MB Special Report: Asset allocation in the great Australian adjustment

Introduction

This is undoubtedly the most difficult time in a generation for an investor to make decisions about where to put his/her capital. Not only are we in the middle of a great shake up in major stock markets, and ongoing crises in European debt and Chinese equity and property, but the end of mining boom and an extremely unclear and fraught economic future beckons for Australia.

In this report I’ll first go through the macro prognosis, outlining the key threats and opportunities available to the Australian investor in the short and medium term. Next, by matching these likely scenarios to a probability quadrant of what is most likely to happen to both asset price and consumer price inflation we can start to weight our probability into an optimal allocation. The question then turns to the use of “traditional” asset allocation techniques, or my preferred and more robust “barbell” style. Finally we look at the brass tacks; timing and adjusting the strategic allocation to the current and possible short term tactical opportunities.

Prognosis

Against the backdrop of “The Great Moderation”, the most likely scenario facing the Australian economy does seem bleak. The optimists point to the previously strong asset prices that brought about falling unemployment, enormous household wealth and two decades free of recession as the keystones of sound economic management, but in fact this has resulted in an inherently weak economy that is in no state to take on another global shock or the normal end of a business cycle. The recession-less economy is not recession-proof.

To suggest that the next five to ten years will be similar to the post GFC re-inflation, or the so-called “Great Moderation” that lasted a generation is highly questionable, yet the consensus view on asset allocation reflects this combination of recency bias, speculation masquearading as conservative thinking and the long held hubris that “she’ll be right, mate”.

There are three main external risks to consider, tied to the three main economic powerhouses, Europe, China and the United States, each in their own way trying to exit post-GFC stimulus era. The currency union is holding on to the delusion that it can exist as a whole economy without fiscal integration or that austerity can be fruitful without external demand support. The Middle Kingdom is undergoing an enormous restructuring of its investment led economy into a more robust services version, ending its construction bubble but blowing another in stocks that combined is already skirting a hard landing. Finally, the world’s largest economy is still agonising seven years later on how to exit the world’s biggest monetary stimulus, with even the whiff of a single interest rate rise in an effort to restore the true cost of capital sending markets running scared.

Domestic risks are five-fold: a mining investment cliff that is already significantly detracting from headline economic growth and driving job losses, weak consumer confidence and spending due to the post-GFC income recession that looks set to accelerate, the bubble in Sydney and Melbourne house prices, a terms of trade and Budget shock due to the reliance on commodity prices and finally a currency that refuses to fall enough thus increasing the impact of all the above.

This constellation of risks is only offset by a small basket of opportunities in tradable sectors, including increased service exports and a potentially revived manufacturing export sector that is now so hollowed out it exists only in narrow niche products not in volume.

Probability

Given the above prognosis, what asset classes are most likely to perform well on a risk/reward basis, or more appropriately, what should be on the “avoid” list all together?

I prefer to take a top-down approach with two major intersecting factors in deciding where to allocate capital: first, at what rate is the global and local economy expected to grow or contract, and second; how will inflation or deflation occur due to consumer purchasing power or fiscal/monetary stimulus?

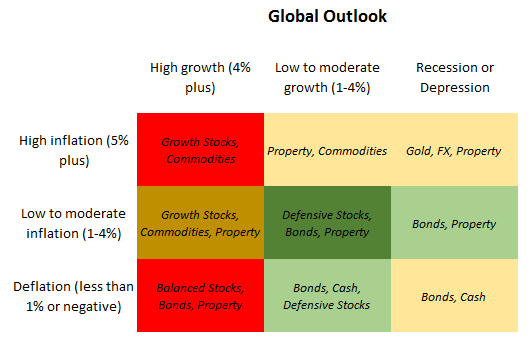

The variety of outcomes over a medium term can be plotted as a matrix of nine outcomes, each with a particular mix of assets that should do well. In this quadrant below, the higher probabilities are marked in green, lower in red with the best performing assets ranked within. This is the outlook for the global economy across an optimal global portfolio:

The most likely outcome is a low economic growth and low inflationary environment in the post-GFC world, with an almost equal probability of recession in the near future as the current economic cycle reaches its end. Whether this results in a moderate period of deflation or a 1970s style stagflation before the next upleg in the cycle is more dependent upon the reaction of monetary and fiscal authorities to the recession. Historically, this has been a time to be long defensive stocks, bonds and real estate for a combination of inflation-adjusted income and return of capital.

