From Mining.com:

While miners are holding off on new projects and looking to slow the completion of ones in the works as they face the worst commodity price collapse since 2008, research house Wood Mackenzie warns the industry could be paving the way for a major supply shortage.

In a presentation prepared for clients at LME Week in London, the firm’s vice chairman of metals and mining research, Julian Kettle, draws together the overall outlook for metals, citing the challenges of lower commodity prices, pressure from shareholders to curtail investment and a new reality of lower demand growth. Wood Mackenzie concludes that if the industry fails to invest the US$150 billion required to meet future supply needs, looming supply shortages will follow.

“The need for investment is becoming desperate in zinc and lead and will be an issue in copper in the next few years,” Kettle writes. “Unfortunately there is little appetite to invest with prices cutting into the cost curve, low free cash-flow, surpluses building, difficulty in financing and shareholders demanding dividends.”

Supply shortages, hmm perhaps, but then again maybe not.

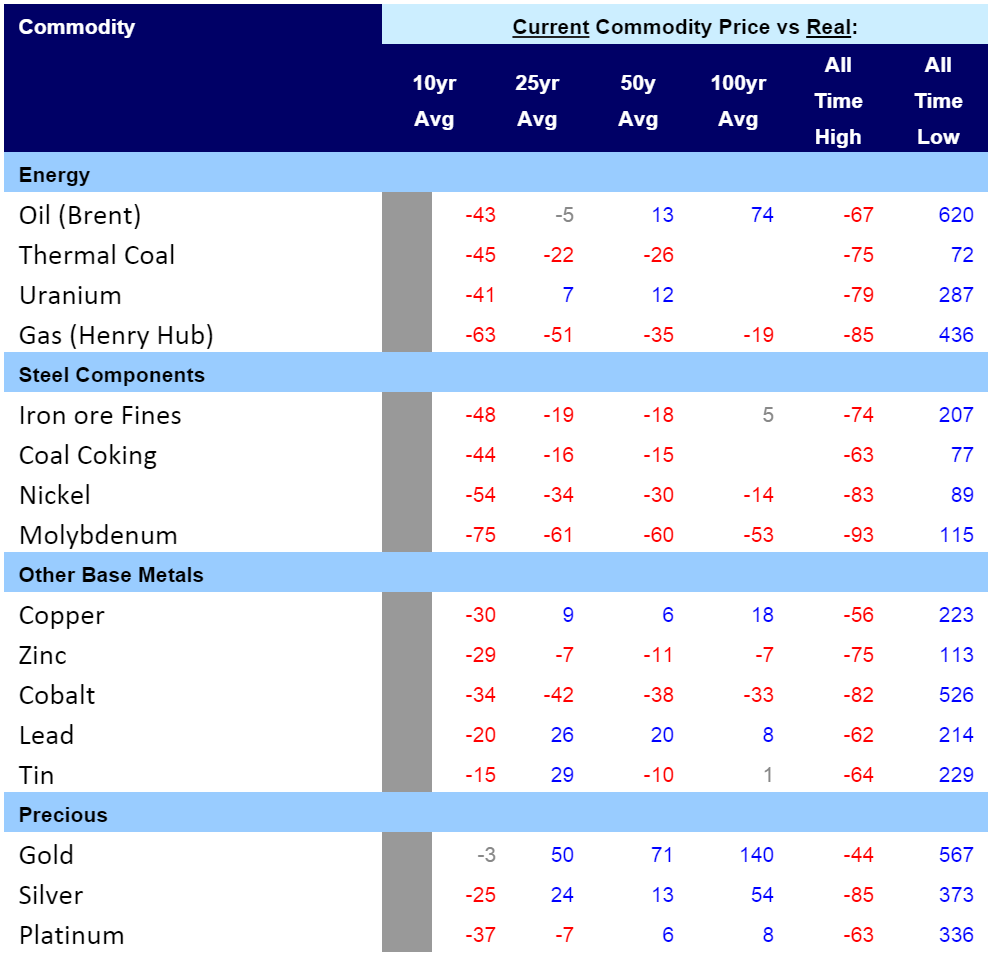

I’ve put together a 100 year table of all major hard commodities to see what it looks like in terms of real (inflation adjusted) prices over the last century (using data from the US Geological Survey and adjusted with the US GDP deflator):

The table shows the percentage by which today’s metals prices have deviated from real, long term averages. As you can see, everything looks cheap as chips in comparison to the 10 year average price. A majority still look cheap over the 25 year average. At the 50 year average it starts to even out and against the 100 year average the balance is even. Against all time highs, prices have crashed. But the money column is actually the last one. Against all time lows, we are still soaring in every commodity.

