As the yuan tumbled during the past few weeks, Chinese consumers have been scrambling to change the currency for U.S. dollars, causing cash shortages at some mainland banks.

At major lender Industrial & Commercial Bank of China Ltd., one banker said the number of people wanting to change yuan for dollars has increased significantly during the past three weeks—a period during which the Chinese currency has declined about 2%.

During the weekend, ICBC received an urgent notification from China’s central bank warning of a dollar shortage, he said. The tight supply means ICBC customers applying to change yuan for dollars on Tuesday have to wait four days to complete the transaction, rather than the normal one day, he said.

…Harry Hou, who works in the financial industry in Shanghai, said he, his wife and parents bought their limit of $200,000 last year, and started buying dollars again through China Merchants Bank’s online service as soon as the New Year kicked in.

“This year’s biggest market risk is not going to be [stocks] but the yuan,” said Mr. Hou. “The government has let the yuan fall in the past, allowing it to weaken to 8 yuan from 5 yuan against the dollar in the 1990s.”

Maybe! After yesterday’s Shanghai rout, stocks sit only just above last year’s closing crash low:

Advertisement

MB remains of the view that the bubble will fully unwind below 2000.

Even so, Mr Hou is right that the yuan is a much larger issue. MB has been of the view that China will simply fail to hold up its currency as it continues to ease policy. But there are limits to that outcome for its “impossible trinity” too. From UBS via FTAlphaville:

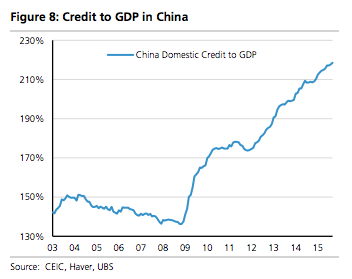

And here’s the thing – the factors that we believe have motivated the shift in currency regime [to a broader trade-weighted basket] are unlikely to change anytime soon. Weak international demand will likely keep a lid on export growth. Most importantly, lest we miss the woods for the trees, let’s remind ourselves that China’s key issue is that it is levering up almost at the same pace as it was 5 years back, when investors first started worrying about credit misallocation (Figure 8). The more levered the economy, the less effective countercyclical monetary will be. Clearly, then, all growth enhancing options need to be on the table. From a 2-3 year perspective, we do believe that the CNY can be considerably weaker than what forwards are implying.

Advertisement

Michael Pettis has more:

I have already described many times the self-reinforcing relationship between rising debt and slowing growth typical of the late stages of China’s investment driven growth model. As a larger and larger share of new debt is created simply to roll over the debt of borrowers who are unable to service their obligations out of the returns generated by the investment into which the credit had been directed, two things happen. First, in spite of what seems a rapid expansion in credit, there is likely to be very little liquidity in the system, and only the implicit guarantee of local or central governments prevents balance sheet mismatches from collapsing as liquidity becomes increasingly strained.

Second, assets and liabilities will become increasingly mismatched, and as balance sheet fragility inexorably rises, any change in government credibility or in the perception of government guarantees will cause large disruptions in the financial markets. One consequence of increasing balance sheet fragility will be that for all the talk of allowing defaults to occur, in the hopes finally of introducing discipline into the credit markets, any default that is credible enough to impose discipline also risks causing a disorderly re-pricing of the credit markets. That is why for all the talk every time another borrower is unable to service its debts, I very much doubt that Beijing will allow a major default to occur until it finally has no choice and can no longer prevent it.

A second consequence is that sharp disruptions will become a regular feature of the Chinese financial markets, although because each disruption will be followed by regulatory interventions aimed at preventing them from reoccurring, they are likely to pop up in unexpected places. When the shock to the interbank markets occurred in June, 2013, with overnight rates soaring officially to over 30%, and unofficially to as high as 100%, I promised my readers that there would be many more such shocks, although not necessarily in the interbank markets.

In short, China could be forced to hike interest rates instead of letting the yuan fall with very obvious and deeply negative implications for growth.

If so, precisely the same conundrum will confront Australia.

