The jobs euphoria is widespread today. It comes from the top, from The Australian:

The Prime Minister yesterday hailed the drop in the jobless rate as evidence Australia was adjusting to the end of the mining boom, while acknowledging that the monthly figures “bounce around”.

“The economy is in transition and it is transitioning very well,” Mr Turnbull told the Knowledge Nation 100 event in Sydney, co-sponsored by The Australian.

He said the fall in the jobless rate to a 19-month low was the result of the entrepreneurship and innovation of millions of Australians who were seizing new opportunities. “The mining boom may have receded … but the ideas boom is the boom that can continue forever; it is limited only by our imagination and our commitment,” he said.

Lot’s of economists and journalists follow the line and it seems unnecessary to repeat it. I would very much like to believe in the spectacular job gains but alas I cannot. Despite the hoopla, the truth is that the economy is not improving, that interest rates have not bottomed, that the Budget is descending into crisis, that the currency will continue to fall, and that we will all continue to get poorer. How can I be so sure of this?

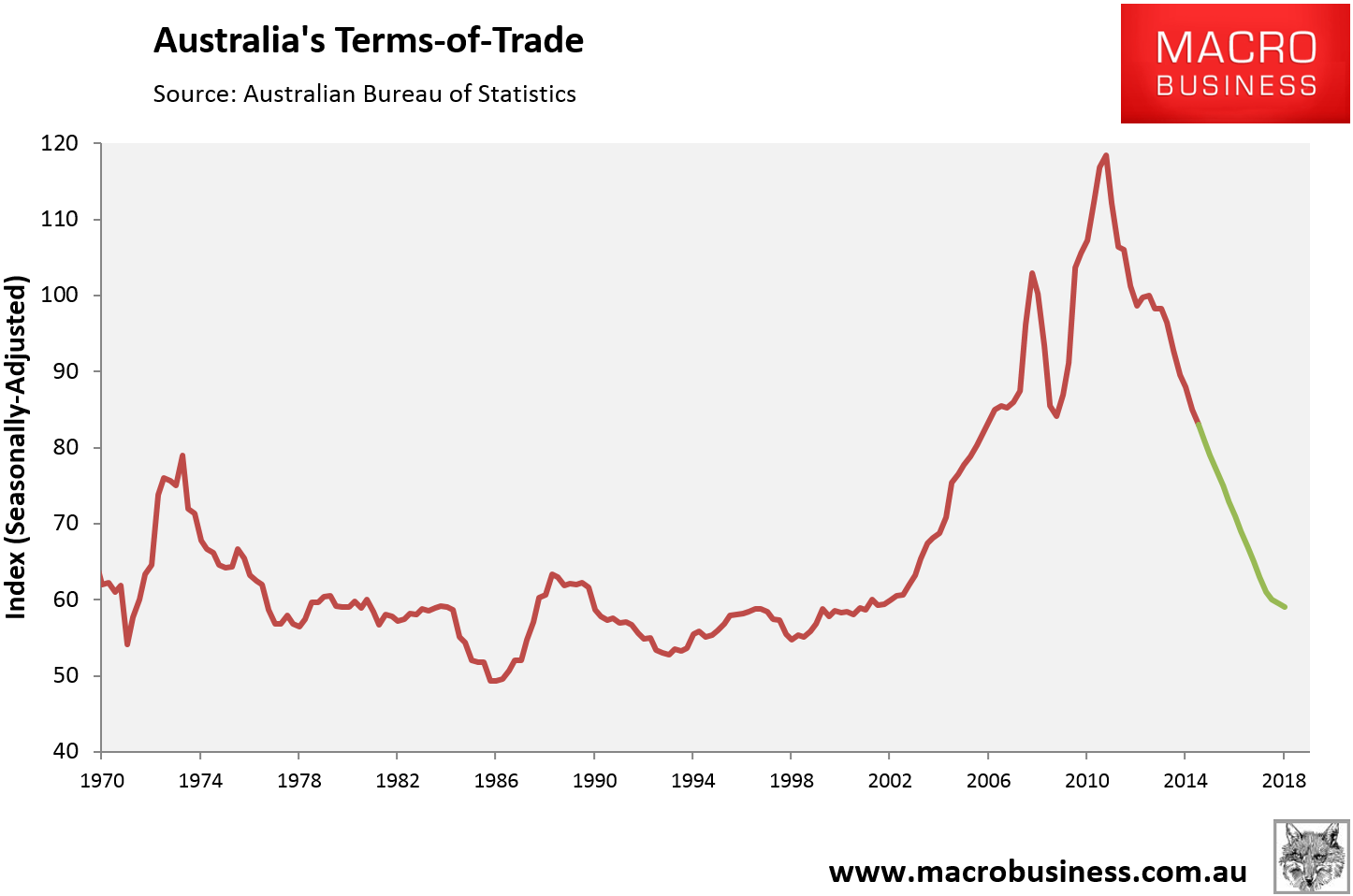

Well, you can read our special report on the matter to understand everything going on but the one key fact, the incontrovertible brick wall into which we hurtling, the cracked key stone of our exceptionalism, the liquefying bedrock of our foundations, has not changed and is getting worse not better. It is the iron ore price.

Why is this so important?

The iron ore price makes up one third of our terms of trade. With coking coal (which is pretty much part of the same trade) it is nearly half. It is iron ore that gave us the mining boom and it is iron ore that is taking it away. But we’re “rebalancing” the hopeful yell! Alas, we are not. National income is the key measure of our standards of living and it continues to fall along with iron ore. In the absence of income growth, we are leveraging not rebalancing, so that we can pretend for a little while longer that we are getting richer.

To understand this consider how the Australian economy functions. We derive income from the world largely via selling dirt. The most profitable dirt by far is iron ore. Even today, the vast majority of iron ore is immensely lucrative. That mining income is harvested by equity markets for dividends, by governments via higher corporate taxes, and by households via lower taxes and higher wages.