A repeat of the high growth, high inflation era that characterised the Asian Tigers prior to 1997, or a wartime economy is highly unlikely, given the lack of developing nations and other strategic factors. High economic growth with a deflationary bent is also highly unlikely, due mainly to historical factors and given the lack of consumer demand due to the enormous public and private debt load accumulated during the Great Moderation that requires ongoing servicing.

A return to the golden ‘Great Moderation’ of the last 30 years, or the post-WWII to Bretton Woods period is considered by the optimists to be the more likely scenario, where stocks (particularly financial and industrial) would begin a new secular bull market alongside everything else, including industrial commodities and property.

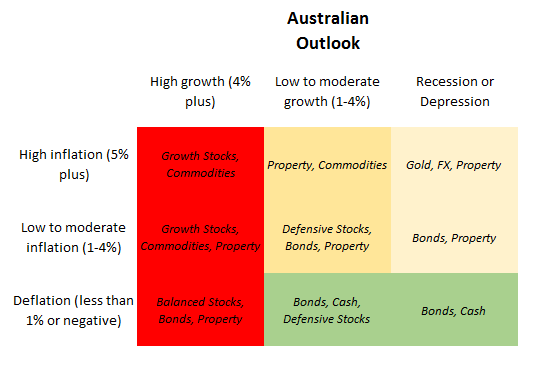

The picture changes when we look at the Australian outlook, where the upside risk of high growth is almost negligible, eliminating a vast swath of asset choices, and the downside risk shifts to that of falling inflation and economic growth:

The most likely scenarios here point to a mix of defensive stocks (with little or no capital growth expected), bonds (on the short end of the curve, and then ready to shift out if inflation starts to heat up) and cash/fixed interest. In should be noted that cash becomes more valuable as an asset in periods of low or negative inflation as purchasing power increases.

Different asset classes perform differently in magnitude and timing under the various conditions outlined above. Moreover, currency valuations can provide as much or more return on allocation alone, especially in inflationary periods during recessions, where a small amount of precious metals could also be beneficial. Property should not be discounted either, as it historically been a very solid store of capital during inflationary periods. Historically it’s only utility during a deflationary period is as a security asset, and/or at the end of the cycle pre-empting an uplift in inflation ahead.

Strategic Portfolio Allocation

Applying this probability to an optimal portfolio for the average Australian investor is called strategic asset allocation. By understanding the upside and downside risks ahead over the medium to long term, we now calculate the best mix of assets as part of an overall strategy.

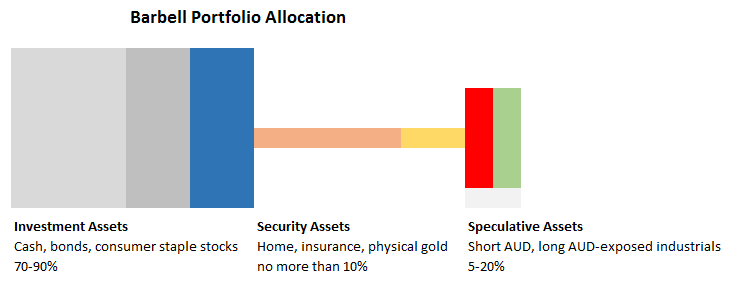

My preferred method of constructing a portfolio is using the “barbell”. A little explanation is necessary to convey the philosophy behind this more robust approach.

Traditional asset allocation only takes into consideration the excess of savings from an investor, and the allocation into “investments” usually split into growth and defensive assets. The so-called “balanced” portfolio might have as much as 70% in growth and 30% in defensive. This is a narrow view, built around the almost risk-free returns of growth assets during the Great Moderation and does not take into consideration that most investor’s wealth is tied into their own home (if they have one, or if its highly leveraged), with the remainder locked up in superannuation nor does it consider the value of insurance or other security assets as part of the mix or strategy.

The portfolio can be best visualised as an asymmetric barbell – a very heavy set of iron weights on one side, a solid bar in the middle and a very small set of “volatile metal” weights on the other. The proportion is really determined by the investor’s circumstance and cannot be optimised. The rule of thumb however is that no more than 10% should really be in the “volatiles” or what I call speculative assets. These include foreign exchange positions, most if not all listed securities and anything with a substantial amount of leverage employed. The solid bar includes security assets such as the home, life/TPD insurance, at call cash and possibly some other hedges including gold. The largest weights are the solid investment assets, those that deliver not only a return on the capital, but a return of the capital. These include cash and fixed interest, staple and utility stocks (and in the past, bank stocks) and unleveraged or positively geared property.

