Old man Gotti today tries his hand at the QLD LNG debacle:

Australia needs extra gas, and the ruling families of Brunei and the United Arab Emirates have the world connections to bring expertise into Santos to replace the skills that have been lost amid Santos’ cost-cutting.

In theory, the simplest way around the problem would be for Santos to bring back John Ellice-Flint, the man who conceived and set up the Santos base Queensland strategy. When Ellice-Flint resigned in 2008, the Santos board upscaled the project with insufficient capital and technical skills in coal gas production.

Survival while awaiting better prices is now the name of the game. It’s not easy because as it now stands, Santos must continue to invest big sums annually to produce Queensland gas. What’s required is investment to streamline the Queensland gas production and an expansion of operations in the Cooper Basin.

John Ellice-Flint is backing the bid because he knows he will have the capital available to make the changes required and invest in the future. Santos has too much debt to achieve that goal and there is no way the local institutions would subscribe the billions required in capital to begin the streamlining and expansion processes. That requires an investment strategy that is totally foreign to Australian institutions.

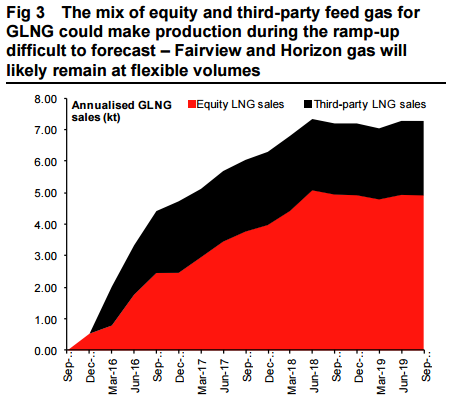

In short, let the big money have STO. The problem is, why would Sceptre Partners invest in more gas any more than STO alone would if it can also get it cheaper from the network? The following chart from Macquarie shows you how short GLNG is:

Either Asian gas prices are high enough to suck gas offshore and trigger more investment in gas here or they are not. It doesn’t matter who owns it.

Except if that ownership is large enough to offer local pricing power. The ACCC is already up in arms about Shell and Arrow’s gas stocks:

The Australian Competition and Consumer Commission has released a Statement of Issues on the proposed acquisition by Royal Dutch Shell (Shell) of BG Group (BG).

The Statement of Issues seeks industry views and more information on the competition issues that have arisen in the ACCC’s review to date.

“The ACCC is concerned that, by aligning Shell’s interest in Arrow Energy with BG’s LNG facilities in Queensland, the proposed acquisition may change Shell’s incentives such that it will prioritise supply to BG’s LNG facilities over competing gas users. As a result, Shell could choose to direct more (and possibly all) of Arrow’s large gas reserves towards meeting BG’s contracts to supply LNG export markets. This would remove some or all of Arrow’s gas from the domestic market,” ACCC Chairman Rod Sims said.

“Currently, Arrow has the largest quantity of uncommitted gas reserves in eastern Australia and there are a limited number of other potential suppliers to the domestic market. If the proposed acquisition resulted in less supply of gas to the domestic market, therefore, this could substantially lessen competition to supply domestic gas users and lead to higher domestic prices and more restrictive contractual terms.”

We could face the absurd situation in which one or several dominant producers force local gas prices higher than the export net back price just because they can (and will). Theoretically that could result in some other smart alec importing gas to Australia but we don’t have any regasification facilities so the market is not contestable in that way.

Basically, with the LNG bubble bursting and assets for sale all over the joint, Australia is now moving arse first through the resolution process for the eastern gas market. The ACCC is doing its best but is facing the fallout from the years of abdication of regulatory action by government around the LNG bubble. The ACCC’s own inquiry into said bubble is not due for release until mid next year, long after the decisions on these mergers will have been made.

There is one simple way to ensure both takeovers don’t frack up the eastern gas market any further: install domestic reservation. The ACCC can’t do that in a policy sense but it could try to apply conditions to the takeovers – the divestiture of Arrow for example – to protect domestic gas market competition.

Alas, that’s about as good as we can hope for in this backwards process (country).