Iron ore has today sunk to $48.70. Joe Hockey’s last Budget forecast for this year was $48FOB. To bring it up to the CFR benchmark equivalent one must add freight of $6-8 so his actual number was more like $55.

So far this year the price has averaged almost exactly $55 but that is about to change with more falls ahead, no end of year restocking and big new supplies about to hit the market. Next year iron ore is going to average $45 and the year after that $35 and the year after that $25.

So, as Prime Minister Turnbull mulls his first mid-year economic update (MYEFO) and frames his Budget for next year as well, at the forefront of his thinking needs to be how he is going to manage massive further writedowns to his revenue outlook. He has two choices about how to go about this.

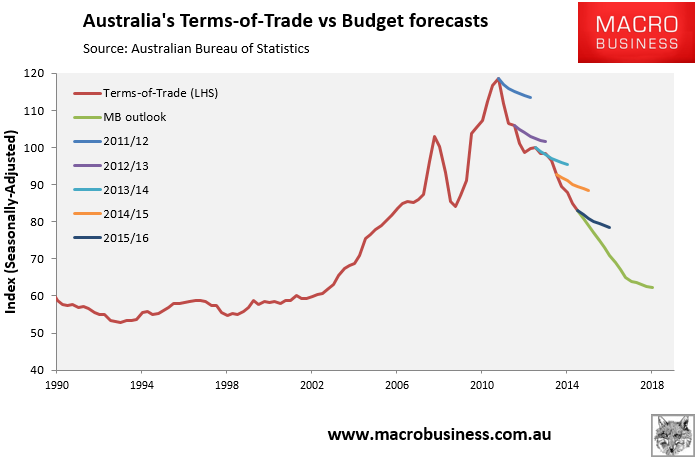

First, he can do what every government has done before him and kid himself (or outright lie). He can follow the disastrous analysis at the Office of the Chief Economist (formerly BREE) which sees the iron ore price miraculously rebounding to $70 in future years, and plan his entire agenda around a fiction that steadily falls apart. The following chart captures the history of said approach:

The outcome of this path is predictable. As the Budget misses its outlook again, and again, then again, wider confidence will suffer the same fate that it has under four successive prime ministers and then it will to turn to anger directed at the government that failed to anticipate it. If Turnbull takes this path he is effectively committing to spend his political capital on life support for the current dying Australian economic model as it coughs its last, taking his political legacy with it.

The second approach that Prime Minister Turnbull can take is to be honest with the Australian people and put appropriate iron ore forecasts in his Budget. To do that he will need to explain in detail that the Chinese economic adjustment is structural and permanent, that Australia’s post-mining boom adjustment is equally lasting and challenging, and that to get through it without severe pain we are going to need to share some more managed pain up front.

That pain need not be couched as the ‘doom and gloom’ found so abhorrent in the national discussion these days, it needn’t even hold the myriad blunders of business and bureaucrats to account for getting us here, it simply needs to explain that the mining boom is over forever and that we will need to work for our supper in the years ahead. This will mean no pay rises, higher taxes, more public investment than we are used to, and difficult tax reform including to property and superannuation giveaways. The PM’s innovation agenda is also good, if far too small to carry the load.

The agenda is hard, yes, but it is the only way to govern beyond a single term.