Right on cue, The Australian’s Henry Ergas has penned another spurious defence of negative gearing.

Let’s take a look at his key howlers:

To begin with, prices of existing houses would fall as investor demand for properties declined. And since investors have accounted for a fifth to a quarter of purchases of existing houses, the falls could be material. Obviously, the greatest losses would be borne by those owning properties best used for rental, as their resale value would be savaged. Labor’s assertion that existing investors would not suffer from the change consequently makes little sense.

But it is not only investors who would feel the pain. Rather, since the decline in demand would affect the market as a whole, other homeowners would also be worse off. And the losses would loom largest for older Australians, as real estate (including the family home) accounts for 80 per cent of their net worth…

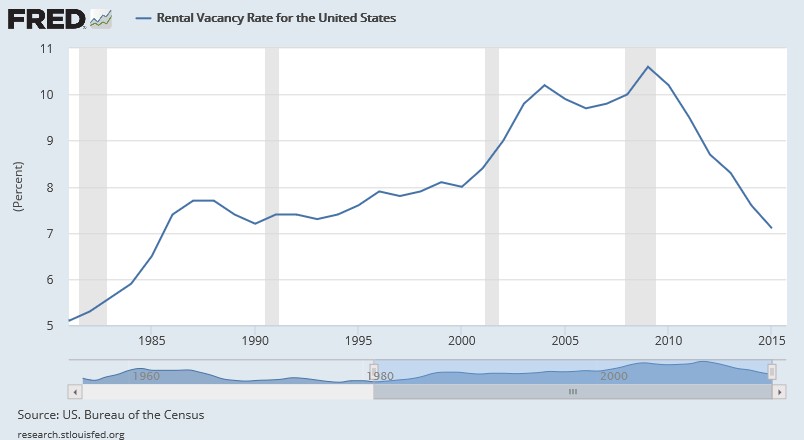

What is certain, however, is that renters would be substantial losers, as they were in the US when negative gearing was abolished. After all, if the supply of rental housing is to grow over the longer term, the return it generates cannot be much lower than it has been to date. But if the policy will cause house prices to increase less rapidly, as Labor claims, while capital gains tax rises, then after-tax returns can only be sustained by higher rents.

Let’s get a few facts straight.

The independent Parliamentary Budget Office (PBO) has estimated that the ALP’s property tax policy, which would restrict negative gearing to newly constructed dwellings and halve the rate of capital gains tax, could save the Budget $32.1 billion over 10 years. Thus, the ordinary taxpayer would be a big winner from this policy.

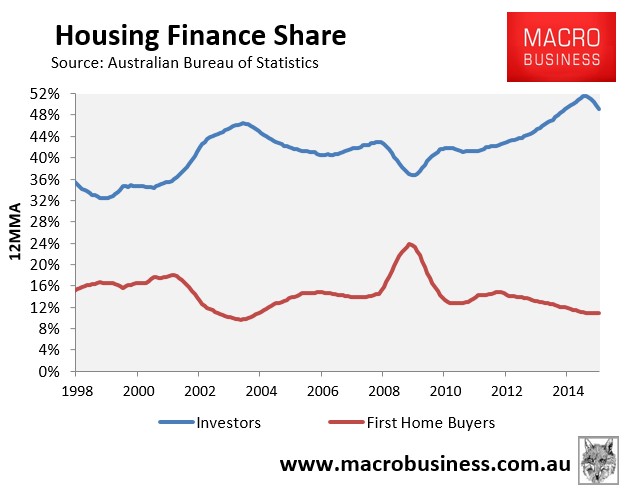

Second, the lower housing prices that the ALP’s policy produces would be a direct benefit to first home buyers, who have been crowded-out by investors speculating in pre-existing dwellings (see next chart).

Thus, what Ergas is essentially arguing is that more expensive housing is good, but more affordable housing is bad.

Third, Ergas’ argument that “renters would be substantial losers, as they were in the US when negative gearing was abolished” is plain false. The US abolished negative gearing in 1986, after which time the rental vacancy rate rose considerably. Only in the wake of the GFC, which caused a crash in dwelling construction, has the rental vacancy rate returned to its abolition level (see next chart).

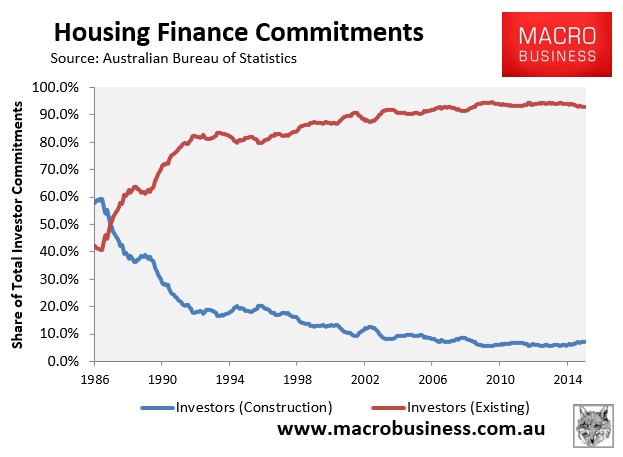

Back in Australia, Blind Freddy can see that negative gearing and the CGT discount in their current form have driven an explosion of investment in existing dwellings, not new construction (see next chart).

Hence, they have merely substituted homes for sale into homes for let, and not improved the rental supply-demand equation one iota. In turn, they have not lowered rents, as argued by Ergas.

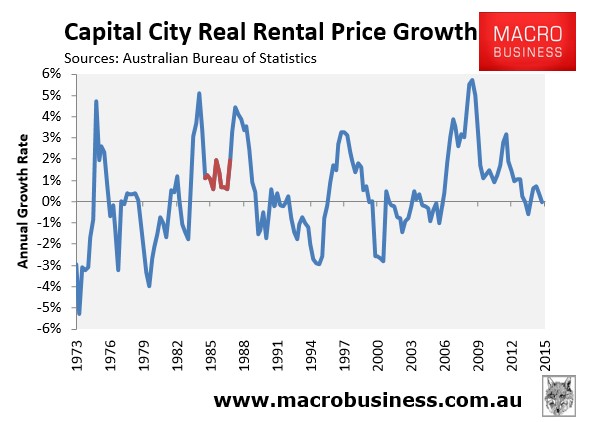

Moreover, the last time that negative gearing was quarantined – between 1985 and 1987 – real rents did not increase nationally (see red line in next chart).

And at the capital city level, real rents either fell or were flat in every capital city, with the exception of Sydney and Perth, where vacancy rates were particularly tight at the time (see here for the definitive evidence).

So why would rents magically rise under the ALP’s policy, especially when it actually boosts the supply of rental stock?