The Reserve Bank of Australia (RBA) has today released its Financial Stability Review (FSR), which contains a useful assessment of Chinese investment in Australian property:

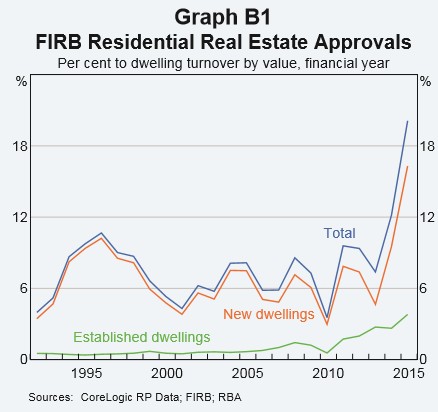

Non-resident Chinese buyers own only a small portion of the Australian housing stock, but industry contacts suggest that they account for a significant and increasing share of purchases. These purchases are largely concentrated in off-the-plan apartments (especially in Sydney and Melbourne), in part because all foreign buyers, other than temporary residents, are generally restricted to purchasing newly constructed dwellings. Consistent with observations by industry contacts, the limited and partial data available from the Foreign Investment Review Board (FIRB) suggest that approvals for all non-residents applying to purchase residential property have increased substantially of late (Graph B1). The majority of these approvals are for new dwellings in New South Wales and Victoria. China is the largest source of approved investment in (residential and commercial) real estate and its share of total approvals is growing, but it still only accounts for a small fraction of overall market activity.

Nonetheless, if a significant subset of buyers reduce their demand sharply, this can weigh on housing prices, and Chinese buyers are no exception to this given their growing importance in segments of the Australian market. Such a reduction in housing demand could result from a number of sources, including:

• A sharp economic slowdown in China that lowers Chinese households’ income and wealth. Any accompanying depreciation of the renminbi against the Australian dollar could further reduce their capacity to invest in Australian housing. In the extreme, Chinese investors may need to sell some of their existing holdings of Australian property to cover a deteriorating financial position at home. A macroeconomic downturn in China could also be expected to have knock-on effects on other countries in the region, which could also affect those countries’ residents’ capacity and appetite to invest in Australian property. On the other hand, if economic prospects in China deteriorate this could make investment abroad, including in Australia, more attractive and result in an increase in demand for Australian property.

• A further tightening of capital controls by the Chinese authorities that restricts the ability of Chinese households to invest abroad.

• A domestic policy action or other event that lessens Australia’s appeal or accessibility as a migration destination, including for study purposes. Industry contacts suggest that in addition to wealth diversification, many Chinese purchases are dwellings for possible future migration, housing for children studying in Australia or rental accommodation targeted at foreign students. If so, this demand could be expected to be fairly resilient to shorter term fluctuations in conditions in China or developments in the domestic property market, but more sensitive to changes in migration or education policy. A substantial reduction in Chinese demand would likely weigh most heavily on the apartment markets of inner-city Melbourne and parts of Sydney, not only because Chinese buyers are particularly prevalent in these segments but also because other factors would reinforce any initial fall in prices. These include the large recent expansion in supply in these areas as well as the practice of buying off-the-plan, which increases the risk of price declines should a large volume of apartments return to the market if the original purchases fail to settle.

The Australian banking system has little direct exposure to Chinese investors. Australian-owned banks engage in some lending to foreign households to purchase Australian property, but the amounts are small relative to their mortgage books. Australian-owned banks also have tighter lending standards for non-residents than domestic borrowers, such as lower maximum loan-to-valuation ratios, because it is harder to verify these borrowers’ income and other details, and because the banks have less recourse to these borrowers’ other assets should they default on the mortgage. Australian branches of Chinese-owned banks appear to be more willing to lend to Chinese investors because they are often in a better position to assess these borrowers’ creditworthiness, particularly where they have an existing relationship. Nonetheless, although the direct exposures are small, if a reduction in Chinese demand did weigh on housing prices this could affect banks’ broader mortgage books to some extent.

All fair enough, although it is disappointing that the RBA did not mention that the FIRB data to which it has drawn upon very likely significantly understates the true level of foreign purchases of Australian real estate, particularly existing dwellings.

As noted last year by the chair of the parliamentary inquiry into foreign real estate investment, Kelly O’Dwyer, the systems and data on foreign transactions is woefully inadequate and FIRB do not know the true levels:

Advertisement

“I regard the current internal processes at the Treasury and FIRB as a systems failure. Most concerning is that sanctions seem to be virtually non-existent. There have been no prosecutions since 2006 and no divestment orders since 2007. Suggestions by officials, that this is due to complete compliance with the rules is simply not credible. The data on foreign purchases of Australian houses and apartments is inadequate, making policy evaluations very difficult”…

The global regulator for money laundering, the Paris-based Financial Action Taskforce (FATF), has also identified Australian property as a haven for laundered funds, particularly from China, and has recommended that the Australian Government implement counter-measures to ensure that real estate agents, lawyers and accountants facilitating real estate transactions are captured by the regulatory net.

As I noted earlier this week, it also appears that the Government has given up chasing and prosecuting illegal sales of existing properties to foreigners.

Advertisement

After much bluster initially from Treasurer Scott Morrison about cracking-down on illegal foreign purchases of Australian real estate, he has been deafeningly silent of late. There are also rumours that ATO resources have been cut.

Again I call upon Treasurer Scott Morrison to end his silence and deliver a status update to the Australian people.

Leith van Onselen is Chief Economist at the MB Fund and MB Super. He is also a co-founder of MacroBusiness.

Leith has previously worked at the Australian Treasury, Victorian Treasury and Goldman Sachs.