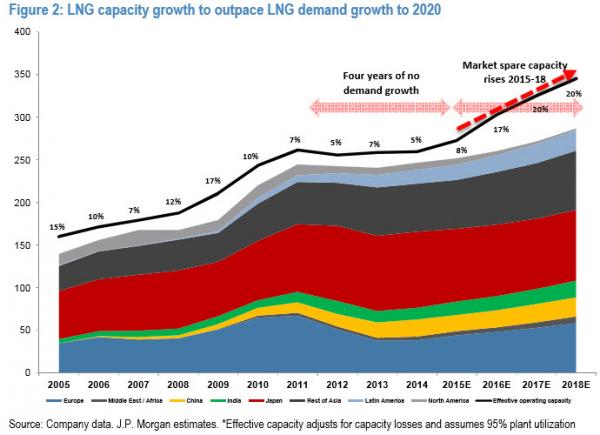

All participants shared a cautious view on near-term demand trends, with Japan and South Korea likely flat to down and China gas demand growth having slowed this year. In Japan, population and economic trends are the main driver of lower electricity demand growth, with some nuclear facilities expected to restart that will initially lead to fuel switching away from burning oil products, then eventually coal and LNG, if enough reactors start back up (Tepco guided 1GW nuclear plant reduces LNG demand by 1.2mtpa). KOGAS believes LNG imports will decrease in South Korea next year owing to coal and other commodities being cheaper and could see a stagnant demand period from FY17.

The full text of this article is available to MacroBusiness subscribers

David Llewellyn-Smith is Chief Strategist at the MB Fund and MB Super. David is the founding publisher and editor of MacroBusiness and was the founding publisher and global economy editor of The Diplomat, the Asia Pacific's leading geo-politics and economics portal.

He is also a former gold trader and economic commentator at The Sydney Morning Herald, The Age, the ABC and Business Spectator. He is the co-author of The Great Crash of 2008 with Ross Garnaut and was the editor of the second Garnaut Climate Change Review.