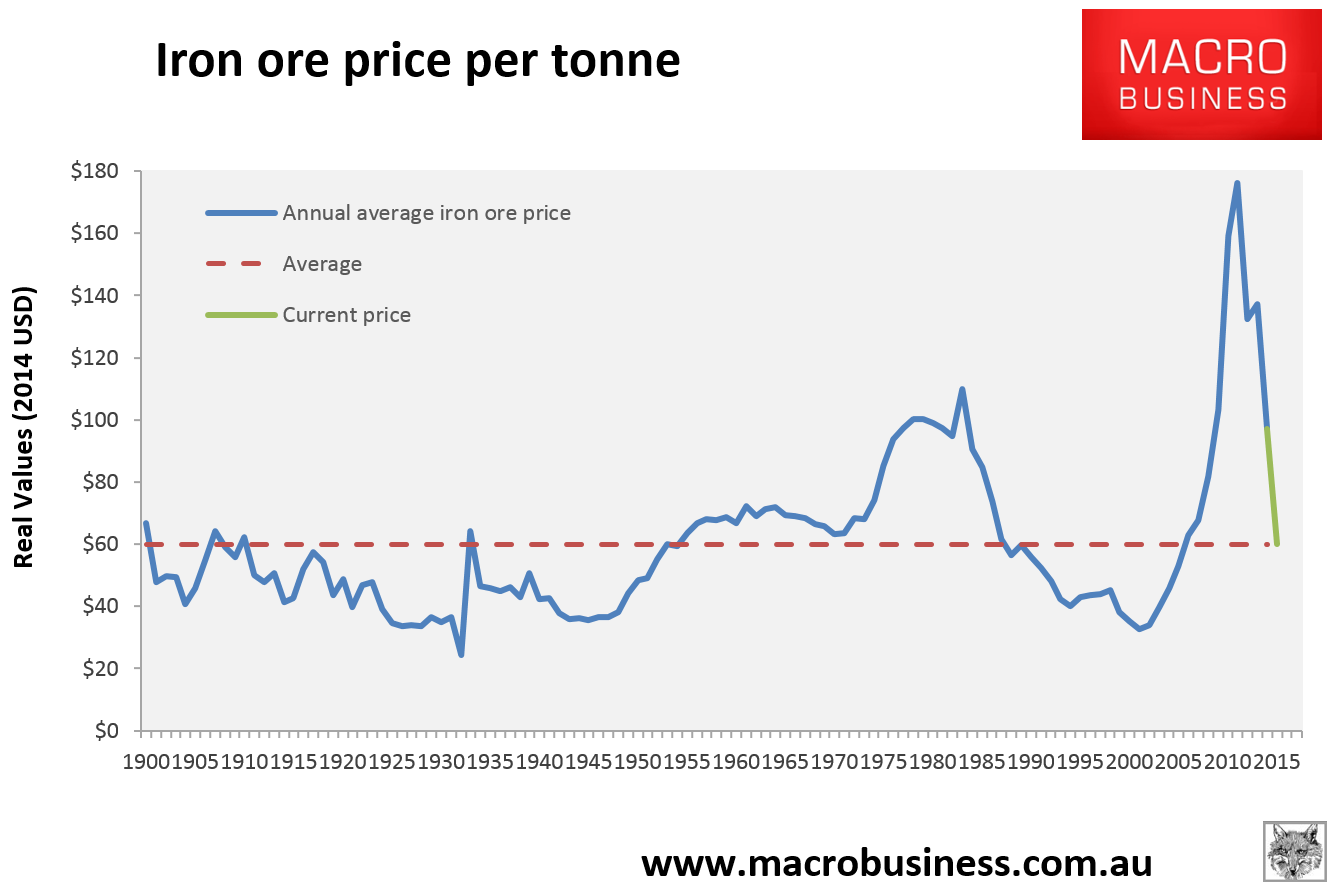

The way to read this table is to see long term averages as a representation of the structural value of certain commodities while the deviation from long term highs and lows is a gauge of where we are in the commodity price cycle. Using the 50 and 100 year averages, we see that many commodities are already cheap – coal, iron ore, nickel and zinc – but those same commodities are still way off their all time lows implying that if super cycle upside is going to be followed by a super cycle downside then we’ve much further to fall. We can nicely illustrate this with iron ore:

Note that the current price is at the average but when you account for boom and bust cycles, we are nowhere near what we can expect as a cyclical nadir given previous cycle lows. We’ve just had the greatest iron ore boom in history and are in the greatest bust.

Other commodities are still structurally and cyclically overvalued – oil, uranium, copper, lead, and the precious metals. By rights, all of these have much further to fall, period.

How far depends upon how much of a Malthusian enthusiast you are. The threat of ‘peak everything’ is more real today than in the past so some price premium is warranted. That is most pressing in oil and gas though commodities generally deserve a premium versus history on the sheer magnitude of human consumption now that China has joined the global bourgeoisie. The precious metals are not about supply so we can also discount them.

For me, then, the table suggests that the commodities most at risk of further cyclical declines are oil and gas (with prospects for a strong rebound) , uranium, iron ore, copper and lead. The commodities closest to the bottom are coal (with little prospect of a rebound), zinc and nickel.

Have commodities bottomed? Nope.