For markets, the Mining GFC is now in full and panicked reverse gear. It’s buy anything today that was sold yesterday regardless of the order of things. The US dollar surged:

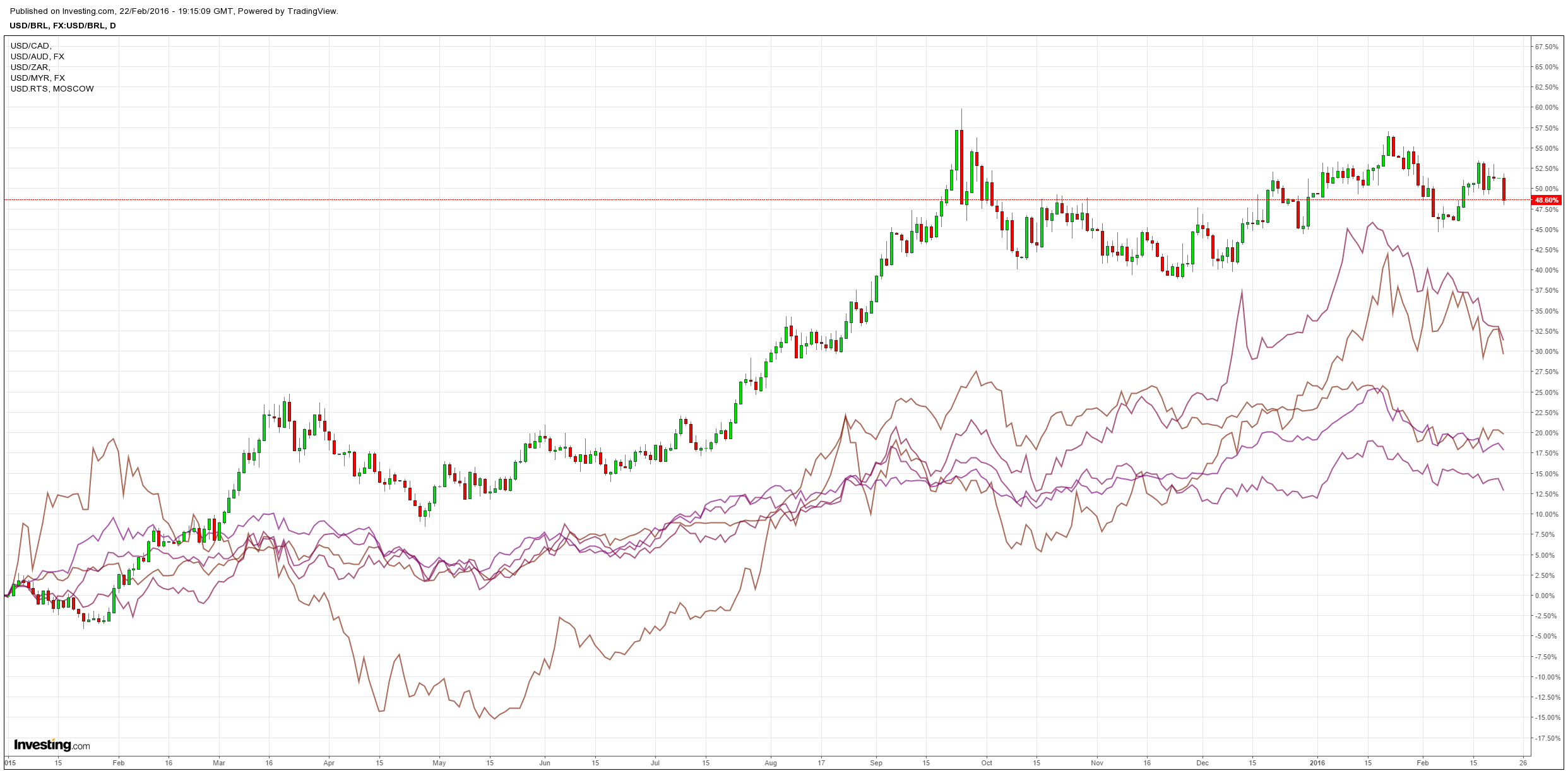

But that didn’t prevent commodity currencies from going even higher:

Or oil surging:

Or base metals surging:

