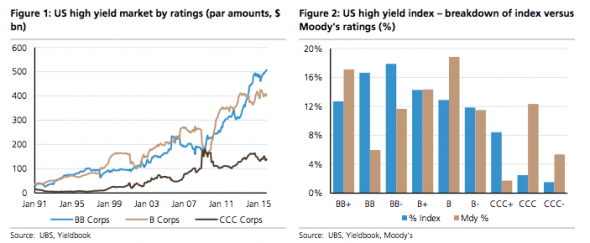

The fallacies of this approach are that ratings competition actually favors issuers as it results in more aggressive credit ratings2, and deterioration in credit ratings is glacial and lagged versus prior cycles. For example, the proportion of triple C issuers in the Citi US high yield cash bond index is currently 13%, appearing in-line with the average triple C proportions in the prior cycle. However, since index rating criteria now typically utilize the middle classification of the three agencies3, this could be biased. If we instead utilize Moody’s ratings – the more conservative rating for a majority of the ratings – the proportion of triple Cs increases to 20% (Figure 2). And this is not a function of changes in rating methodologies with respect to incorporating loss in default ratings. According to Moody’s not only has the number of single B and triple C issuers surged post- crisis, but the proportion of issuers by count rated triple C is at all-time highs (27%, Figure 3). Note this figure would include high yield bonds as well as leveraged loans, the latter of which has been under particular scrutiny from the Fed due to elevated credit risk and poor underwriting concerns.

Given that cash flow measures are also subject to significant variation, particularly when funding costs are rising and capital market access is declining, the reality that median net leverage for single B issuers is back at late 1990 levels should be troubling, given corporate earnings and margins are also above trend (Figure 4). Equally worrying, the post-crisis theme of HY companies issuing or refinancing debt at lower and lower interest rates has almost certainly ended (Figures 5 & 6). Lastly, many investors may forget, but a few may recall, that cumulative default rates were actually much worse in the late 1980s and 1990s than they were in the financial crisis (Figure 7) – and much of that is predicated on the origin of the credit growth and excesses. We would posit that non-financial corporate credit is at the nexus of the excesses in this cycle, unlike in 2007-2008 which was centred on the US housing sector and the banking system. This does not bode well for future long-term cumulative corporate default rates.

In total, we would posit that roughly 35 – 40% of the outstanding US high yield and leveraged loan universe is at risk (not including any emerging market exposure). Based on the size of the US high yield cash bond and leveraged loan indices, which total approximately $2tn in debt outstanding, that would imply $750 – 800bn in low quality speculative grade debt. However, exact figures of the size of US speculative grade debt vary 6 . According to a recent S&P study US speculative grade entities could have as much as $4tn in debt outstanding (if one includes bonds, loans, and revolving credit facilities assuming fully drawn7) – with about one-third maturing through 2020 (Figure 8). In short, indices understate and the rating agencies overstate the amount of debt coming due, so we’ll take the middle ground which implies roughly $1.05 – 1.2tn in low quality speculative grade debt outstanding.

…Some may argue the Fed is pursuing the right policy, in that the alternative is for leveraged loan markets to overheat further. While that may be accurate the lesser evil is still evil; low quality speculative grade issuers do not organically delever – they only do so through earnings growth, and given above trend earnings and elevated leverage the prospects for such an outcome are slim. They cannot pay down debt because cash flow generation is weak, and now interest costs are rising. Sothe Fed is explicitly condoning rising default rates. Finally, it is our humble belief that the consensus at the Fed does not fully understand the magnitude of the problems in corporate credit markets and the unintended consequences of their policy actions. The implication is that their actions will be reactive, not proactive – but only time will tell…

The real risk posed by illiquid credit markets is the interaction between liquidity and default risks; namely, as an issuer’s fundamental prospects deteriorate, secondary market liquidity declines as dealers pull back, and default risk rises as equity holders face larger losses in refinancing maturing bonds. This can become a vicious cycle as plunging bond prices correlate with falling equity prices, sending further market signals of stress and further complicating refinancing prospects. It is this scenario which we have consistently feared for lower-quality credits; i.e., a liquidity ‘crunch’ exacerbates deterioration in fundamentals and creates a self-fulfilling prophecy – but on a broader scale.

