An iron inquiry of lies, dills and ignorance

What a political economy we find ourselves in! It’s a wreck and a ruin. Populist to a fault. Totally without facts. Run by dills. Powered by lies. Churning out ignorance. Witness the iron ore inquiry.

The Australian says:

It’s true that the big operators will be able to increase pressure on smaller Australian producers such as Fortescue as they lift export volumes. It’s also true that they have high-cost Chinese underground miners in their sights and not just Fortescue. But what Rio and BHP are doing also happens to be a logical tactic to maximise returns in a low price market; a tactic that serves the interests of shareholders. Nor is the volume argument all one way. Rio’s iron ore chief executive Andrew Harding says his company, BHP and Brazil’s Vale together have added almost 400 million tonnes to the seaborne market since 2004 compared with just over 400m tonnes contributed by Fortescue and other new entrants. There is no evidence that Rio and BHP have been acting in concert, and even were they to agree to cut production it’s unlikely to have the simple effect hoped for by Mr Forrest, who said: “The iron ore price will go straight back up to $70, $80, $90 and the tax revenues which that will generate will build more schools, more hospitals, more roads, more of everything which Australia needs.” Resource companies by their nature operate in a global environment with dynamic supply and demand far more powerful than any brake we might put on our exports. And the attempt would risk damage to our reputation with China and other key markets while ceding advantage to offshore rivals such as Vale and new producers coming on stream. Former BHP chairman Don Argus puts it more bluntly in this newspaper today: intervention would make us a “laughing-stock of the world” and suggest we are a command economy.

It must be recalled that BHP, RIO and Vale have not expanded production on the basis of driving Chinese mines out of business. They expanded on the notion that Chinese steel production would grow another 160 million tonnes (mt) from where it it today to one billion tonnes. That is another 280mt in iron ore demand matching the roughly 300mt in planned expansions. The fall back argument was that a $120 “price floor” – where Chinese production was costed – would hold up the price as Chinese mines closed. All of the juniors used the same argument to expand, including Fortescue.

In short, the entire iron ore expansion program of the past five years was built on a very large mistake. Chinese steel output has now peaked and there is no $120 price floor.

The Australian’s second mistake is to argue that if Australia were to cut production, the price would not go back to $70. It would in the short term. But that would immediately invite higher cost Chinese, African, Indian and Brazilian iron ore back into the market and prices would fall again unless the Australian cartel cut production again.

Remember that the global infrastructure to supply has already been built based upon the over-estimation of Chinese demand and the $120 price floor blunder.

With Chinese demand falling into the future, Australia would very quickly find itself rapidly shrinking its output to support the price with the end result that the world’s most profitable iron ore lies fallow in the ground while all other countries make money.

And so to Don Argus:

Former BHP Billiton chairman Don Argus has warned Australia would become a “laughing stock of the world” if the government intervened in the iron ore market.

As the Abbott government considers an inquiry into claims by Fortescue Metals Group chairman Andrew Forrest that industry giants Rio Tinto and BHP Billiton have been forcing down prices and driving out smaller rivals, Mr Argus warned that intervention would make the nation non-competitive and send mixed signals about whether Australia was a command economy or a market economy.

“We will be a laughing stock of the world because, in a market economy, prices will determine what is produced, how it’s produced, and who will get the things we make,” Mr Argus, also a former National Australia Bank chief executive, told The Australian.

“A market economy uses prices as signals telling us how to use resources.”

Yes, it does, but Mr Argus will know that iron ore is not really a “free market” as such. It is an oligopoly market. There is an existing and implicit cartel structure in the big three producers and a massive duopoly in the Pilbara. These are natural monopolies owing to the nature of the iron ore business itself in which scale, capital intensity, geography and geology are the key determinants in profitability.

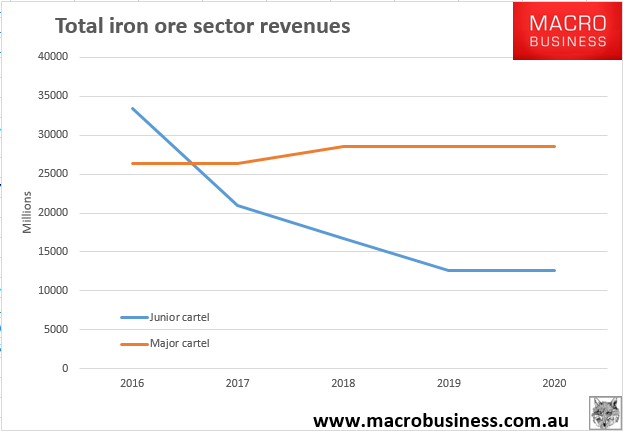

The choice before Australia is not a “market” versus “command” iron ore structure, it is what kind of cartel do we want. Do we want a natural cartel run by large and very profitable firms that can dominate market share and retain some long term pricing power, or do we want an artificial cartel that supports smaller miners in the short term but squanders market share in the medium and long term and leads the sector into a feedback loop of falling production and prices. Here is my modelling of the two outcomes.

