Special report: Five reasons the mining bust is not over

The ANZ’s Richard Yetsenga has nailed his colours to the mast, from the ABC:

The bank’s acting chief economist and global head of financial markets research Richard Yetsenga told a business function in Perth he believed the commodity bear market days were in their “final stages”.

“I don’t think you’ll see new lows for the oil price, I don’t think you’ll see new lows for the iron ore price,” he said.

“That suggests we will get headline inflation this time next year of somewhere between 1 and 2 per cent, rather than something around zero, so that also means central banks start to sound much more comfortable about where things are and less alarmist.

“I don’t have a great rationale for a bull market around the corner but I think that downshift in commodity prices is basically done.”

“When the news is bad, we hunker down immediately and severely on the assumption it’s about to get a lot worse,” he said.

“The risks of a substantial downside surprise are much, much lower than I think than what you would get from reading popular press and a range of popular commentators.”

“Unemployment rate at 6 or 5.8 on yesterday’s number is not a great number, but it’s not terrible either when you consider the adjustment that we are going through and where the global economy has come from,” Mr Yetsenga said.

“I think the era of zero rates is drawing to a close, we might see one or two more moves from different central banks because of a particular local circumstance but I think this post-crisis period of easing policy is starting to finish.”

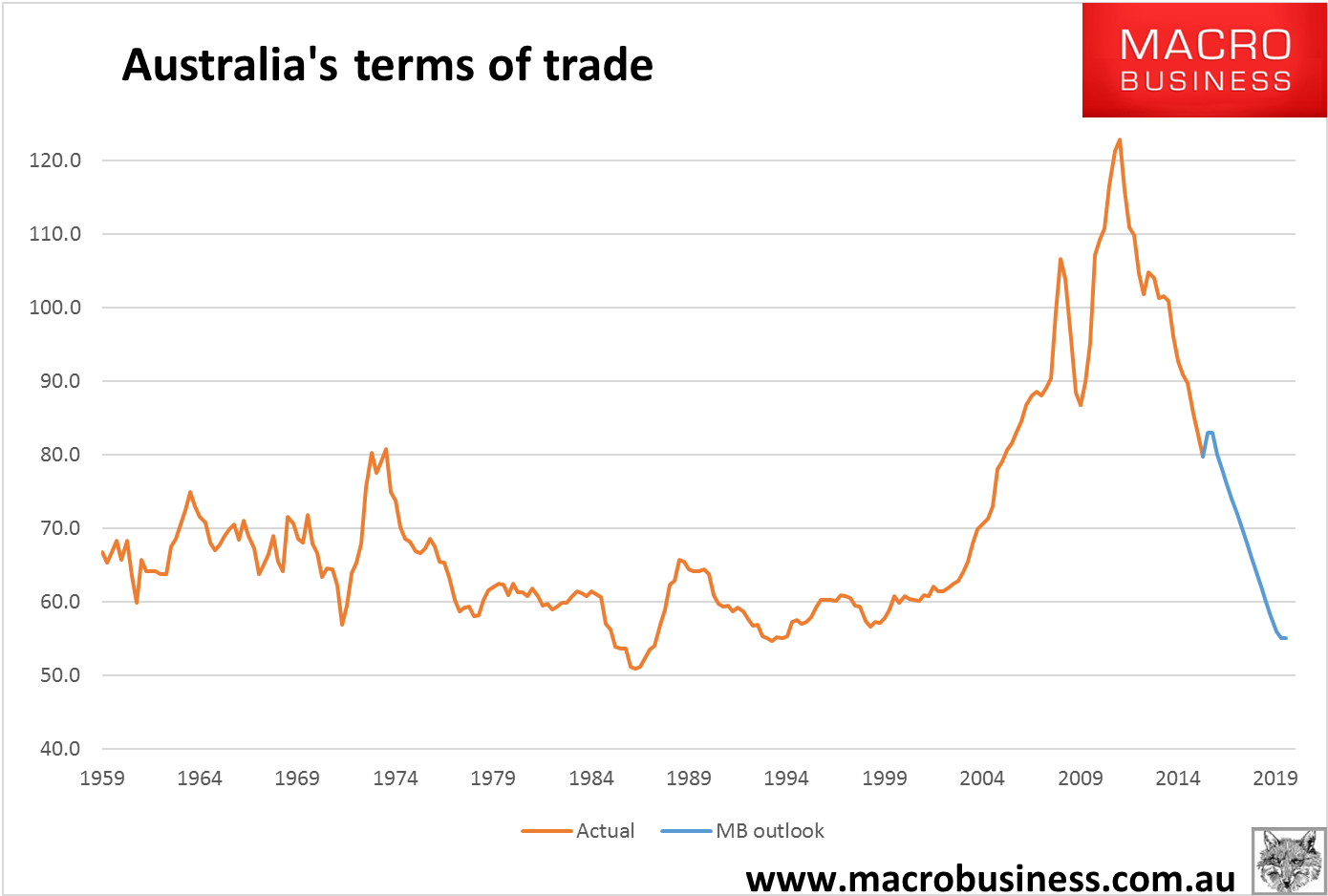

Some bold stuff there. MB remains unconvinced. The commodity bear market is certainly closer to the end than it is to the beginning but given it’s been running for five years that’s not terribly comforting. To believe that commodity prices have bottomed, one also has to believe that Australia’s terms of trade are about to plateau at their highest pre-China boom level in history:

To draw that conclusion MB would have to suspend everything it knows about markets and their tendency to overshoot, as well as commodity economics which is, in the end, all about just one thing: finding the lowest marginal cost producer.

Rebalancing

There are two ways an oversupplied commodity market can rebalance. As prices fall, cheaper material triggers renewed demand and expensive supply becomes uneconomic and closes. The two key prices for the commodity bear market (for Australia) are oil and iron ore so let’s take a look at both and see where we are.

Both have been convulsively sinking and rising over years in deepening downtrends (the latter longer than the former) as each tries to shake out enough supply to balance the market after years of over-investment. That is a process of price discovery that seeks to displace the marginal cost producer.

For oil, it has to bankrupt the highest cost output of US shale. For iron ore it has to shut the mines of a global spread of juniors. Each price fall has triggered production slowdowns then a price rebound which has been met again with resurgent supply. This is currently happening in iron ore after just a few months of stronger prices. In oil, the US shale rig count stopped falling last week indicating that it is also approaching stabilisation after just a month or tw of rising prices.