The leading edge, and driver, of this credit deterioration is the $200 billion or so in junk bonds issued to US shale and, alas, there is little doubt that it is going to get worse as the Fed tightens.

Advertisement

Contagion is already sweeping highly leveraged commodity producers globally, both private and sovereign but so far it is relatively contained to specific problems such as US shale or Brazil.

I suspect that it’s not going to remain that way for very much longer. Using a Global Financial Crisis analogy, the Minsky moment occurred in August 2007 when French bank BNPBaribas declared ‘the complete evaporation of liquidity in certain market segments of the US securitisation market has made it impossible to value certain assets fairly regardless of their quality or credit rating’.

This time around it will not be banks that are at the heart of the debt freeze but miners via bond markets. The good news is that that means it won’t literally be a “freeze”, rather a steady rise in marginal bond rates until all miners alike are felling the pain regardless of ratings a credit quality. At some point I expect that to trigger some kind of Bear Stearns event when a large private firm – like Glenore – defaults or goes under.

Advertisement

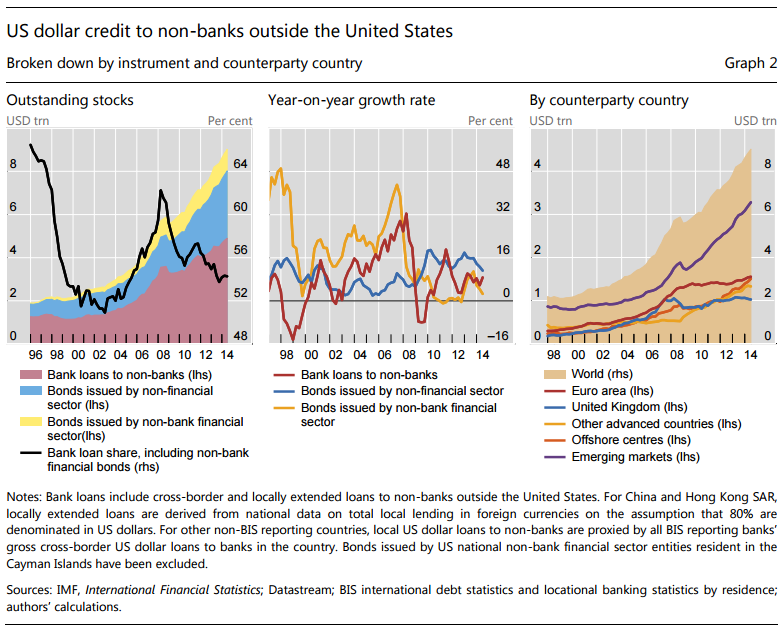

But that may not be the end of it, either. The Lehman moment is more likely to come some little time later when a sovereign defaults – perhaps Brazil or Russia or who knows who. The BIS illustrates the risk:

The risk is that when that $7 trillion or so in emerging market US dollar denominated borrowings begins to unravel at the margin, we will see a self-fulfilling dash for US dollars as everyone seeks to repatriate US dollar debt simultaneously. If so, we will enter a self-fulfilling crisis of US dollar rises blowing up more US denominated debt in un-dollarised economies as the world find itself acutely short of dollars.

Advertisement

It’s not another GFC but it is, in effect, the Asian Financial Crisis gone global for commodity producers.

David Llewellyn-Smith is Chief Strategist at the MB Fund and MB Super. David is the founding publisher and editor of MacroBusiness and was the founding publisher and global economy editor of The Diplomat, the Asia Pacific's leading geo-politics and economics portal.

He is also a former gold trader and economic commentator at The Sydney Morning Herald, The Age, the ABC and Business Spectator. He is the co-author of The Great Crash of 2008 with Ross Garnaut and was the editor of the second Garnaut Climate Change Review.

condoning rising default rates. Finally, it is our humble belief that the consensus at the Fed does not fully understand the magnitude of the problems in corporate credit markets and the unintended consequences of their policy actions. The implication is that their actions will be reactive, not proactive – but only time will tell…