From Bloomberg:

After inking a surprise joint venture deal with the world’s top iron ore producer, Fortescue Metals Group Ltd. is setting its long-term sights beyond China, its biggest customer and the world’s top customer.

The tie-up of Australian billionaire Andrew Forrest’s company with Vale SA amounts to the emergence of a new iron ore power bloc, according to Macquarie Group Ltd. The accord, which allows for the Brazilian company to buy a minority stake in Fortescue and invest in existing or future mines, may help the world’s fourth-biggest producereventually push into new markets to the west of China, according to Chief Executive Officer Nev Power.

“In the most difficult circumstances, he’s always ready to pull another rabbit out of the hat,” said Philip Kirchlechner, previously Fortescue’s head of marketing from June 2003 to May 2006. The pact is “quite a sophisticated idea because it is doing something more strategic and visionary,” said Kirchlechner, now Perth-based director at Iron Ore Research Pty.

The accord partners, whose first priority is an ore blending joint venture in China, also have an eye on developing a pipeline of projects that could eventually feed steel demand driven by the demographic change likely to sweep through Central Asia to the Middle East, Fortescue’s Power said March 15 in an interview.

“Their self belief is very strong and they have a really good operating team,” said Morgan Ball, managing director of iron ore producer BC Iron Ltd. Fortescue and BC Iron in December suspended a joint venture with a capacity of six million tons a year because of lower prices. “They are pretty innovative, they think about things differently,” Ball said in an interview in Perth.

Sure they are but they’re still horribly doomed. The “power block” argument is rubbish. If it weren’t the deal would never get up with regulators. The reason why is simple enough, when the juniors are all gone, FMG and Vale are left as the marginal cost producers so they were going to have to cut production anyway. It is extremely unlikely that they can lower long term costs for their blended material below that of RIO and BHP given its moisture content, blending costs and diminishing returns from high-grading. Meanwhile, BHP and RIO can just keep driving costs lower and lower given their still bloated management structures from the boom.

But the rubber really hits the road on demand. Over the long haul, nobody yet understands just how stuffed iron ore is. Let me show you.

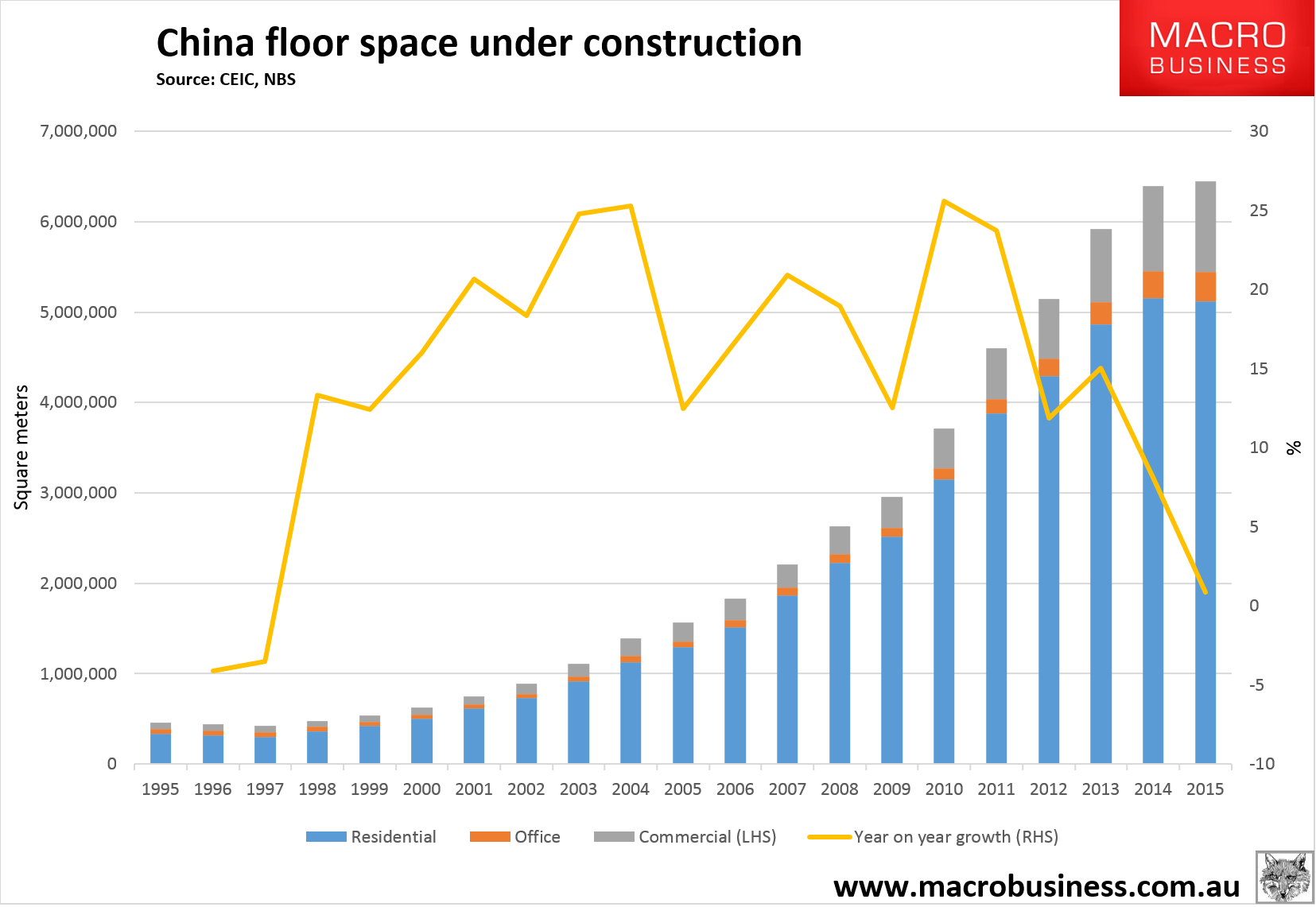

First, here is the stock of Chinese floor space under construction which absorbs half of Chinese steel consumption:

Total Chinese floor space under construction is peaking. Residential already has, office and commercial are next.