We then take that income and leverage it in global markets by borrowing heavily and dumping that money into super large mortgages. That is really all the Australian economy is, a giant iron ore securitisation product. If you add the Chinese leverage driving iron ore demand then we become a collateralised debt obligation. We don’t grow income via productivity and only painfully slowly via other exports. Thus the huge services economy cannot grow without the iron ore income and/or the leveraging to drive rising house prices. It is its lifeblood, as we saw in the 2010-11 period.

The key question, then, for the ‘rebalancing’ is not whether employment is growing or not in any given month or quarter, it is can the lost income be replaced and if not how much longer can you leverage up in the face of the falling income? Authorities have already shown their hand that they know the limit is near by overlaying low interest rates with macroprudential tools and running overly tight fiscal policy in the circumstances.

And the shelf life of the pretense is shortening every day as iron ore falls. As this stage of the illusion, nobody has priced where iron ore is today, let alone where it is going. Equity markets still have an average price of $50 embedded in analyst models. Ratings agencies are the same. Government budgets are assuming $55. All as well see the iron ore price rising into the future from here.

But iron ore is not going to average that next year. $35 is a better bet for 2016. $25 for 2017. $15 for 2018. With any recovery far away.

As a result Australia’s terms of trade will keep falling, all the way back to 2002/3 levels, if not lower:

And so, we will be able to do only a few things in response. We can increase leverage again and/or we can boost productivity and/or exports to substitute some of the lost iron ore income. There is nothing else.

There is not much hope of us achieving higher productivity growth. The political economy is so paralysed by vested interests that it is nigh on impossible. That leaves us with non-iron ore exports which are growing slowly but nowhere near fast enough as an income offset. LNG might have done it but it is an income black hole for as far as the eye can see. Thus as iron ore keeps falling next year we will again be forced to cut interest rates to both boost leverage and lower the dollar chasing more non-iron ore export growth.

We’ll probably be able to do this without facing the consequences until markets seize up again in the next global shock. Though as we record in our special report, we do not think that it will achieve much given the limited scope for further leveraging is now pretty obvious to all.

Once the end of cycle event comes, and the world accepts that iron ore is forever stuck at $20 and below, then the great superstructure of leverage that we have built upon the $120 iron ore price floor will also tumble.