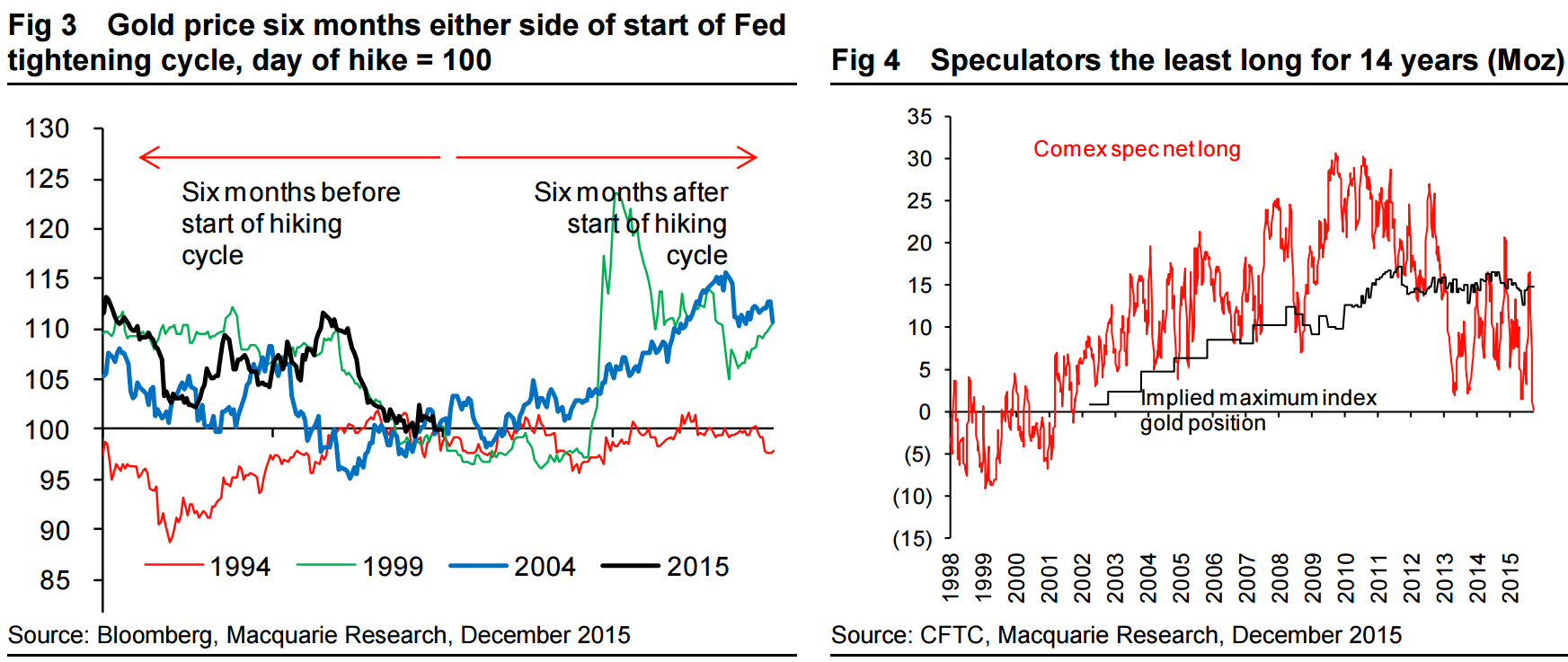

The evidence from previous episodes of when the Fed has began hiking is mixed. As fig 3 shows of the last 3, which were in 2004, 1999 and 1994, gold ended up higher on two occasions and lower on one. On the two it ended up higher, 1999 and 2004, it also fell quite sharply into the decision, whereas in 1994 it actually gained (perhaps explained by 1994 being more of a shock). But the usefulness of these historical examples is limited by their being so few, and over such a long time period during which much about the gold market and wider economic and financial markets has changed – hence our preference to use the recent 2013 tapering episode.

What could spark a rally this time? One characteristic of the gold market that has seen the price turnaround before is when speculators get overly short. Certainly at the moment by historical standard speculators are pretty short (and to be fair with good reason). On the Comex futures market the non-commercial net long position, the historical main measure of speculation, reached on 2 December its lowest for 14 years (see fig 4 overleaf). While it is still (albeit marginally) net long we remain of the view that the dataset is somewhat misleading as it likely includes some passive index fund positions (see ‘Are gold specs on Comex net short’?), and therefore actual speculators are probably net short by some margin.

But a short market is a necessary, not a sufficient condition, for a bounce. The ‘sufficient’ tends to come from events. In 2014 the 1Q rally was driven by weaker-than-expected US growth on poor winter weather, fears over China, and geopolitical tensions (then Ukraine). The first of these seems unlikely this time around given better weather and the poor comparables of 1Q 2015 (also hit by the winter weather), but the second and third clearly remain key possibilities, and it is in the nature of ‘events’ that they are hard to identify1 .

