A plunge in the US manufacturing PMI in November has taken our global manufacturing PMI measure to its lowest in over two years and on the brink of recession.

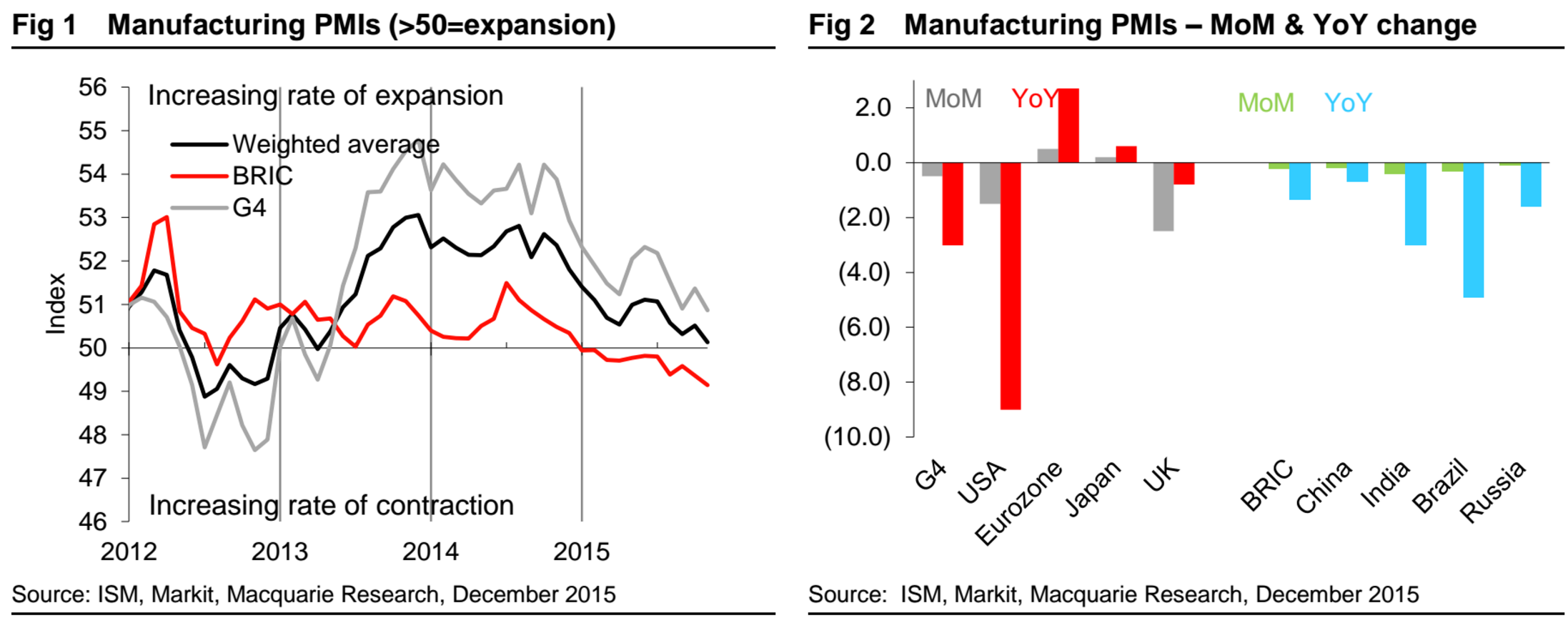

In November our aggregate manufacturing PMI for the leading industrial powers1 50.5 in October (fig 1). This is barely above the 50 mark which denotes contraction/expansion, and is the lowest reading since April 2013. The main driver of the fall MoM was a sharp reduction in the US, but most regions declined, though two exceptions were the Eurozone and Japan. The same two are the only regions with a YoY increase; most others suffered a substantial fall.

Global manufacturing is clearly in a bad way. The big question for metals demand, of which we believe manufacturing is a key driver, is to what extent that’s the bad way we know about or that there is worse to come? Our normal comparison is between the aggregate PMI and YoY global IP growth (fig 3). This points to a further slowdown in YoY IP growth in coming months, from 1.7% to, say, 1.6%. This however isn’t that surprising – Q4 2014 saw a relatively rapid 0.9% growth (3.8% annualised) – see fig 4 – and even moderate growth in 4Q 2015 would see YoY growth decline in line with the PMI data. So the PMI is perhaps not painting as bearish an outlook as one might surmise from the headline, though it is still pretty bearish.

In short, weak industrial production and metals demand, everywhere.

David Llewellyn-Smith is Chief Strategist at the MB Fund and MB Super. David is the founding publisher and editor of MacroBusiness and was the founding publisher and global economy editor of The Diplomat, the Asia Pacific’s leading geo-politics and economics portal.

He is also a former gold trader and economic commentator at The Sydney Morning Herald, The Age, the ABC and Business Spectator. He is the co-author of The Great Crash of 2008 with Ross Garnaut and was the editor of the second Garnaut Climate Change Review.