Advertisement

But let’s not be quite so bearish! Let’s assume the alternative scenario of easing policy and devaluing the yuan is sustainable coupled with reform to generate new growth drivers. As discussed yesterday, that will inundate the world with deflation and cause major disruption in commodity, forex and stock markets. But we can take it, right? Have some more Albert Edwards from Societe General:

I have always said that if inflating asset prices via loose monetary policy were the route to economic prosperity, Argentina would be the richest country in the world by now ?and it is not! The Fed?s pursuit of negligently loose monetary policies since 2009 is a misguided attempt to boost economic growth via asset price inflation and we will now reap the whirlwind (the ECB, Bank of Japan and the Bank of England are all just as bad). One of the main problems has been the overconfidence with which the Fed pursues their objective. Yet in the run-up to the 2008 Global Financial Crisis they demonstrated their lack of understanding of the disastrous impact of excessively low Fed Funds. Even in retrospect they remain in denial – as evidenced by Bernanke?s recent book. Why can?t these incompetents understand that they are, once again, the midwife to yet another global unfolding economic crisis? But unlike 2007, this time around the US and Europe sit on the precipice of outright deflation.

…I have always thought that in order to revive a spluttering Chinese economy, the authorities would have to devalue, but not just because an overvalued exchange rate was squeezing their manufacturing sector (e.g. sector nominal GDP growth of zero in Q3 2015). Instead I felt that an overvalued exchange rate had steadily undermined competitiveness to the point that it had undermined the balance of payments. This was compounded last year by an accelerated capital outflow as anti-corruption measures intensified, and an unprecedented unwinding of dollar-denominated borrowings by Chinese corporates. All these factors have combined to take the Chinese balance of payments into deep deficit.

The BIS and IMF have both shown that rapid growth of EM dollar-denominated debt over the past few years was mainly concentrated in the Chinese corporate sector (unsurprising after years of steady, carry-trade inducing, renminbi appreciation). Hence despite the Chinese economy being sucked into a deflationary quagmire ? best illustrated by a declining GDP deflator ? many dismissed the possibility of devaluation because of the likelihood that this dollar debt would cause substantial corporate bankruptcies.

That risk to the Chinese corporate sector was substantially reduced by the end of last year. The Institute of International Finance (IIF) recently reported a huge unwind of this debt.

This prescient action means that many Chinese corporates have taken the signal from the initial August devaluation seriously and readied themselves for further renminbi fall. Hence China is now in a better position to transmit a massive deflationary shock to the West without damaging its own corporate sector. Indeed we can already see US import price deflation intensifying as the decline in the dollar prices of goods from China accelerates.

…The western manufacturing sector will choke under this imported deflationary tourniquet. Indeed US manufacturing seems to be suffering particularly badly already.

I believe the Fed and its promiscuous fraternity of central banks have created the conditions for another debacle every bit as large as the 2008 Global Financial Crisis. I believe the events we now see unfolding will drive us back into global recession.

Valuation booms are followed inevitably by busts. But the key point is that these valuation bear markets take the Shiller PE back down to 7x or below.

Since valuations peaked at the most obscene level ever in 2000, we have only seen two recessions and at the nadir of the last one, in March 2009, the Shiller PE bottomed at 13.3x, way above the typical sub-7x bottom. In valuation terms the bear market was not completed in 2009 and indeed after only two recessions there was no reason to expect it to have been completed.

If I am right and we have just seen a cyclical bull market within a secular bear market, then the next recession will spell real trouble for investors ill-prepared for equity valuations to fall to new lows. To bottom on a Shiller PE of 7x would see the S&P falling to around 550. I will repeat that: If I am right, the S&P would fall to 550, a 75% decline from the recent 2100 peak.

As said yesterday, Albert is the uber-bear par excellance but his logic is sound even if we are too polite to agree with his price targets.

For Australia, then, China’s Chimerican unwind is a choice between death by deleveraging or death by deflation but, either way, its dirt export model is a dead duck.

