured billions into projects and jobs, while international markets collapsed all around. The serendipity was gigantic, easily big enough not just to protect us from the GFC but to redefine the basis of the economy towards sustainable prosperity for generations. But instead of being grateful and prudent we succumbed to the hubris of exceptionalism.

Third, the deteriorating economic circumstances of the commodities bust that we currently face have been obvious for three whole years (if not all along). We knew the boom was narrowly based in China. We understood the magnitude of investment. We knew the size of the supply expansion. We knew prices were going to fall a long way. We knew a capex cliff was coming. But authorities did nothing to prepare for the end point except to deliberately reinflate a housing bubble supposedly to float us blithely over the carnage.

Certainly the history of capitalism has seen bigger bubbles than Australian property. There have been stranger bubbles too.

David Llewellyn-Smith is Chief Strategist at the MB Fund and MB Super. David is the founding publisher and editor of MacroBusiness and was the founding publisher and global economy editor of The Diplomat, the Asia Pacific's leading geo-politics and economics portal.

He is also a former gold trader and economic commentator at The Sydney Morning Herald, The Age, the ABC and Business Spectator. He is the co-author of The Great Crash of 2008 with Ross Garnaut and was the editor of the second Garnaut Climate Change Review.

Birth rate is at historical lows and deaths at historical highs