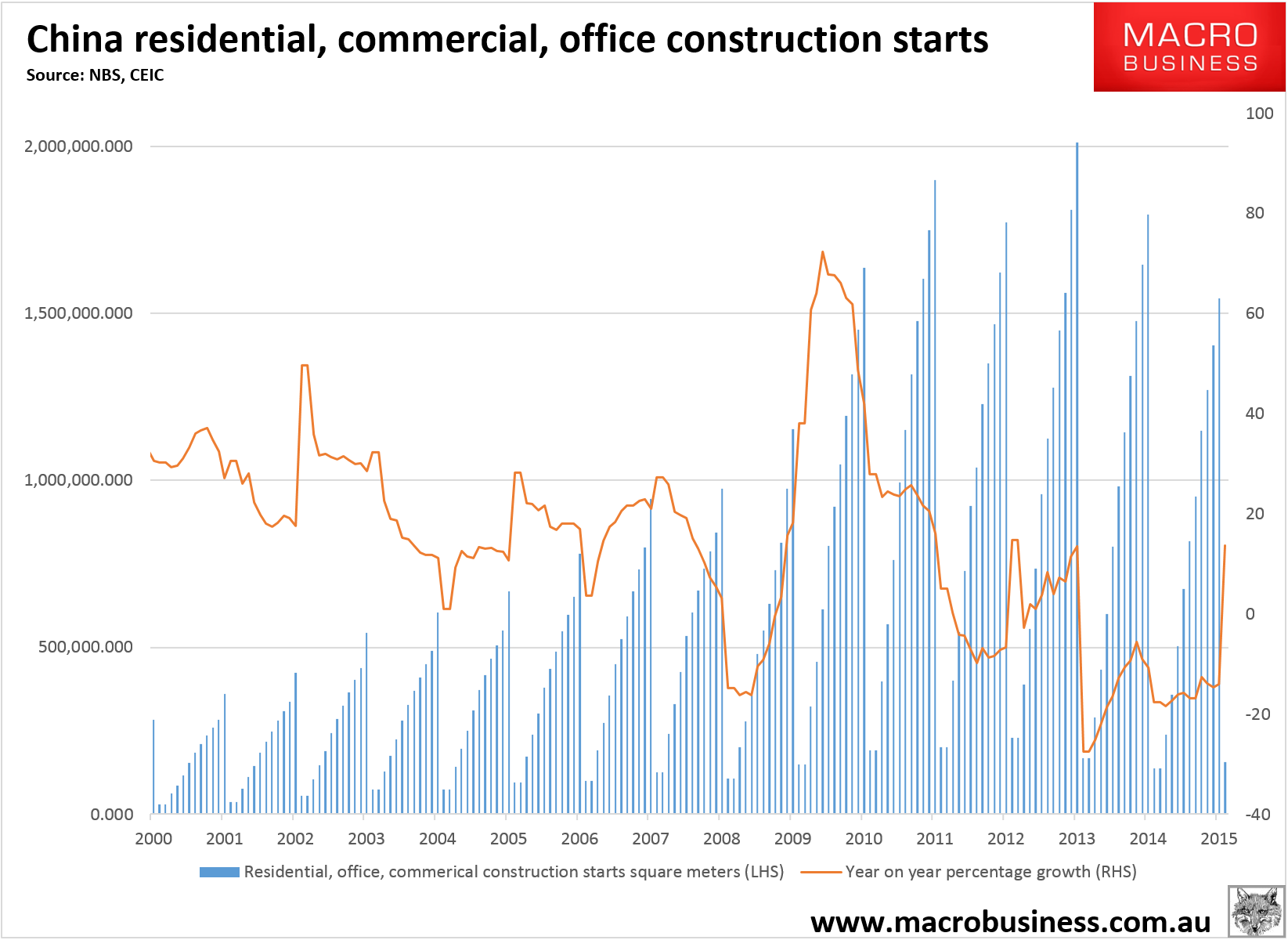

On the demand side of the equation, iron ore is very troubled given global steel production is falling fast, down -2.8% last year but accelerating such that January production was down -7.1% year over year. The driver of this is, of course, waning Chinese investment growth and, in particular, the fading post 2009 residential construction boom:

You can see the huge post-GFC boom, the 2012 peak and now downtrend which I expect to run for a decade. We began this year with a bang, up 13.7% year on year, which could lend short term support to steel and iron ore demand, but one needs to take the specifics of this data with a grain of salt given its granularity is doubtful (that is, we’ve seen similar brief spikes before disappear just as quickly). It’s the trend in the flow of starts that matters and it is down.