Advertisement

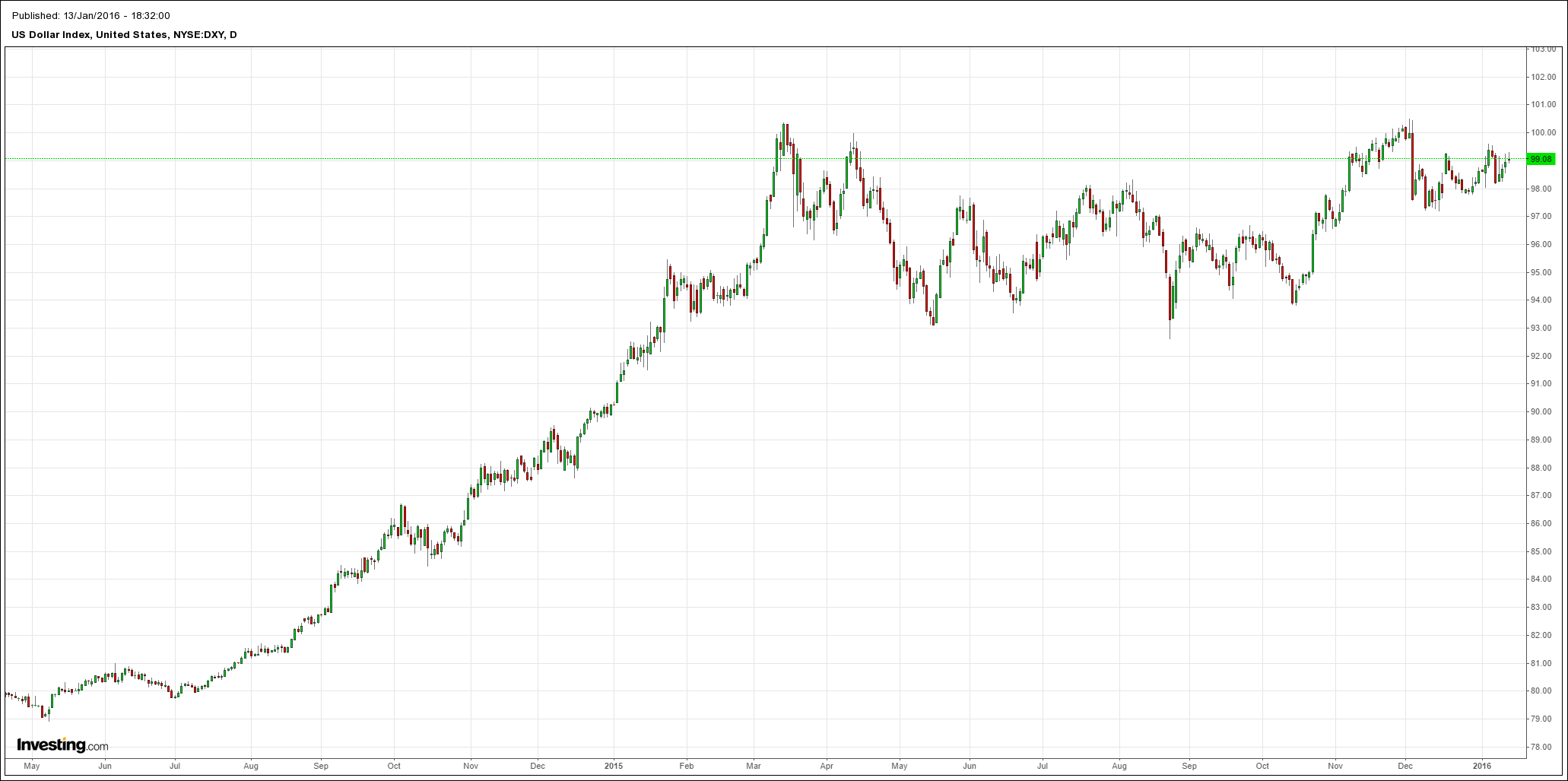

Today we’re are certainly still sinking with the latter as the Mining GFC intensified again and global stocks were hammered. The US dollar was strong:

Oil was pounded to all sorts of new lows:

Advertisement

Base metals were better on Chinese trade data though not copper:

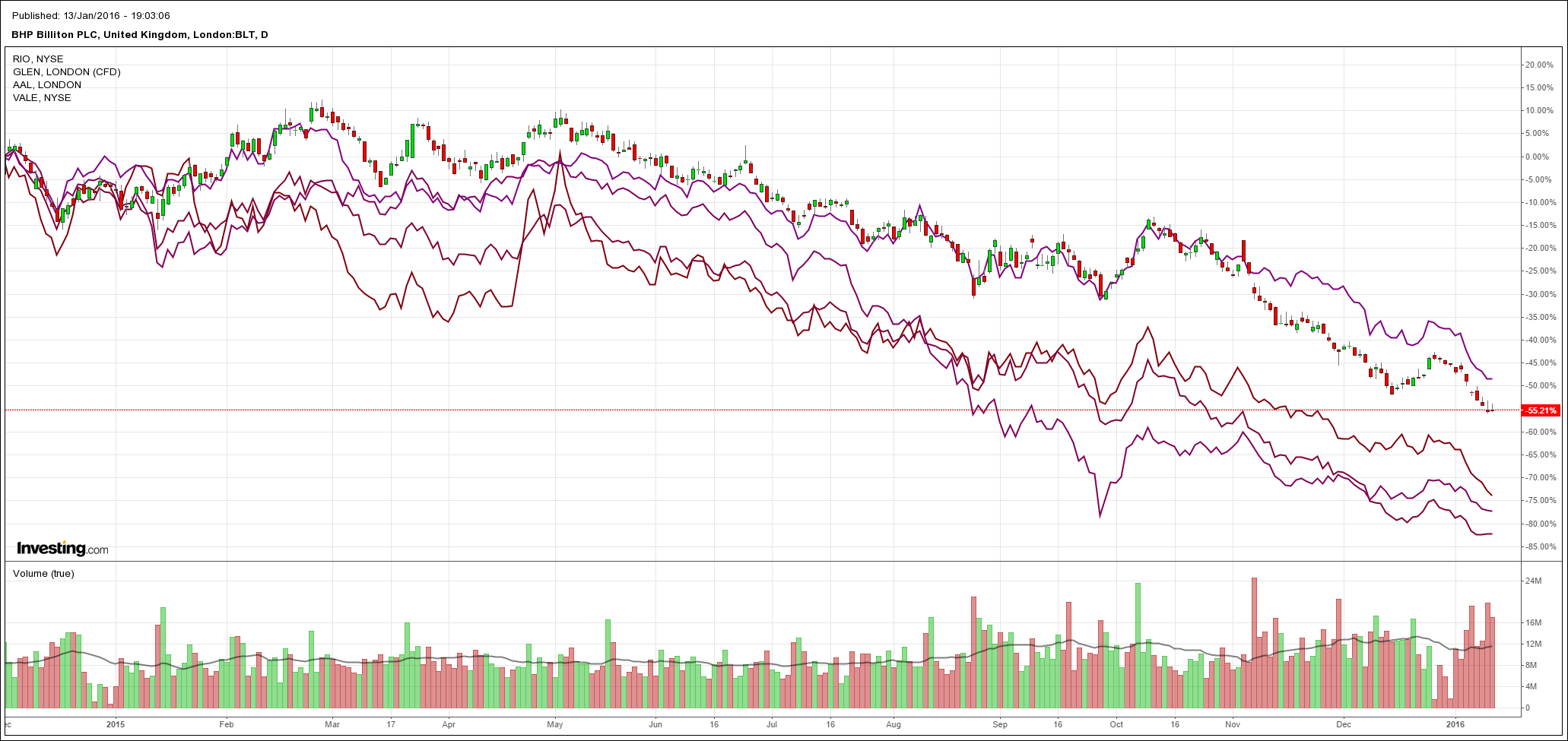

Big miners also caught a little break:

Advertisement

As did commodity currencies:

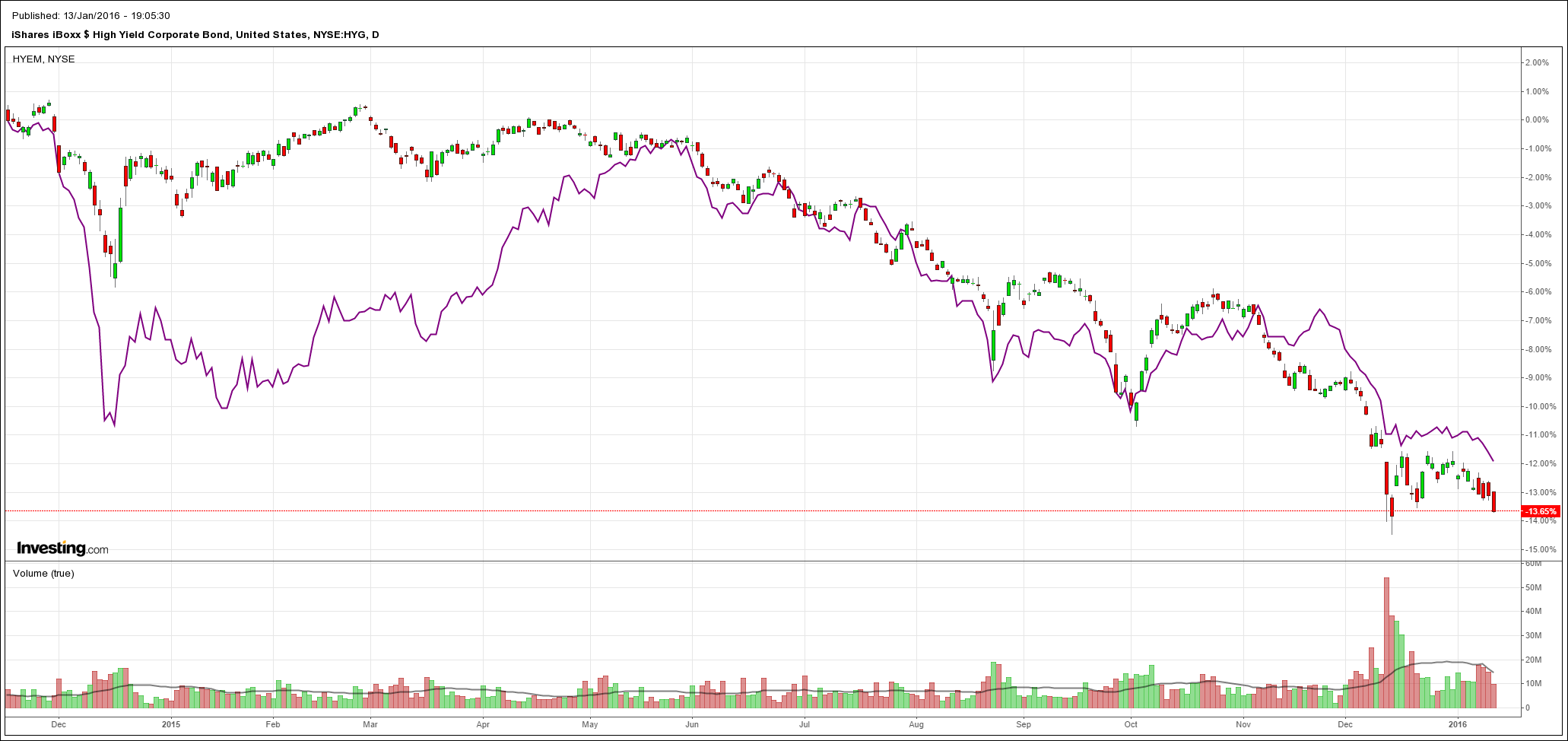

But US and emerging market high yield debt tumbled and the latter is in free fall again:

Advertisement

Importantly, this was on a day when Treasuries were bid, blowing out spreads. The Mining GFC is now running on its own internal logic. Fear is upon us.