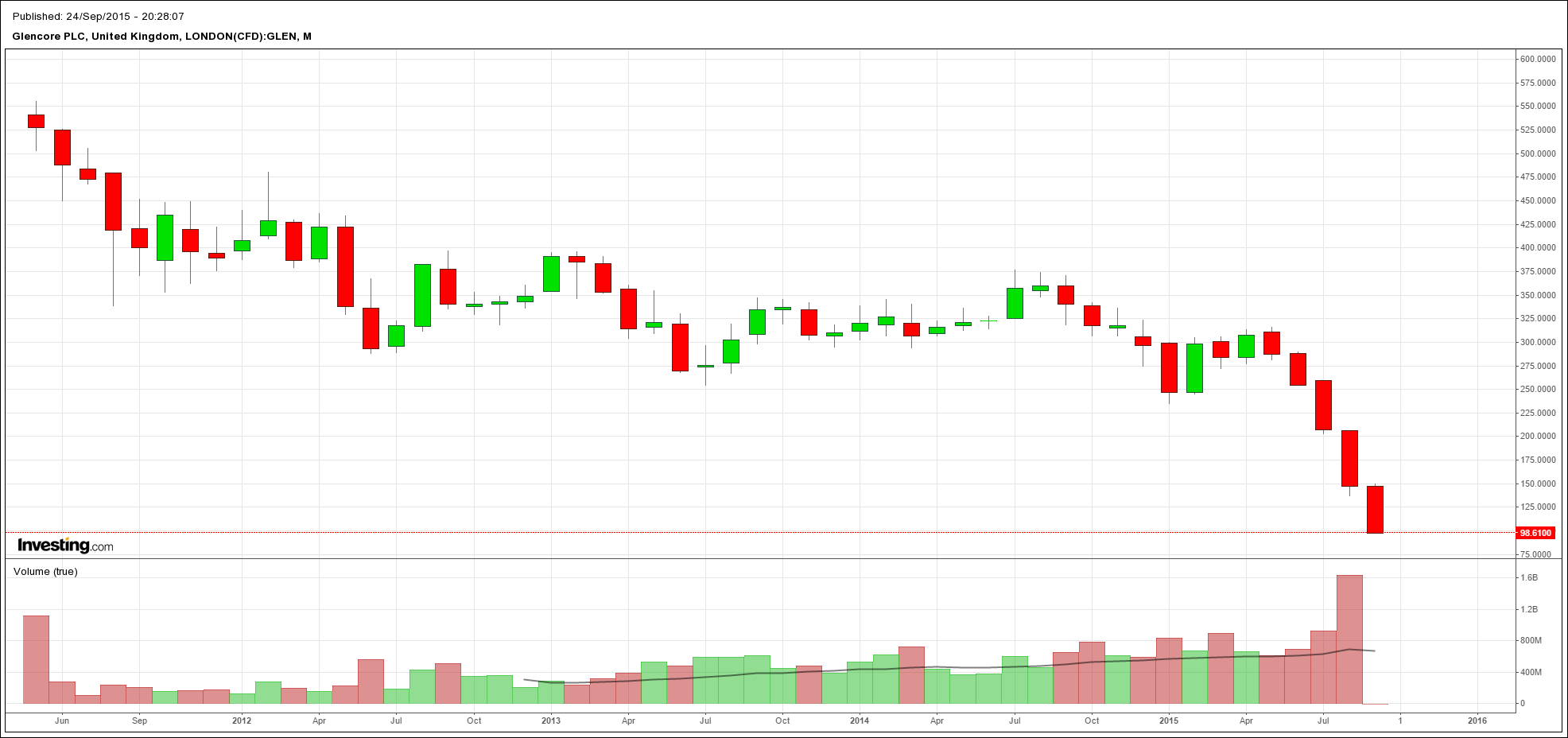

Trouble a-brewin for Ivan the Terrible with Glencore monstered another 10% last night in London:

The stock is now down 80% from its peak. The cause was Goldman:

What’s worse, if the company is downgraded from investment grade to junk, watch as the “commodity Lehman” scenario for Glencore, which much more than a simple copper miner just happens to be one of the world’s biggest commodity trading desks, comes full cricle leading to waterfall collateral liquidations and counterparty freeze-outs as suddenly the world is reminded that there is a vast difference between a real and a rehypothecated commodity, and that all collateral rehypothecation chains are only as strong as the weakest counterparty!

We update our estimates for Glencore following the completion of its equity placement on September 16, in which it raised its target of $2.5bn. We also update our estimates to incorporate our commodity analysts’ lower thermal coal forecasts ($58/54/52/t for 2015/16/17E) and lower met coal forecasts ($91/85/90/t), which impacts Glencore’s 2016/17/18E EBITDA by c.15-18%… On lower estimates we reduce our 12-month price target to 130p (was 170p).

The full text of this article is available to MacroBusiness subscribers

David Llewellyn-Smith is Chief Strategist at the MB Fund and MB Super. David is the founding publisher and editor of MacroBusiness and was the founding publisher and global economy editor of The Diplomat, the Asia Pacific's leading geo-politics and economics portal.

He is also a former gold trader and economic commentator at The Sydney Morning Herald, The Age, the ABC and Business Spectator. He is the co-author of The Great Crash of 2008 with Ross Garnaut and was the editor of the second Garnaut Climate Change Review.

What’s worse, if the company is downgraded from investment grade to junk, watch as the “commodity Lehman” scenario for Glencore, which much more than a simple copper miner just happens to be one of the world’s biggest commodity trading desks, comes full cricle leading to waterfall collateral liquidations and counterparty freeze-outs as suddenly the world is reminded that there is a vast difference between a real and a rehypothecated commodity, and that all collateral rehypothecation chains are only as strong as the weakest counterparty!