The barbell composition can change as circumstances dictate, noting that in a high growth environment, keeping most of your “irons” in cash would be detrimental, and that more focus on the volatiles is necessary, particularly if inflation is running high.

But the core reason behind this approach is the concept of absolute return – not losing money. Market volatility combined with a traditional approach to asset allocation can be wonderful, if you retire in 2007 or started investing in March 2009. But over the long run, you need to focus on eliminating capital losses first and foremost.

It is clear from the probability matrix above that cash will dominate due to its increasing purchasing power in a low inflation/low growth environment. For the Australian investor, a variety of differing sized and maturity term deposits (no more than $250K to have the deposit guaranteed and between 2 and 5 years) will do the job.

Normally, this would expand into other fixed interest assets including government and corporate bonds for their stable returns of income and capital. However, there is growing risk that a loss of the AAA rating by the Federal Government, combined with a raising of interest rates in the United States could turn into material losses for bond holders, especially at the long end of the curve.

Two and five year government bonds at the short end of the curve do not have much of an advantage over cash, currently yielding a little under or over 2%, about 70 to 100 bps below equivalent term deposit rates. Combined with the lack of depth and flexibility with corporate bonds, which is dominated by banks with their inherent risk, its hard to push these choices onto the “iron” side of the barbell.

International bonds may hold more promise given the yield differential, particularly with the US and the expected foreign exchange (FX) appreciation as the Australian dollar falls from here. This is probably more the purview of the sophisticated investor with a much larger portfolio size, although hedged and unhedged ETFs (exchange traded funds) can give smaller investors some choices here.

Furthermore, international shares may warrant an inclusion here on a small scale, if only for the FX advantage, combined with the current tactical setting of most international share markets in or near correction mode. I would prefer such an allocation on the “volatile” side and something to be revisited frequently due to the changing nature of share markets.

That leaves us with some exposure to staples and utilities, not for capital gain but for inflation adjusted income. The base case of the typical Australian consumer and household having less disposable income going forward eliminates the discretionary stock sector with a focus on big names in staples like Woolworths and Wesfarmers, owners of the grocery duopoly.

On the volatile side an exposure to short Australian dollar (against USD or Euro or Yen) is definitely warranted given the falls that are expected over the coming quarters and years. An equal or even larger allocation in Australian dollar exposed industrial stocks to take advantage of these falls and some real capital growth, alongside smaller plays in tourism and other non-discretionary service sector stocks would round out the 5-10% of total portfolio allocation. For those of the view that business cycle is close to ending with large stock price falls ahead, a pure US dollar position may be warranted.

The solid bar will depend on circumstance. Heading into a period of recession, falling house prices and rising unemployment would dictate that anyone currently paying off a mortgage should do so as quickly as possible, particularly if heavily leveraged (more than 80% LVR). Rolling consumer credit at higher interest rates into the home loan would also make sense, but not at fixed rates with the RBA look set to cut in the near future. Although this ammunition may not reach beleaguered lenders trying to rebuild their capital. The time to “lock in a low rate” is on the other side of the recovery.

A prudent amount of life insurance, particularly income protection is also necessary and often overlooked as part of an investors strategy.

Tactical Allocation

This is where we change our strategic allocation based on macro and market forces. While the prognosis is mostly baked in, the timing is not quite right on several fronts. Chief among these is the still elevated Australian dollar which impacts the majority of our planned allocation.

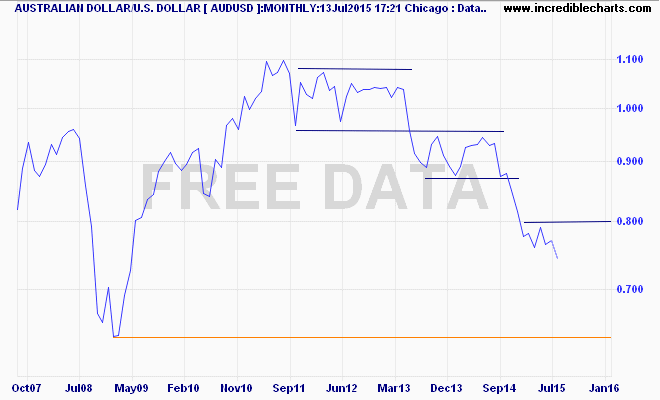

The decline from the $1.10 heights to ca. 74 cents has taken sometime, stopping at various levels of support before recently capitulating below 80 cents. While this looks like a big move, it is not enough to repair the real exchange rate, requiring a move down to the GFC lows around 60 cents (the orange horizontal line):

A short position remains warranted for now, with a view to adding on any rally up to 80 cents. The last stage of the falls are likely to be the fastest, so time may be of the essence here.

