The Mining GFC rose a little again last night as investors turned from the ECB to the FOMC and bought the US dollar:

Commodity currencies were broadly sold off:

Oil too:

Advertisement

And base metals:

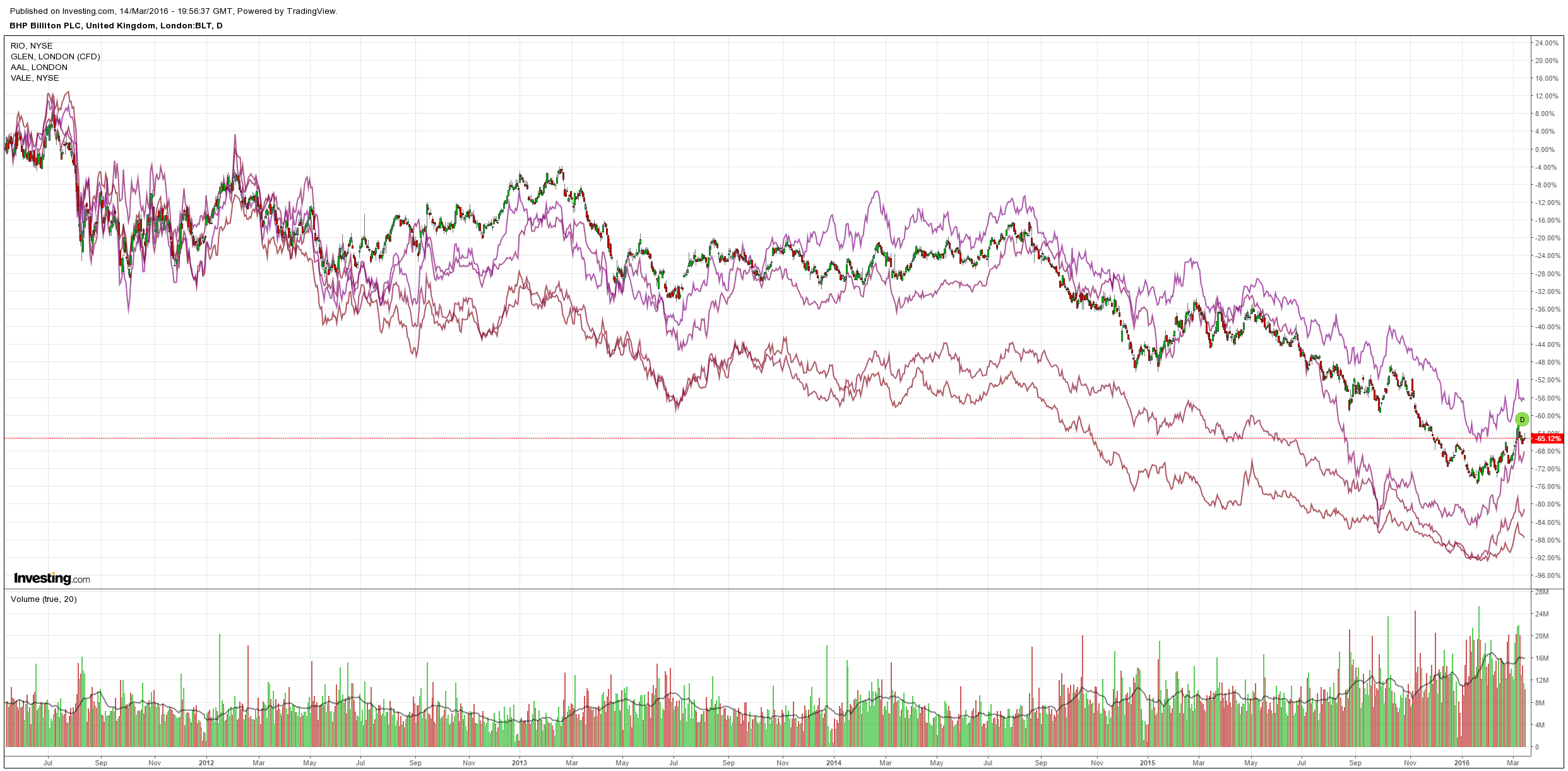

Miners were mixed:

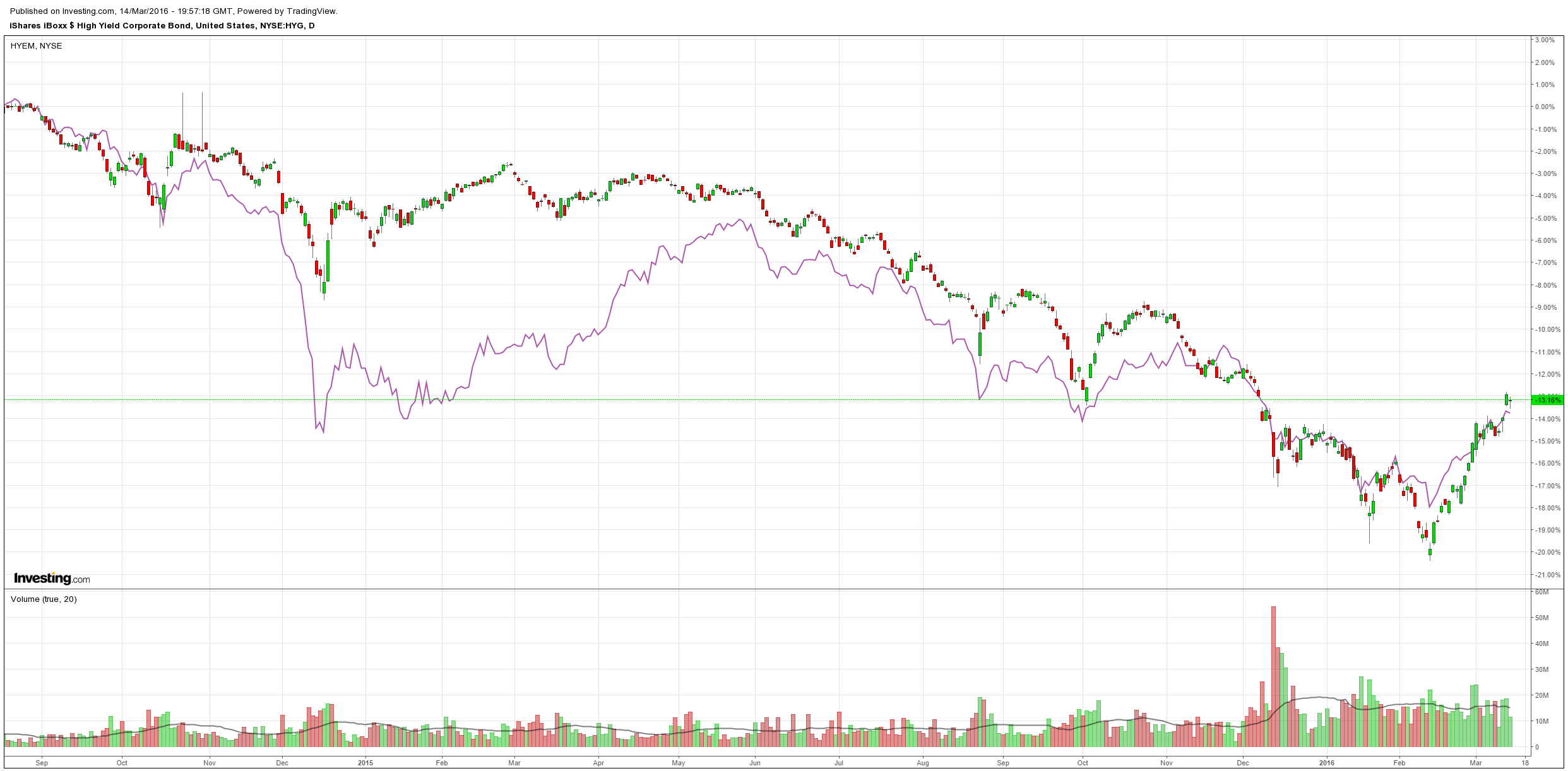

Importantly, US/EM high yield debt held its gains indicating risk is still live:

Advertisement

Readers will recall that the Mining GFC set-up is all about a weakening China and yuan plus strengthening US and dollar, a perfectly toxic combination for global commodity prices. Deutsche adds some interesting material on the former with a look at the adequacy of Chinese forex reserves:

The IMF approach is based on construction of a risk-weighted measure of potential drains on foreign reserves. A broad set of risks is encompassed. Sources of risk include external liabilities as well as current account variables and some measure of potential capital flight.