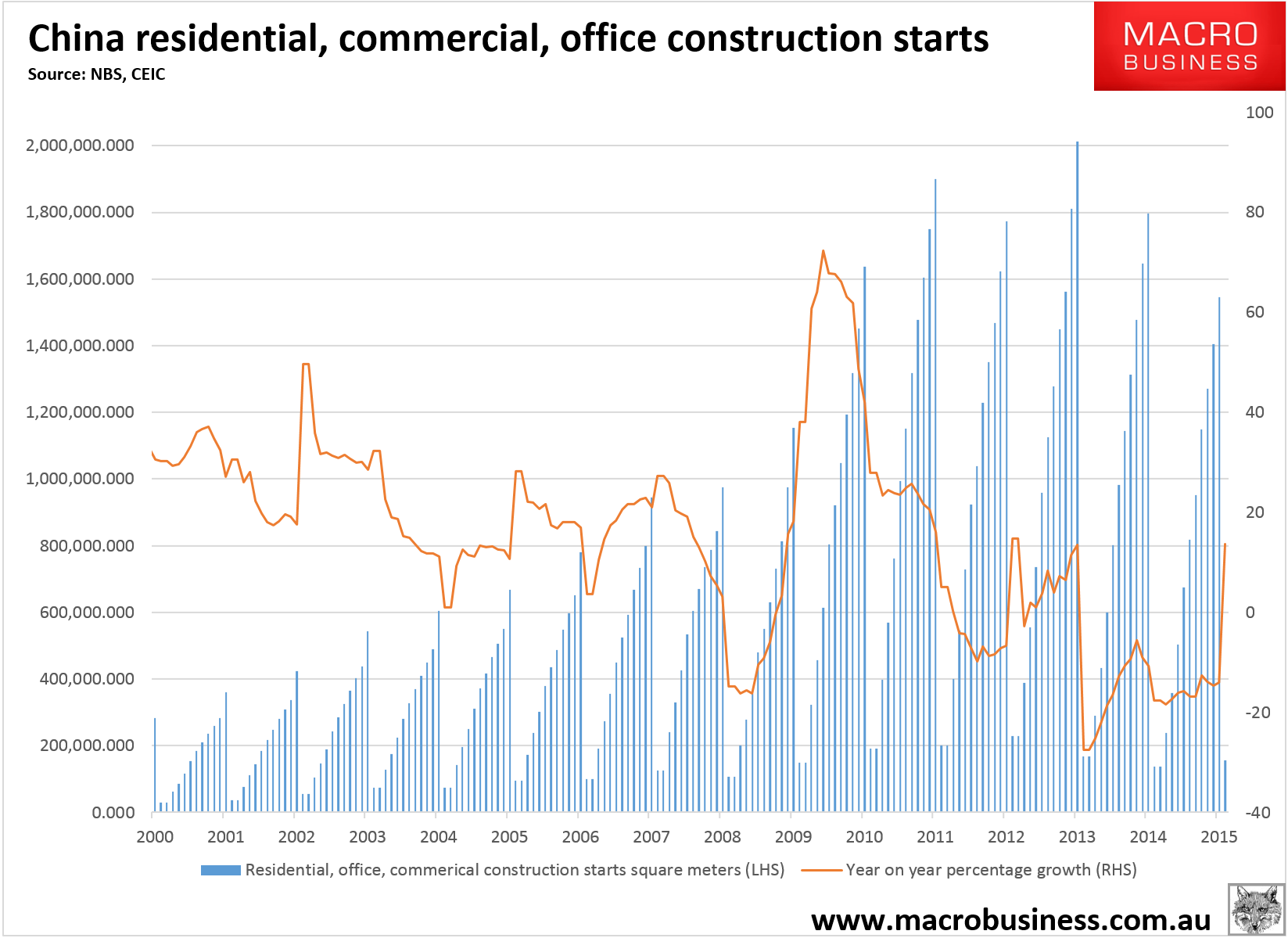

Second, here is the flow of Chinese floor space new starts:

There is always a lag between stock and flow as starts take time to complete meaning that big falls in total Chinese floor space construction are already locked in for this year and next.

That’s the good news. The bad news is that this boom was a one-off. A once per century modernisation build-out that is now on the down slope as urbansition slows materially leaving existing construction stock sufficient for many years. The draw down on the boom will thus be vast and for iron it really does boggle the mind. China currently imports roughly one billion tonnes of iron ore annum. But as its steel output declines to 500 million tonnes plus exports (net 600mt) over the next decade, seaborne iron ore demand is going to fall by 300mt minus whatever amount Chinese iron ore mines shut. If we say that’s 100mt then Chinese demand for seaborne iron ore will fall 200mt even as the seaborne market adds another 200mt of locked-in supply. That means 400mt of seaborne iron ore is going to have to be rationalised unless more demand can found. There’ll be some but nowhere near enough. Let’s be very generous and say another 100mt of demand growth.

That leaves 300mt to come out of current current seaborne producers, 100mt of that might be global juniors leaving 200mt for Vale and FMG to cut.

FMG is a superb miner but an apocalyptic commodity economist and that will destroy it in the end.