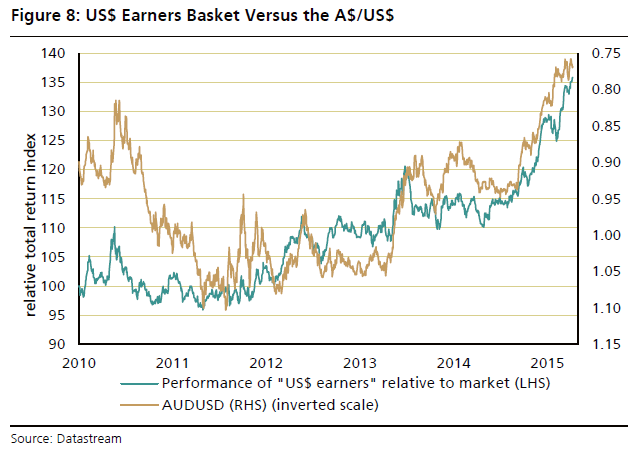

For AUD-exposed industrial stocks, holding on to a position in a broad basket remains sound as the dollar continues to fall, as this relatively long term play is paying off handsomely:

There are some timing opportunities currently with a select few, including Ansell (ANN), Cochlear (COH), CSL, Computershare (CPU), Resmed (RMD) and Sims Metal Management (SGM) all having undergone a small correction or dip in their rallies from which to add to or start new positions.

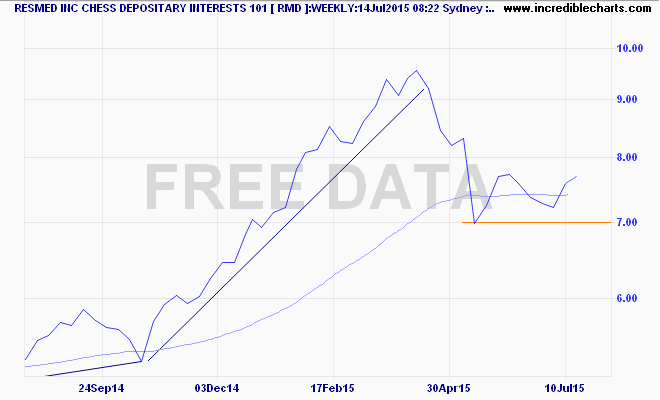

Here’s an example, with Resmed (RMD), a manufacturer and exporter of sleep apnea equipment, having followed and then exceeded the inverse return of the AUD vs USD, has now corrected but formed a firm base to start a new position:

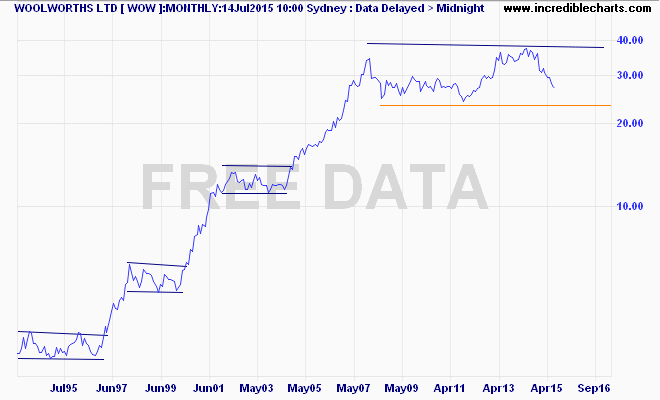

There has been a similar correction in the grocery duopoly with both Woolworths (WOW) and Wesfarmers (WES) (though the latter is higher risk given exposure of discretionary spending), both suffering at the hands of market volatility in recent months. Woolworths has fallen some 30% to a new three year low, but this is part of a long running pattern throughout its share price history, tracking the travails and fortunes of the Australian economy:

With a current grossed up dividend yield over 6%, the time is right for a sizeable allocation given the lower market pricing risk, knowing there is little or no expectation of any capital gain for the medium term.