Specifically, four risk variables are considered:

(i) exports – to capture the potential loss from a drop in external demand or a terms-of-trade shock;

(ii) short-term debt;

(iii) medium- and long-term debt and equity liabilities;

(iv) broad money as a measure of the risk of capital flight.

Risk weights are then based on the relative importance of each of these variables during past episodes of pressure on foreign exchange markets. In other words, the risk weights are assigned based on observed outflows from the different potential sources of BoP pressure in past stress situations. Somewhat higher risk weights are applied to countries with fixed rather than floating exchange rate regimes. These risk weights are provided in the table…

[China’s] reserve stock stands at only 114% of risk-weighted liabilities, if we assume a fixed exchange rate regime. The reason for this is that the multidimensional measure, unlike standard ones, considers broad money supply (M2) and exports as liabilities; China has very large levels of both of these. China’s falling stock of reserves over the past 18 months has also contributed to the current position. Reserves have been drained to keep the currency stable amidst persistent capital outflows driven by slowing growth and the rebalancing of the Chinese economy. Further, an unwinding of the long CNY carry trade has also put pressure on the currency, on the back of diverging monetary policy with the US.

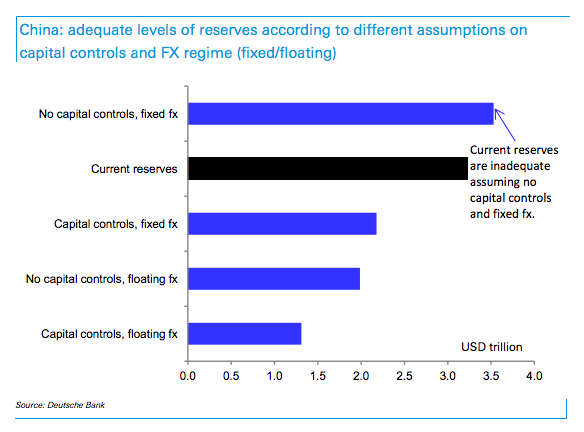

The analysis thus far does not account for the effect of capital controls. If we assume no capital controls and a fixed exchange rate regime (as we have done for China so far), the risk-weighted metric would imply that reserves of USD 3.5tn would be adequate, above the current reserves level of USD 3.2tn.

However, one must account for capital controls in China’s case. This would involve reducing the weight on M2 in the risk-weighted liabilities calculation, as effective capital controls would prevent capital flight. The base case we have assumed thus far is one of no capital controls and a fixed exchange rate; but given the rapidly changing policy space on these two fronts and the eventual aim of opening up the capital account and moving to a floating exchange rate regime, we need to consider alternative scenarios as well. In the chart below, we show the adequate levels of reserves (i.e. those corresponding to 125% of the risk-weighted metric) under the different assumptions on capital controls and FX regime (fixed/floating). In the previous section we highlighted how the risk weights differed for fixed and floating FX regimes. To observe how China’s reserves line up under the capital controls scenario, we reduce the weight on M2 from 5% to 2.5% for the floating FX regime and from 10% to 5% for the fixed exchange rate regime.

The results show that if we assume capital controls or a floating exchange rate regime, the adequate reserve level is less than USD 2.2tn, implying that current foreign reserves (USD 3.2tn) are sufficient.

However, the key takeaway here is that standard measures significantly overstate the adequacy of Chinese reserves. When we look at foreign reserves in terms of the more complete, multi-dimensional risk-weighted metric, the cracks in the surface are clearly visible. The headline reserves stock of USD 3.2tn does not look so adequate anymore, and under the assumption of no capital controls and a fixed exchange rate, the reserves level is outright inadequate. China’s best option is therefore to maintain capital control and yet allow some level of exchange rate adjustment to continue.

Advertisement

In short, China is short of dough to protect the currency so you can expect more closure of pipelines of capital flight. If it does come to crisis or an end of cycle shock then the foreign bid for Australian real estate will not fare well.

David Llewellyn-Smith is Chief Strategist at the MB Fund and MB Super. David is the founding publisher and editor of MacroBusiness and was the founding publisher and global economy editor of The Diplomat, the Asia Pacific's leading geo-politics and economics portal.

He is also a former gold trader and economic commentator at The Sydney Morning Herald, The Age, the ABC and Business Spectator. He is the co-author of The Great Crash of 2008 with Ross Garnaut and was the editor of the second Garnaut Climate Change Review.