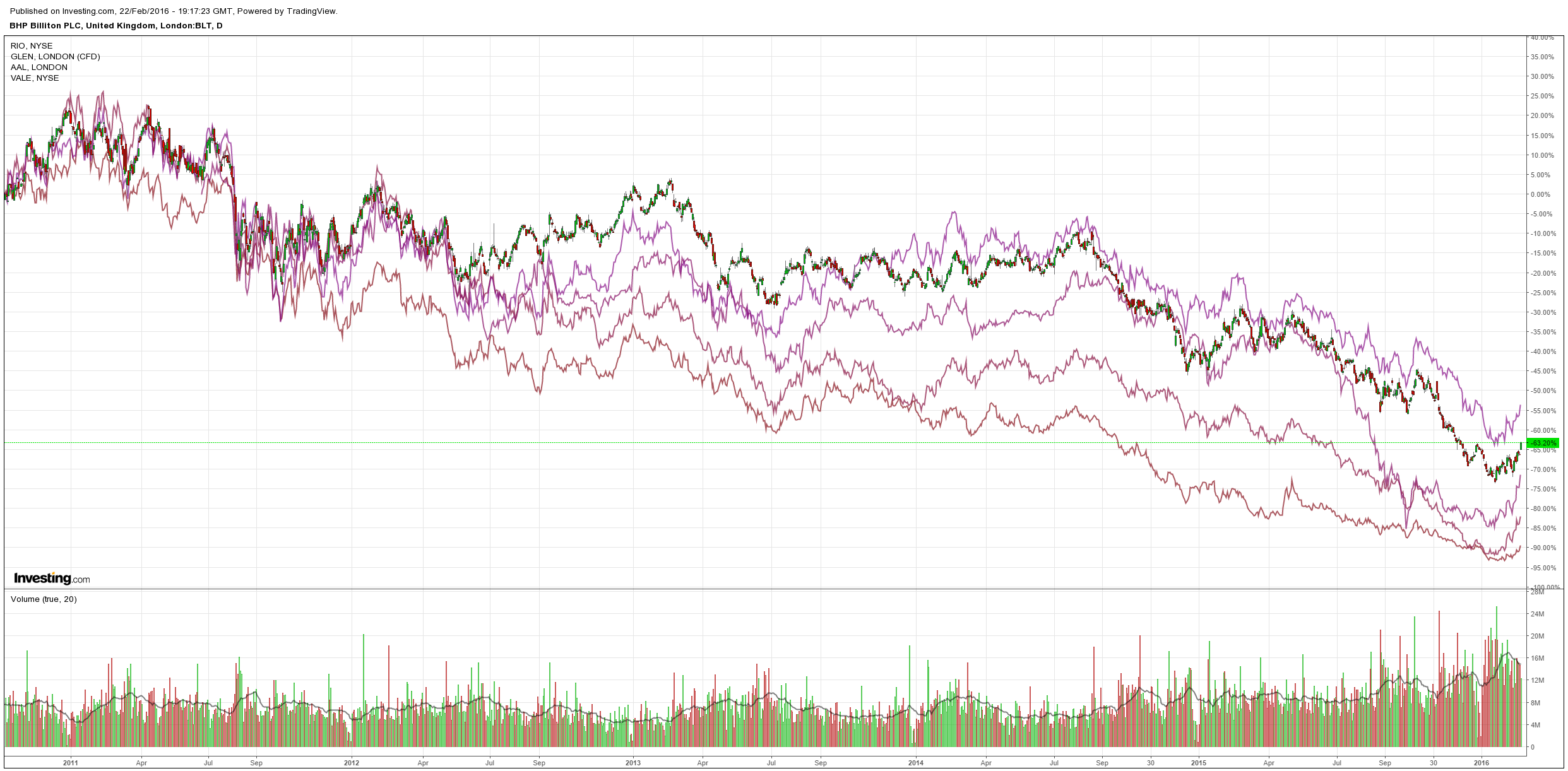

Or miners going completely gaga with BHP up 8.5% and RIO 8.4% in London:

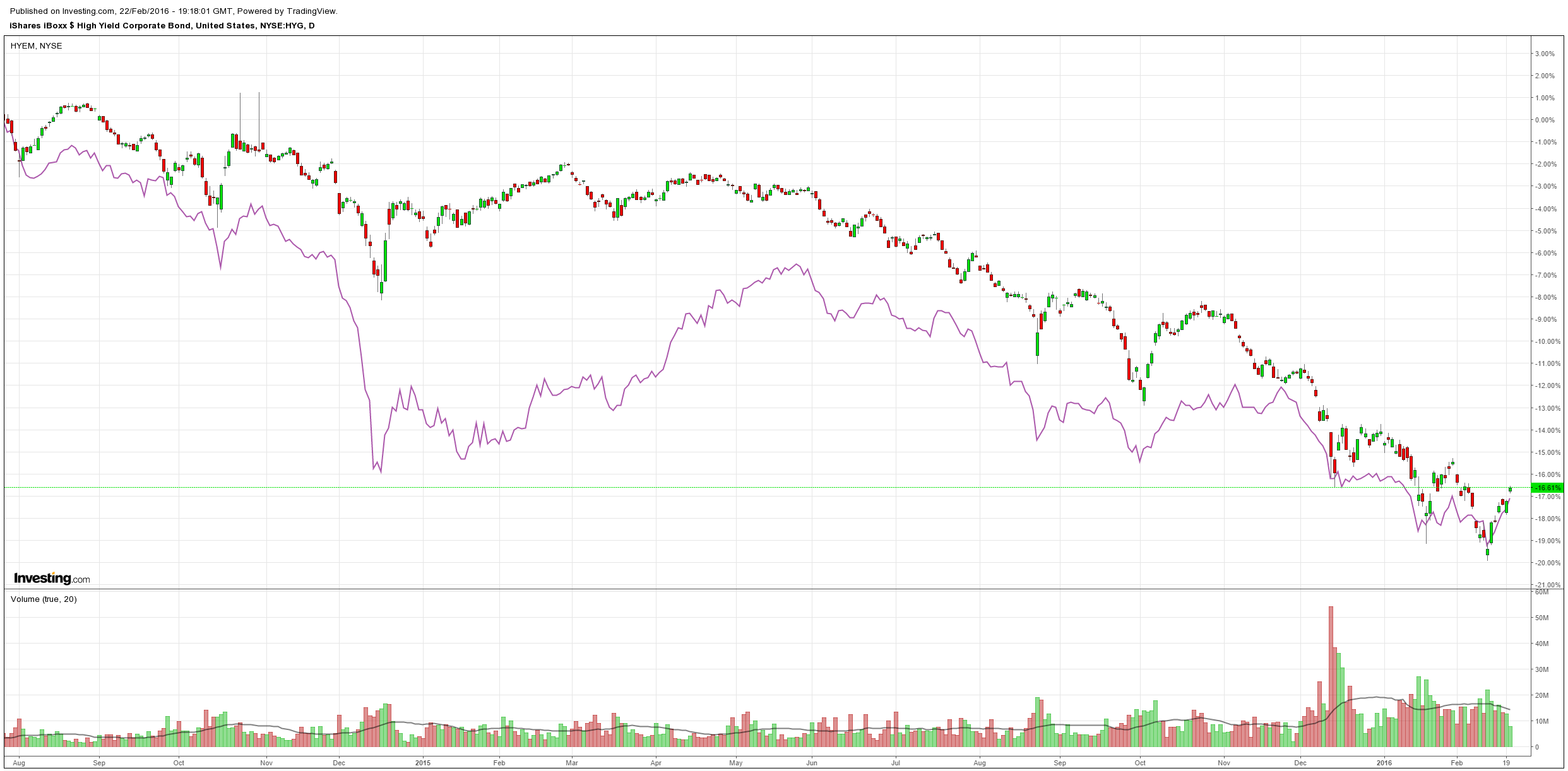

Or high yield US and EM debt rebounding strongly:

So what happened on the night? Nothing. Short markets have been hit by the Chinese stimulus, such as it is, and the OPEC non-deal. Neither changes the outcome but it’s enough to make shorts puke their positions.

Or, you might prefer Goldman’s take:

Risk assets traded somewhat better last week and into the open this morning, and equity volatility is receding. Investors are starting to see the glass as half full. We continue to judge the economic outlook as healthier than what the rate and credit markets in particular currently discount (e.g., government yield curves should be steeper and IG spreads tighter than what is priced).

There are three main risks in that, in the short term, could alter our central expectations:

Developments in crude oil prices: As seen again last week, risk sentiment is still dancing to the tune of WTI. Lower crude oil prices kick up credit risk in HY markets and bank loan books, accelerate central bank reserve de-cumulation (i.e., lead to the sale of financial assets held by petroleum exporting countries in developed markets), and amplify the pressure on inflation-targeting central banks to respond via unconventional policies. Where these involve negative rates, the profitability of commercial banks is negatively affected.

European banks and cost of capital: Banks have underperformed global stock indices in the US, Japan and Europe by an average of 13% since the start of the year. The common factor is a reversal of the interest rate outlook, with rate hikes by the Fed being pared back (the probability of a cut increasing) and the BoJ introducing negative policy rates. Within these broader dynamics (which should reverse if we are right on inflation, and the outlook for rates), European banks have been hit harder owing to the uncertainties relating to the new Bank Recovery and Resolution directive (BBRD). Whether there will be a relaxation in the application of the regime, or joint initiatives between governments and the national central banks to address the problem of legacy assets is unclear.

The ECB’s policy response: As said above, our European economics team expects more easing by the ECB on 10 March, in the form of a 10bp cut in the deposit rate (to negative 40bp) and extension of QE to September 2017. From a markets perspective, we think that both policies would increase asset volatility, and potentially backfire through a tightening of financial conditions. Investors see negative rates as detrimental for banks, and the extension of QE would fuel concerns over the scarcity of German Bunds – raising questions over the long-term viability of the present policy stance. For these reasons, we would look for possible shifts in the parameters governing QE along the lines described in a note published last week. ECB President Draghi indicated at the press conference on 03 December that the central bank would ‘revisit or review some of the technical parameters of the programme in the spring’. These would, on balance, lead to steeper curves in the core markets and tighter intra-EMU spreads – our base case – but whether they are delivered is uncertain.

To me, none of this makes sense. Any further easing by the ECB that is US dollar bullish just restarts the negative Mining GFC feedback loop cycle all over again.