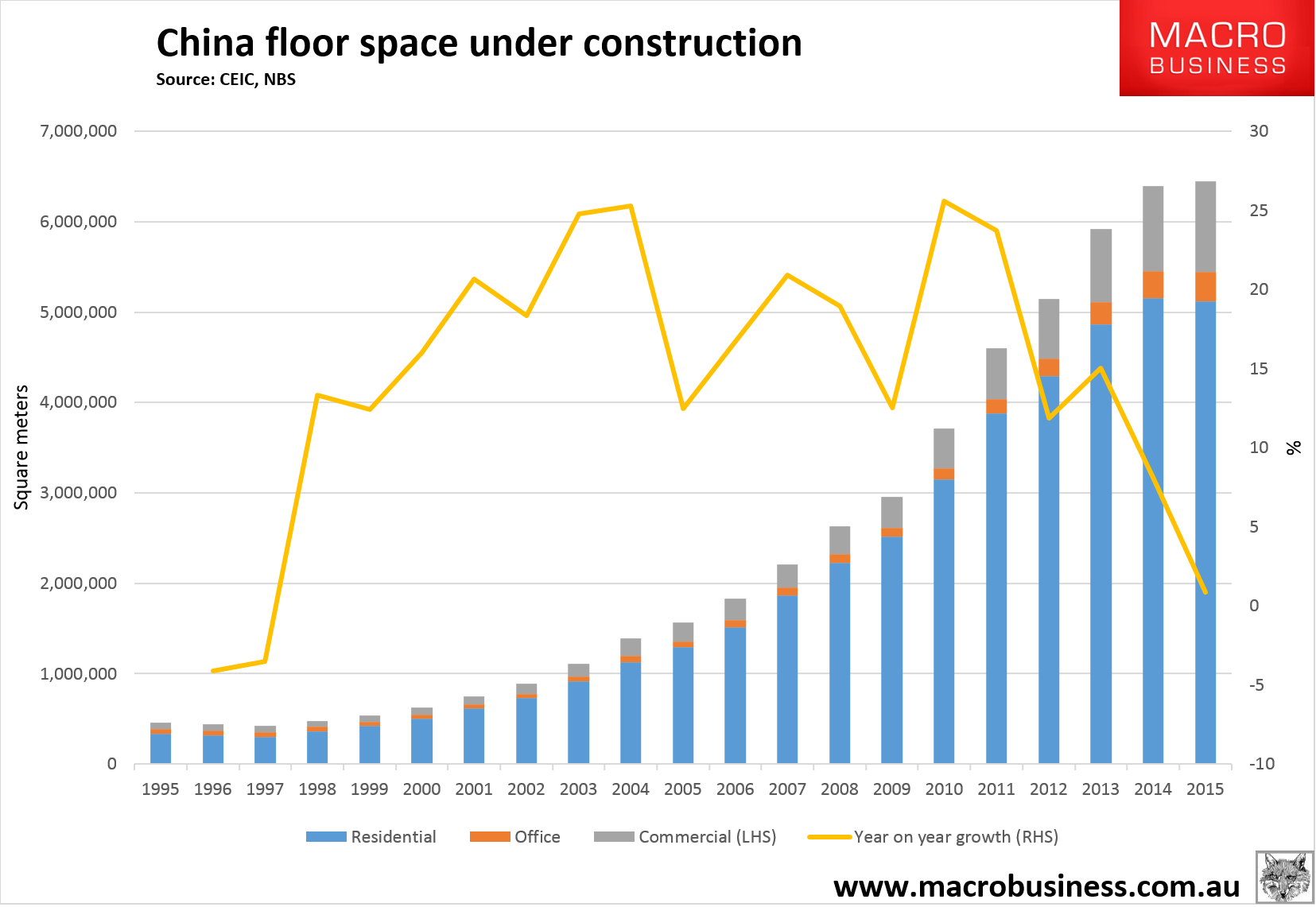

The stock of floor space under construction lags starts by two years or so and here the story is the same:

Total Chinese floor space under construction is peaking. Residential already has, office and commercial are next.

More to the point, this chart represents 40-50% of Chinese steel demand and thus roughly one quarter of global steel consumption. And given China imports roughly 80% of its iron ore, the Chinese construction market’s impact on seaborne prices is greater still.

