The AFR has delivered yet another warning on how off-the-plan apartment buyers will look to bail-out of settling on their Sydney property investments in the new year, which could result in heavy losses for property developers:

“In 2015, we saw a lot of developments granted planning permission but I think heading into 2016 we will see them feel a bit of pain because some purchased their sites on such narrow margins,” said [Sydney estate agent Douglas Driscoll] who heads real estate network Starr Partners.

“As market levels fall away slightly, some developers might struggle to cover costs.

“Towards the end of 2016 we might start to see some investors potentially walk away from their deposits because they perceive that they paid too much for it in 2015 and see that it’s no longer worth the risk,” he said…

“Going into 2016, mortgage lenders will start freezing out investors, as lenders actually don’t have an obligation to provide the finance. They will simply say that they can’t provide the finance on the original terms (say, a five per cent deposit) and that now much more is needed”…

The ‘funding time bomb’ facing some off-the-plan buyers was explained beautifully by Ross Elliott back in July:

Think of the investor who’s been sold the story of a generational shift to inner city apartment living. They see demand rising for this type of product and lifestyle and figure that this is a good market to buy into. They purchase a $500,000 unit ‘off the plan’ with a $50,000 deposit, when the banks are happy to lend 90% of the value…

Fast forward three years to settlement time. The banks are no longer prepared to lend 90% but our investor’s bank will still lend to 80% of the valuation. That valuation has come in a few months before settlement and the bank now has a piece of paper that says the home unit is worth $450,000. Values have fallen because there is a very large volume of similar stock on the market at the same time, in roughly the same location, and there are more sellers than buyers.

So as far as our investor’s bank is concerned, they will now lend 80% of $450,000, which is $360,000. The investor now needs to fund the remaining balance of the contract price of $450,000 ($500,000 less his deposit). So our investor needs to find another $90,000 to make the settlement. They could walk away and lose their deposit, or they could try argue their way out of the contract, but both aren’t exactly appealing options.

They could sell the apartment but that would mean taking a loss in that market. They could rent it as planned but vacancies are high (there’s a lot of similar product out there) and rents have fallen (supply over demand). So their return on renting is nothing like they imagined it could have been. Plus, by now, interest rates have risen so the gap between the rental income and the repayments is much wider than they banked on. It’s called ‘negative’ gearing for a reason but there’s a limit to how much most people can lose.

If our investor decides to sell and realises $450,000, they still have their transaction costs to take into account so their net realisation may be closer to $400,000 on the ins and outs of the deal. They can pay out their $360,000 loan and have $40,000 left. This looks pretty ordinary if they had to sink $140,000 of their own savings into the deal. That $140,000 is now worth $40,000 – not including any losses on the cash flow if they’ve been renting it (or trying to) for a time.

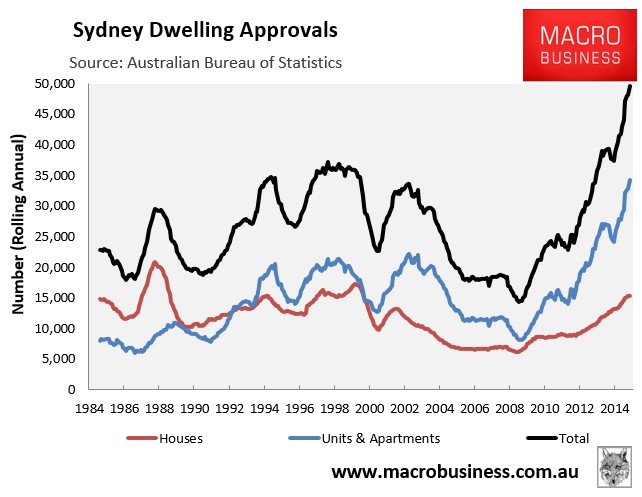

Investors in Sydney should be getting very nervous given the unprecedented volume of apartments recently built, currently under construction, and planned:

As I have argued previously, anyone that is willing to pay $700,000-plus for a cookie-cutter two bedroom apartment in Sydney deserves to lose money.

Most of these properties have few redeeming qualities. They are generally small, bland, and subject to expensive body corporate fees. They are also unsuitable for families, which limits the buyer pool to foreigners, young couples, empty-nesters and students.

Another problem with purchasing off-the-plan apartments is that once they have been lived in, and become “used”, they no longer qualify for first home buyer subsidies nor sale to foreign buyers, since they are generally restricted to newly constructed dwellings only. This effectively reduces their resale value.

In short, steer well clear of these money black holes.