Regular readers will know that the MB base case for global commodity markets is an historic bear market so large that it will not end until dirt is considered near worthless and it rocks the Australian economy to its knees.

The three legs of the thesis are the Chinese structural adjustment to slower and less commodity-centric growth, the enormous mal-investment that has created incredible oversupply in everything from coffee to steel based upon a ten year bubble in emerging market growth expectations, and the monetary tailwinds of a falling US dollar going into full reverse as the greenback rises first on rate hikes and then a global panic as the end of cycle event takes hold. This, in turn will deflate the bubble in ‘commodities under management’ that seized global managers over the past decade (that is, the huge unwind in hoarding).

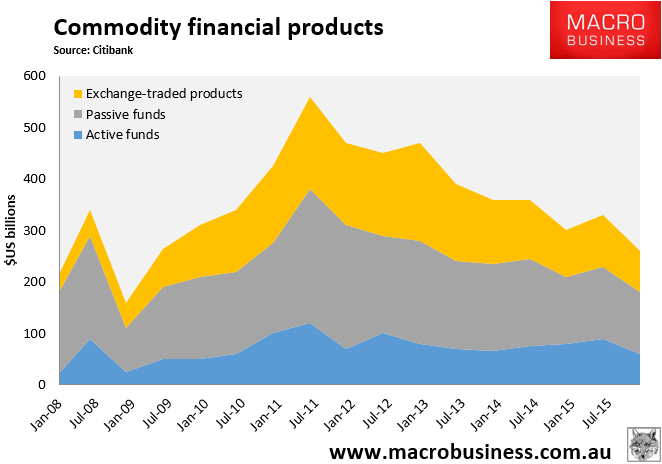

I keep everyone updated on the progression of this thesis across all of its dimensions but one that is less frequent is the degree to which the last point is unwinding. Today we get the update from Citi and we are well on track:

The full text of this article is available to MacroBusiness subscribers