On Wednesday, Glencore took the knife to capital expenditure again, cutting 2016 guidance to “no more than” $US5b, from $US6.6b. But chief executive Ivan Glasenberg said he expected 2016 to be “well below” the newly revised $US5b ceiling. Last week it cut 2015 guidance by up to 12 per cent to a “ceiling” of $US6b.

The RIO executive Andrew Harding recently described what was transpiring in the iron ore market as a balance sheet shakeout. That is, it was no longer just the cost curve that determined the winners and losers but the state of respective company balance sheets, that is, who had too much debt.

This is true to an extent but has been a movable feast not least because historically low interest rates have enabled those miners and commodity producers with stretched balance sheets to endure, marking time as they slashed costs and refinanced over and again.

We’ve seen this in capital hungry US shale, for instance, which has not shut down like many expected, but persisted and in so doing creating its own capital market calm, as well as now turning to unorthodox sources such as private equity.

We’ve seen it in coal and iron ore too, with any number of firms that were built for the good times able to manage through crisis as cheap debt was plentiful.

Advertisement

The end result of this has been that no commodity market has shaken out sufficiently quickly to establish new equilibriums in supply and demand, nor prices which have just kept on falling, in turn taking inflation and interest rates down in a deflationary feedback loop.

However, rather than see Mr Harding as wrong, I’m beginning to wonder if he was not more right than he knew. The global economy may wait for the deflationary feedback loop described above to play itself out in a benign manner. But it may not. Markets have a way of cruising along until the 11th hour and then suddenly panicking. And I wonder if we’re not approaching such a point around commodities and balance sheets.

Last night the monstrously indebted Glencore reported a respectable loss, from the AFR:

Advertisement

Underlying profit for the six months ended June 30 fell to $US882 million ($1.1 billion) from $US2 billion last year, 13 per cent ahead of consensus. But Glencore swung to a net loss of $US676 million, from a profit of $US1.7 billion, due to $US1.6 billion in writedowns.

The group was taking a “range of pre-emptive actions in respect of our balance sheet, operations and capital spending/recycling in order to preserve our current credit rating and sustain our track record on equity distributions”, Mr Glasenberg said. The group held its first half dividend flat at US6¢, in line with the year-earlier period.

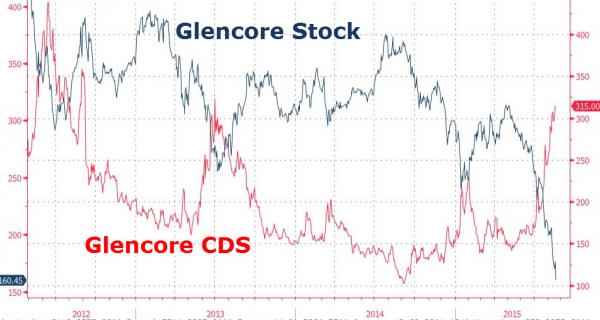

Well, good for it. But markets vomited and GLEN fell 10%.

Extrapolate this out a little and let’s ask what GLEN can really do? Its assets are plummeting in value, its debt ratios are ballooning and its cost of credit is rocketing. It’s caught in a balance sheet shock, I’m afraid, and while the AFR is still wondering if it will make a tilt at RIO, in truth it is headed swiftly into the trash can of market history:

Advertisement

And this is the point. It may be that given how easy debt is and has been that only a balance sheet crisis can effectively rebalance commodity markets. If that is the case then commodity market finance is going to have to seize up and the commodities balance sheet recession move up into both debt markets and banks. A kind of Minsky moment for dirt.

And, given many commodities are themselves key components in national budgets, and the firms that produce them are national champions, especially in emerging markets, we can push this analogy all the way to sovereigns. That is, commodity dependent nations are going to be forced into balance sheet adjustments as well.

Advertisement

This is the stuff of Australian nightmares.