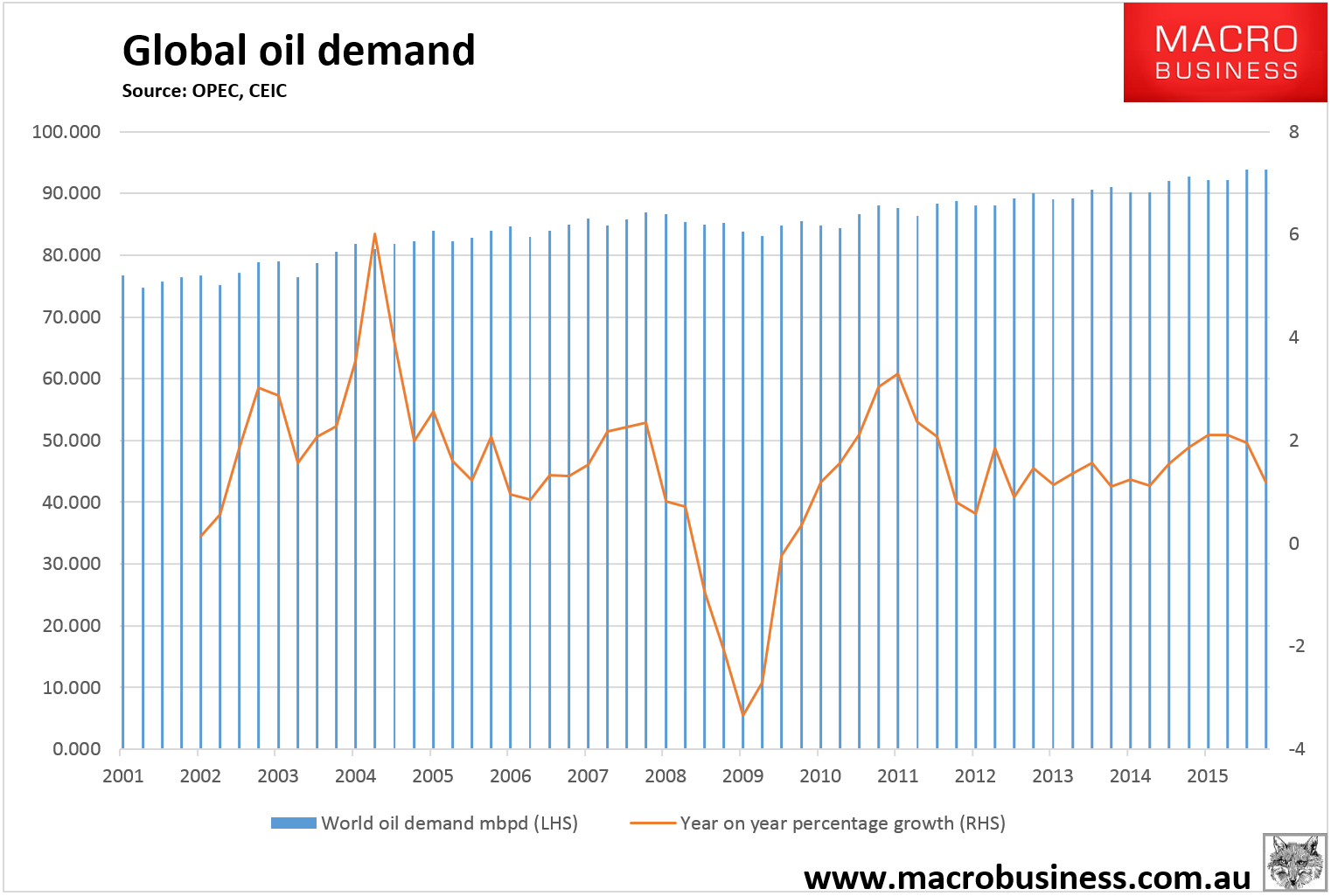

For oil, the demand story is better as it continues to grow via cheaper prices:

However, even here the growth is slowing sharply and it will not be enough to absorb the present glut over the medium term without further supply side curtailments.

