Exclusively from Gerard Minack.

Australia has a new prime minister to face the unwind of a once-in-a-century mining boom. Next year looks tough: the capex decline will accelerate, the car-makers will leave, and the housing boost may fade. A lower A$ is an offset. The key to avoiding recession will be avoiding job losses. It will be a close run thing, in my view.

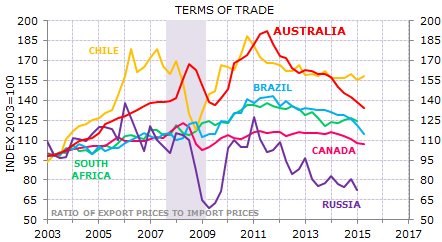

Australia is struggling with the unwind of a once-in-a-century mining boom. The boom was unprecedented for Australia, and was bigger in Australia than for other commodity-producing countries. The terms of trade went higher in Australia than elsewhere (Exhibit 1).

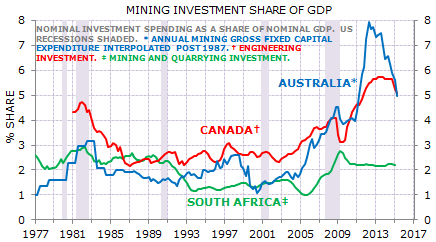

The investment boom was bigger in Australia than elsewhere (Exhibit 2).

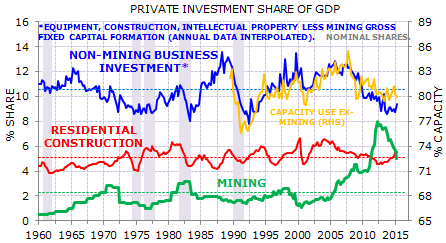

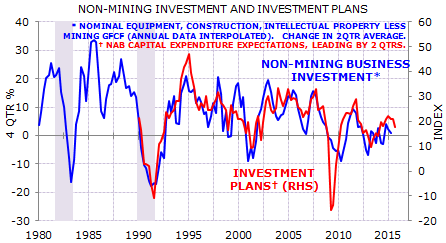

So far Australia has avoided recession, while most other major commodity producers have not. However, several problems lie ahead. First, the mining investment decline is likely to accelerate next year as major projects are completed. It’s not clear that investment spending elsewhere will provide even a partial offset. To be fair, ex-mining business investment is now near multi-decade lows as a share of GDP (Exhibit 3).

However, the usual drivers of investment remain soft: domestic demand is weak, profit growth is low, and there are few signs of capacity constraints. It’s not obvious that the main problem is ‘confidence’. For now, surveyed investment spending plans remain mediocre (Exhibit 4).

The second problem is the looming shut-down of domestic car production. Estimates for job losses are in the 20,000-40,000 range, concentrated in Victoria and South Australia. (The range depends on how many jobs will be lost in the domestic car-parts supply chain.)

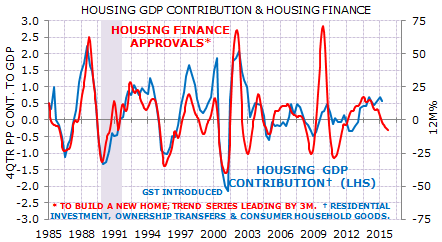

The third problem is that housing is unlikely to contribute as much to growth next year as it is now. Housing, including construction, real-estate activity and consumer spending on household goods, contributed 0.6 percent to growth over the year to June. Final domestic demand increased 1.2% over the same period. Leading indicators, such as housing finance approvals, suggest that the housing contribution will fade (Exhibit 5).

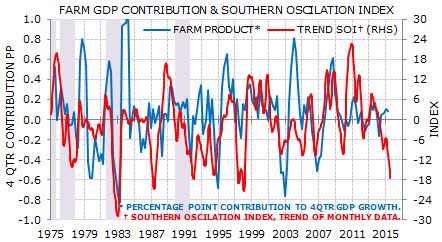

A possible fourth problem is drought. The Southern Oscillation index has averaged -15.5 in June-August. The June-November average in the nine strongest El Niño episodes since 1900 is -14.3. A serious drought can cut ½-1 percent from GDP (Exhibit 6).

This check-list of problems will hit an already-soft economy. Headline GDP growth overstates the strength because it is being supported by the rising mining export volumes. This is calorie-light growth: the volume growth is now being offset by price declines so mining export earnings have fallen over the past three years. This is why real national income is flat. Next year will see the start of LNG production, but price will be damped by the (typical) link to now-falling crude oil benchmarks.

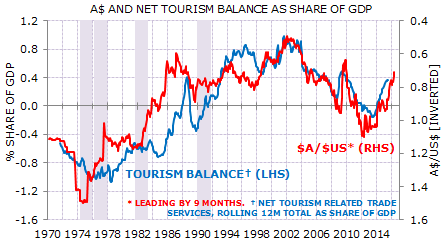

Lower interest rates have lifted housing, but as explained above that boost is likely to fade. The great hope is the weaker A$. There are signs of improvement in some areas, notably tourism. The net balance on tourism services has improved by around ½ percent of GDP (Exhibit 7).

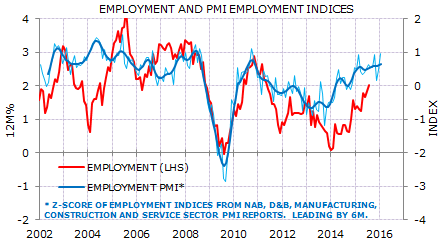

But looking into 2016 the issue is not whether there will be green shoots. The issue is whether the green shoots will have grown large enough to offset the branches that are about to drop. In GDP terms, that seems unlikely. However, in terms of judging recession risk GDP is not the key metric, in my view. The key is employment. As seen over the past 18 months, the slowdown in GDP has not been matched by weakness in employment. More to the point, leading indicators remain solid (Exhibit 8). I will adjust the risk of recession next year on the basis of how those leading indicators change.