Although the recent correction in European share markets and the current pause in the US may provide an opportunity to pick a new bottom, the time has probably passed to add to or start an allocation to international shares. The main concern is that valuations are extremely stretched going into the end of the business cycle and through the air pockets that will characterise the exiting of the stimulus packages and a return to normalised interest rates.

Furthermore, whilst the Australian dollar has fallen substantially, this has not yet correlated with falls in share prices, thus only profiting those who purchased international shares in recent years, who should really be looking to take profit.

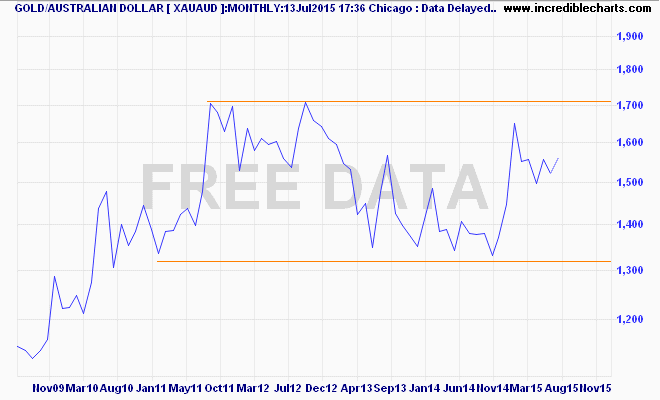

For those wishing to start or add to their physical gold positions, whilst gold priced in USD remains in a secular bear market as the USD strengthens, priced in AUD the situation is different.

Gold (AUD) has been in a wide trading range since hitting a post-GFC high at $1700AUD per ounce in early 2011, and recently a low of $1300AUD per ounce. We are now at a mid point of those extremes and even if the USD price of gold stutters or falls, provides a good hedge against a falling local currency. MB remains of the view that US dollar gold will fall materially further before rebounding so adding to positions can wait:

The return on the largest allocation, cash, is always dependent on the future direction of interest rates. For now, while the RBA has paused its cutting of interest rates at 2%, the inevitable conclusion of the mining investment boom coupled with crashing commodity prices and their impact on the Federal Budget will force their hand sooner rather than later. MB expects another cut by no later than October this year, which will immediately impact term deposit rates. The longer maturation the better for now as there is little or no expectation of any rate rises in the medium, or indeed long term.

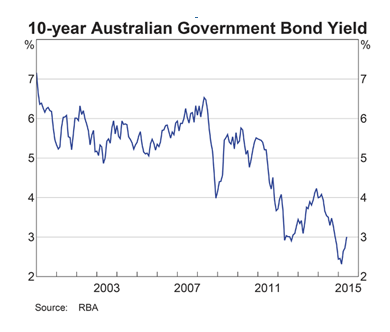

A similar dynamic is playing out in bond markets as the long end of the curve, the 10 year government bond only yielding a little over 3%, having reached a bottom at 2.5% recently:

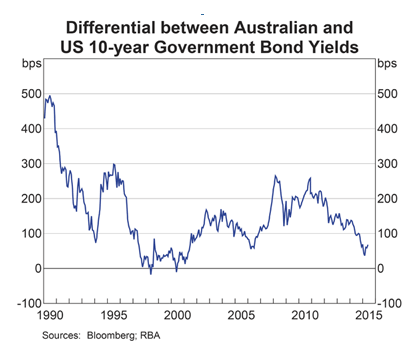

Given the high risk of the loss of the AAA rating in the near future, coupled with the potential of an interest rate rise in the United States, the interest rate differential with US Treasuries is slowly being filled, which will lead to capital losses for Australian bondholders (mostly foreigners) and possibly capital flight. The risks versus straight cash in the bank are too high for any allocation right now:

Conclusion

As the great Australian adjustment gets going, it is more important than ever to focus on the key element to successful investing – asset allocation. By determining the most likely trajectory given the macro factors at play, and adopting a conservative, yet robust stance amid volatile markets, combined with some tactical allocation techniques, the savvy investor can negotiate this period without high risk of capital loss, in comparison with the “buy and hope” traditional investor.

This report is the core of a series on how the Australian investor can both protect and profit from Australia’s deteriorating economic circumstances. Next up is in the series is How to Hedge a House.