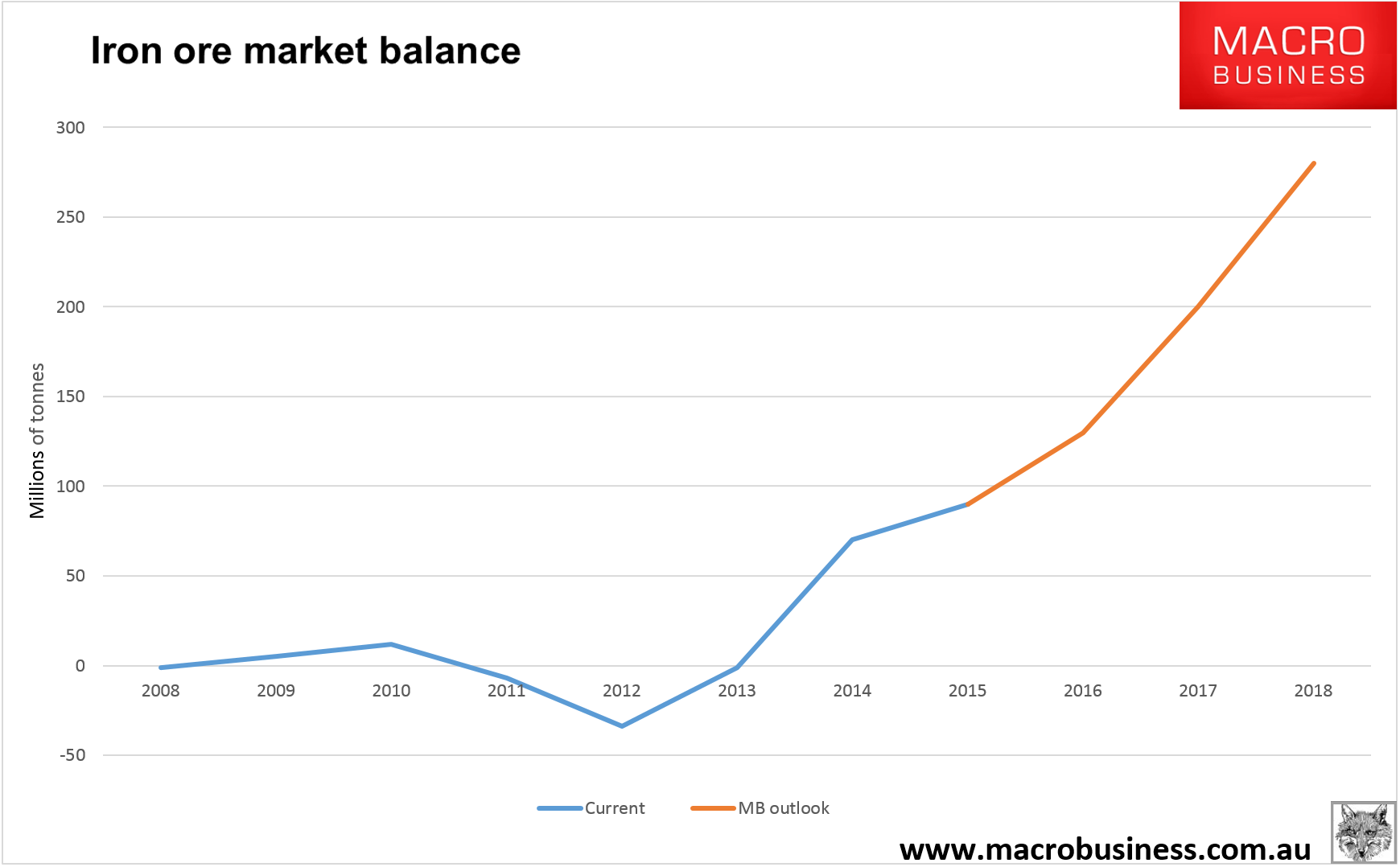

Which brings us to production for the two commodities. We know that iron ore is in structural surplus because its price has fallen from $190 to the mid-$50s. MB puts that surplus currently at around 90 million tonnes (mt). We’re seeing a cyclical tightening in the market on Chinese restocking and supply disruptions, but that will pass and before long we’ll get yet more supply even as Chinese demand keeps shrinking. 200mt of new iron ore supply will come on stream in the next three years as Chinese demand falls at an average rate of 30mt per year with no global offset. Thus we will need to to see another 250-300mt of iron ore supply curtailment:

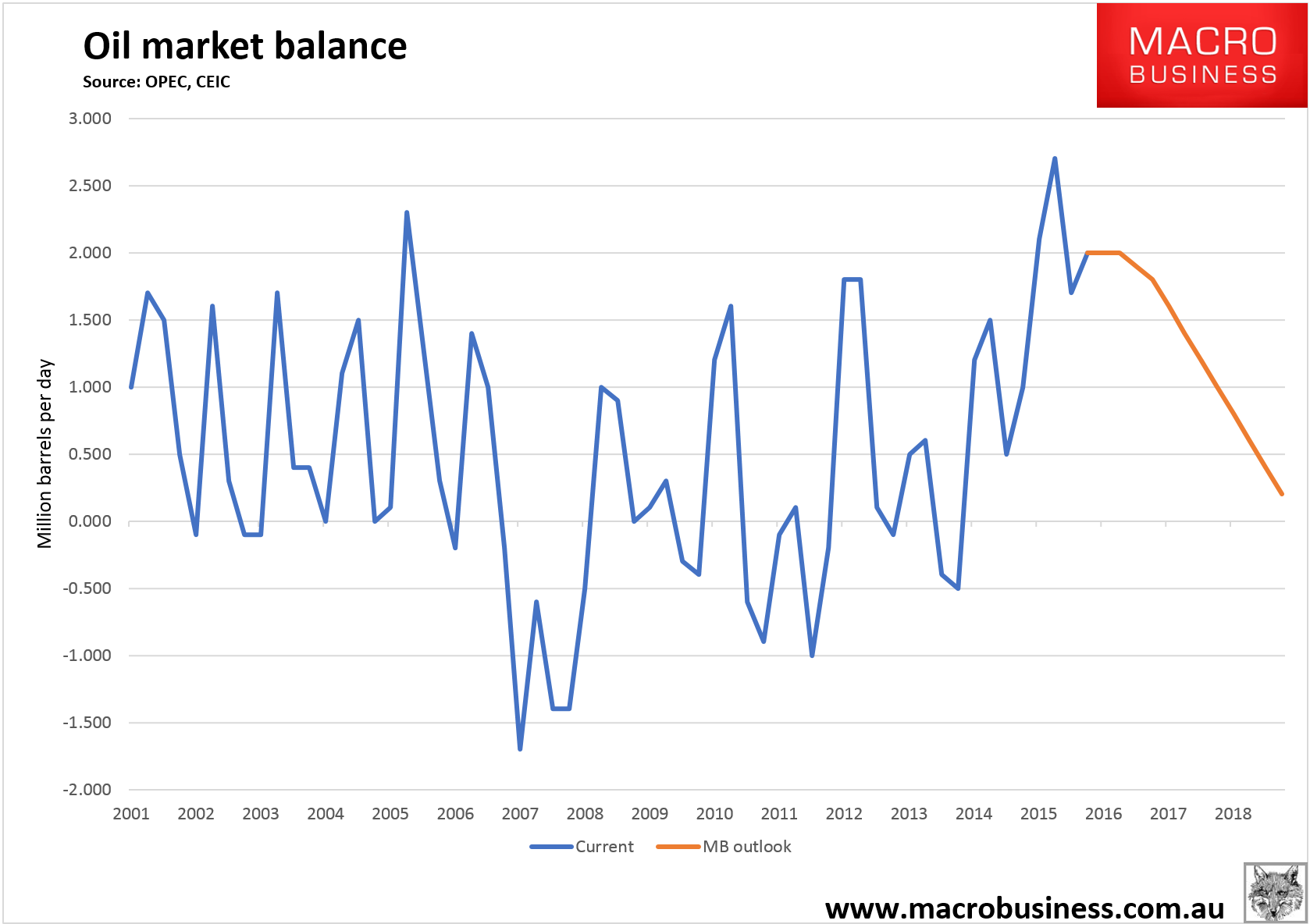

For oil the picture is again better on the supply side but still not rosy. Growing Iranian supply is largely going to offset any demand growth over the next year despite the much vaunted N-OPEC “supply freeze”. Thus unless the US shale bust accelerates, demand only eats into the glut slowly at -400mb/d each year:

Neither of the above market balance charts include any forthcoming supply curtailments. And that is the point. They’re going to be needed and the only trigger for them is price which is going to need to fall again.

There is roughly 100mt of seaborne junior ore that can still come out in the mid-$30s. Chinese ore production can fall further too, let’s say another 50mt. But the rest will take serious pressure on major producer cash costs which are down to the mid and low $20s. The iron ore price correction is far from over.

The actual outcome for the oil outlook will more be volatile than the chart given seasonality and disruptions but it is the base case. It’s possible that Brent oil has bottomed but even so all things equal it still needs to revisit $30 to accelerate the demise of US shale. And while oil falls so, too, can every other commodity including base metals, LNG and coal as their input costs are crunched.

Conclusions for Australia

The current rally across the commodity complex is based upon two false assumptions:

- first, that Chinese demand is about to take off again. It isn’t. The best case scenario is a few quarters of better construction growth then a renewed glide slope lower. China is built-out and must transition to other drivers of growth, and

