RMIT University professor, Gavin Wood, spoke at a Housing Industry Association meeting yesterday, whereby he backed calls to replace stamp duties with a broad-based land tax. From The Daily Telegraph:

“Stamp duty discourages mobility and that’s a major problem for the economy”…

“It also prevents people from using certain housing stock. Empty nesters who would move to smaller homes are instead staying put to avoid the tax. The result is that these larger homes are not available to young families with children”…

Mr Wood said another danger is that the tax payment, which averages roughly $25,000 per property transaction in NSW, has eroded the typical deposit on a home and encouraged new homebuyers to take out larger mortgages…

“If prices fall, those who own only a small portion of their homes are most at risk of having to pay off mortgages worth more than the value of their properties”…

He recommended the tax be replaced by a uniform land tax that all homeowners would pay annually. The land tax would not apply to those who had already paid stamp duty.

Under this system, the tax burden would be shared by owners of both new and older housing…

Professor Wood raises a number of good points, but misses some others.

Advertisement

The number one reason why stamp duties should be replaced by land taxes is because they are highly distorting. As noted by Treasury’s recent discussion paper on tax:

Conveyancing stamp duties… have a high excess burden because they discourage the exchange of residential and business properties…

Stamp duties are some of the most inefficient taxes levied in Australia… they are levied selectively on activities or products and are taxed on the total transaction value, rather than the ‘value added’ component. Such transaction taxes are more likely to discourage turnover of taxed goods, as taxpayers attempt to reduce or avoid paying the tax…

Because revenue growth is driven by property prices and numbers of transactions, stamp duties on conveyances are a highly volatile tax, with revenue collected from stamp duties on conveyances fluctuating by over 50 per cent in previous years. Stamp duties on conveyances add to the costs of buying and selling property and can discourage businesses from undertaking productivity enhancing purchases of existing land and capital. The outcome can be retention of land for relatively unproductive purposes…

Stamp duties also impact on consumers by increasing the cost of buying and selling houses. As house prices increase over time, unadjusted progressive tax rates also increase the tax burden associated with stamp duty. For example, the burden of stamp duty on a median-priced house in Melbourne has almost doubled over the past 20 years — from 2.67 per cent of the sale price in 1988 to 5.16 per cent in 2011.

This clearly adds to transaction costs and contributes to Australia’s high (by international standards) costs of moving. These costs can discourage householders from moving to housing that best suits their needs and can be an important barrier to labour mobility. A number of reviews have found that, by dampening the number of house sales, stamp duties can also add to commuting times.183 Stamp duty can also be inequitable — those who move more frequently face higher costs than those who move less frequently, even if their circumstances are otherwise similar…

By comparison, land tax is the most efficient form of taxation going around, according to the Treasury:

Advertisement

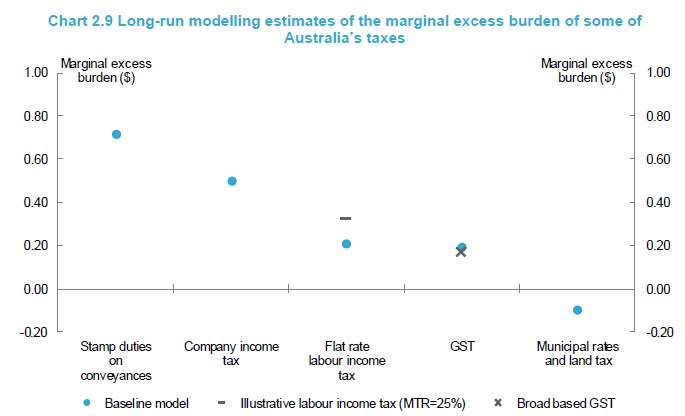

Modelling also suggests that broad-based land taxes, such as municipal rates, have a low economic cost (Chart 2.9). This is because land is immobile (unlike other capital) and cannot be moved or varied to avoid tax. The model applies this assumption to both domestic and foreign ownership of land. Land taxes paid by foreign and domestic landowners are only redistributed to the domestic households, providing a benefit to Australian households and generating a negative marginal excess burden for a broad-based land tax shown in the chart.

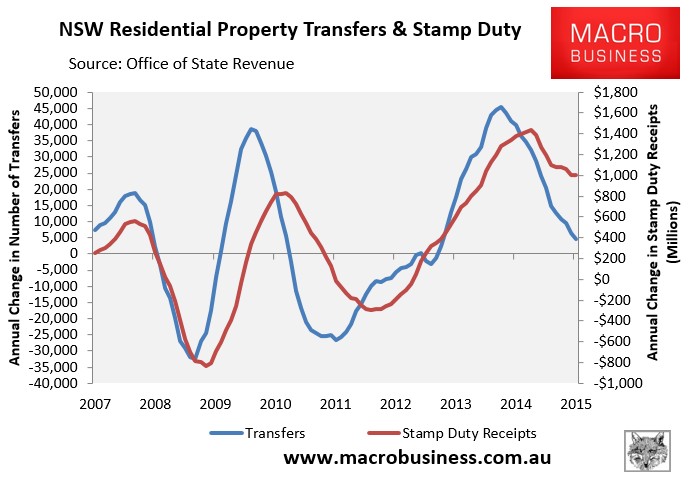

As noted by Treasury, stamp duties are also inherently volatile, which makes Budget planning incredibly difficult. One only needs to view the below chart on NSW stamp duty receipts to see what I mean:

Advertisement

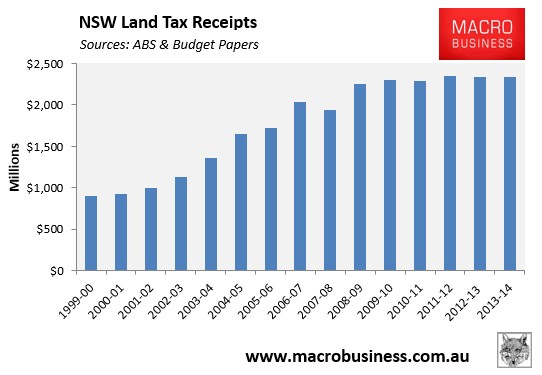

By contrast, land taxes – which are currently only levied on most investment properties – are highly stable:

Of course, there are other reasons to support a broad-based land tax, including:

Advertisement

They would help to make infrastructure investments self-funding for governments, since any land value uplift brought about through increased infrastructure investment (e.g. new roads, trains, etc) would be partly captured by the government via increased land tax receipts. Accordingly, governments would be more likely to facilitate development, rather than act to restrict it in a bid to save on infrastructure costs.

They would penalise land banking and vagrancy, effectively increasing the supply of land in the process and bringing new homes to market more quickly.

That said, I do not agree that land taxes should only be applied to those that have not already already paid stamp duty on their homes – effectively limiting the tax to new buyers. Why, for example, should someone that purchased their home decades ago (like my mum, who has lived in her house since 1972) be exempted from paying land taxes?

A better solution would be to give home buyers a credit for the stamp duty paid, and then deduct the theoretical land tax that would have applied since the home was purchased.

Advertisement

For example, if someone purchased a home in August 2010 and paid $30,000 in stamp duty, and their annual land tax bill would have been $3,000 per year had the new regime been in effect, then their credit would be $15,000, which can be applied against future year’s bills.

Leith van Onselen is Chief Economist at the MB Fund and MB Super. He is also a co-founder of MacroBusiness.

Leith has previously worked at the Australian Treasury, Victorian Treasury and Goldman Sachs.