Our main argument for gold seeing a post-Fed bounce though has been and remains a psychological one. The forthcoming Fed rate hike has been a Damocles sword hanging over the market since at least November 2014, when QE was finally stopped, and in some ways all the way back to January 2013, when the direction of Fed monetary policy changed from greater easing to a slow tightening. We have spoken to investors who have seen positive reasons to invest in gold but were afraid to do so because of the fear of what would happen when rates went up; we doubt this was an uncommon view. That the rate hike is now in the past could restore some confidence, and coupled with the short futures positioning, we see the possibility of bounce in 1Q 2016 back over $1,100/oz in line with the 2013 price move.

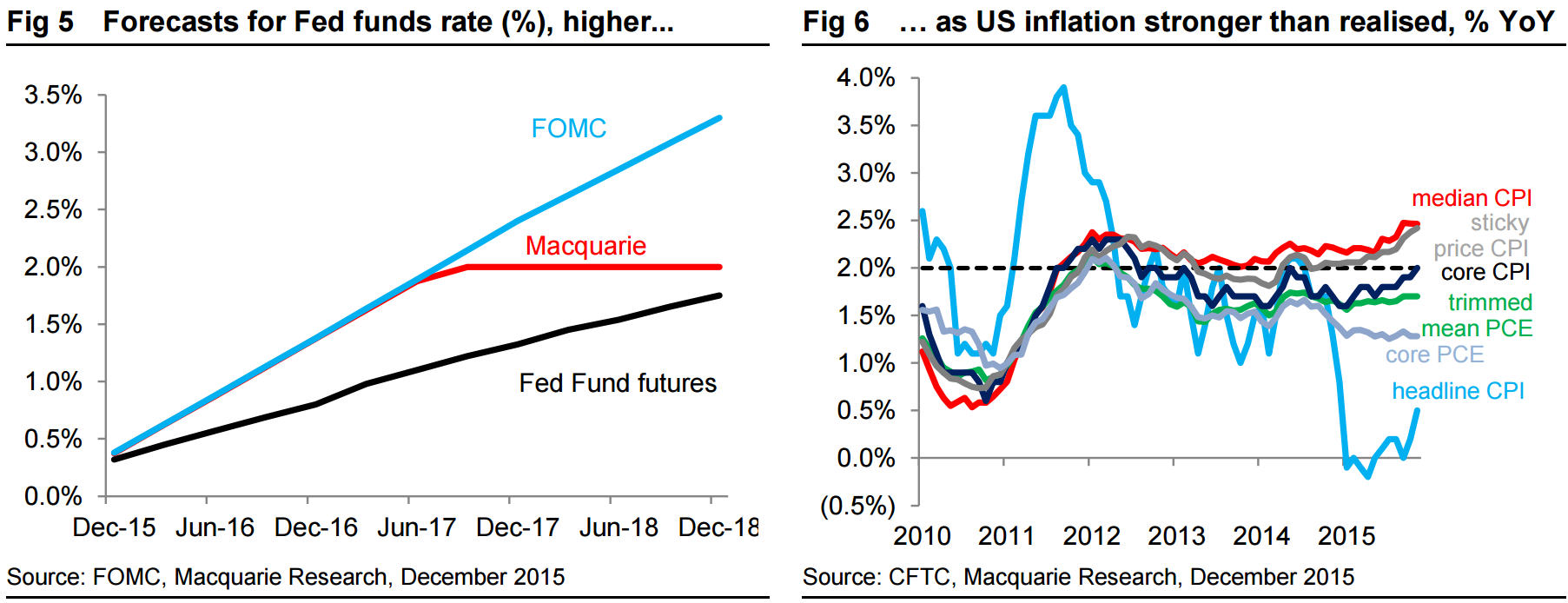

Of more importance though is the medium-term outlook, and for now the most important determinant of that is how investors perceive the hiking cycle. We are hawkish on rates, at least until 2017, compared to futures’ markets expectations and so is the Fed. This presents clear and obvious dangers to gold and mid-year could see it back to its lows. But if, as we believe, the ultimate reason rates are increased is because core inflation is firm and headline inflation rising, then US real interest rates are likely to fall. This should take the sting out the hiking cycle and given some improvement in ‘fundamentals’ allow moderate price gains.

Lordy, I find that unconvincing! If gold bounces after Fed rates I would take it as another signal that the tightening is a policy mistake and that the yellow metal is discounting a reversal in the US dollar on further easing.

In the medium term the outlook for gold remains good, depending upon what kind QE we get next time around from the Fed. If it is negative interest rates or some other form of leveraging QE, which appears to be the base case, then gold will boom. If they wake up to themselves and instead embark on a deleveraging QE, such as directly monetising tax cuts or infrastructure investment then it would not be so good.

Remember that gold is all about the US dollar and the stability in its settings.

David Llewellyn-Smith is Chief Strategist at the MB Fund and MB Super. David is the founding publisher and editor of MacroBusiness and was the founding publisher and global economy editor of The Diplomat, the Asia Pacific's leading geo-politics and economics portal.

He is also a former gold trader and economic commentator at The Sydney Morning Herald, The Age, the ABC and Business Spectator. He is the co-author of The Great Crash of 2008 with Ross Garnaut and was the editor of the second Garnaut Climate Change Review.