- second, that the recent easing of expectations for rate rises in the US has taken pressure off the US dollar (and may lead to further falls) which in turn boosts commodity prices. Though that is true, and perhaps the Fed can help support demand growth by tightening more slowly, what the Fed can’t do is prevent it’s easy money from also supporting commodity supply which it is already doing as high yield debt markets recover for miners and shalers alike.

Thus, even if the US dollar falls further, at some point commodity prices are going to have to decouple from it (that is, also fall) if markets are to rebalance.

So, there are two broad scenarios in the offing for Australia:

- in the first, the Fed is slow with, or done, tightening, the US dollar falls (but not overly far given it is still the “cleanest dirty shirt” among forex markets, commodity prices lift for a time, broader markets are stable and demand slowly eats up the oil glut, but iron ore continues its relentless collapse. After a shortish period the Australian dollar resumes falling but owing an easy Fed (and others) does not fall fast enough to help the economy “rebalance” and so income, as well as economic prospects deteriorate leading to interest rate cuts and a lower dollar over the medium term. In this scenario MB’s outlook for the Aussie reaching 60 cents this year and 45 cents at the cycle bottom is likely to be overly bearish by 10% or so;

- in the second scenario, the Fed is slow but continues tightening, the US dollar remains high or climbs further after some consolidation, broader markets collapse again leading to a credit market event that rebalances commodity markets via an accelerated balance sheet shakeout. The Australian dollar falls fast as Australia plunges into recession owing to the income shock and rising debt funding costs.

MB still sees the balance of risks tilted towards scenario two given market behaviour tends towards tipping points and over-reactions (as we’ve so clearly seen over the past ten weeks).