In the junior cartel, Australian iron ore produces 837 million tonnes (mt) of iron ore from 2016 onwards. It does so at a slightly improved price for 2016 as oversupply is reduced in the short term by 43 mt as majors retrench. However, as Sino, Roy Hill, Anglo and Vale continue their expansions and Chinese demand keeps falling, the glut builds from 2017 onwards and the price keeps falling. In due course, smaller members of junior cartel require enormous subsidy to stay afloat as they register huge losses year after year in a price environment stuck at $20 and below. It’s either that or the cartel must negotiate spectacularly implausible shared volume cuts across all Australian producers (at least those in the cartel). Trade rules must be junked, Chinese relations destroyed and the WTO as well as ACCC told to piss off. To operate this would require a virtual nationalisation of all players as total transparency governs quotas, otherwise widespread cheating is inevitable, as in OPEC.

In the alternative model, the major cartel, Australian iron produces 880mt in 2016. It does so at an average $10 lower than the junior cartel in that year given the higher supply glut. However, as the 50mt of junior and 165mt of Fortescue production shuts down by 2017 the iron ore price at first stabilises and then slowly rebounds as some pricing power returns to the major producer’s cartel. Iron ore volumes are down to 715mt but the price is trading at $40 per tonne in a rough market balance.

Juxtaposing these two scenarios gives you the following total revenue chart for the sector (and nation):

That brings us to a real clangor today from Richard Denniss at The Australia Institute:

A little bit of economic theory is a dangerous thing, and many of the people defending what BHP and Rio Tinto have done to the price of iron ore are demonstrating that they have very little economic knowledge indeed.

…Australian citizens have inherited a significant, but not enormous, bundle of natural resources. We can sell them off as quickly as we want, but we never get them to sell again. Simple economic analogies about free trade are being used to justify the decision making of BHP and Rio Tinto, but if flooding the market and sinking the price was the best way to get rich then why do Apple make so much money selling such expensive phones, and why have OPEC made so much money selling such expensive oil? A parliamentary inquiry into how Australia’s scarce resources are managed is well overdue.

In Apple’s case it is because it adds value to its product and it is not available everywhere by kicking your boot. In OPEC’s case it is because it has occupied the position of swing producer across enough countries and jurisdictions for it to stick. In short, if Australia were producing a high value-add product or it managed to persuade Brazil to join a cartel with quotas that are adhered to, then an iron ore OPEC would work for a while. However, note that OPEC has product that is increasingly in short supply. Even so, it has now created US shale by keeping prices high and as described above, with iron ore infrastructure across the globe already in place, a similar iron ore cartel would create new supply everywhere much more quickly than oil did, and find itself having to cut back in short order as Chinese demand falls.

In short, not all markets are the same and a little economics is indeed a dangerous thing.

Which brings us finally to RIO where there’s good economics but not enough truth, from Matthew Stevens talking to RIO’s iron ore boss Andrew Harding:

“There is an allegation that we are we are flooding the marketplace with our volume increases. But between now and 2017 that increase is going to 20mtpa. The seaborne market is at about 1.3bn tonnes, but let’s say it is 1bn for easy maths. That increase is two per cent of the market. That is not a flood, not anywhere, not in any market.”

…Rio expected to add about 20mt to volumes by the end of 2016. BHP will likely match that, though it has slowed its march on the long-term target of 290mtpa. But over that same period, Brazil plans to add maybe 118mtpa of capacity to a seaborne system. Vale will add about 90mt of that new supply and it will come on at a cost of maybe $US15 a tonne. Anglo will add the rest. Costs will be slightly higher but, at 67 per cent FE, the grade is definitively premium.

RIO is about to add 40mt not 20mt of capacity. BHP has about another 40mt to add as well. The Vale figures are right. As well there is Anglo adding roughly 20mt, Sino adding 20mt and Roy Hill adding 55mt. That’s before we talk about Africa’s Tonkolili at 25mt and India’s Goan ore which will return this year with 10mt but could go much higher with prices above $50.

In short, the Pilbara majors are adding a lot and should capture more market share, which is good even if some of it comes from other Australians.

With that little lot under our belts, the real question today is how did a nation that is so utterly dependent upon one commodity become so completely ignorant about how it works?