by Chris Becker

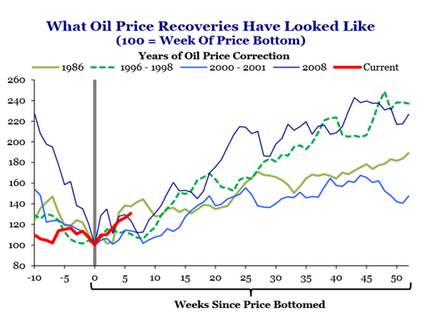

From Stocktwits comes a nice chart showing how previous crashes in oil recovered:

This should inject some caution about declaring that this time is different. But that’s what I’m going to do!

While I’ve spoke recently about the technical outlook for oil, today we can add some fundamental reasons why the greasy stuff is not coming back. Yesterday’s China data dump with its hard landing connotations for demand is taken up at Bloomberg:

The last time oil crashed, during the 2008 financial crisis, China’s appetite for commodities seemed insatiable, and powered prices higher. This time, Chinese fuel use is growing at half the rate of the past decade, and sliding U.S. shale output could reverse as prices rise, smothering the gains.

Global oil demand will grow just 1.3 million barrels a day to 94.58 million next year, the Energy Information Administration said Tuesday.

In the U.S., consumption will increase 0.4 percent next year to 19.44 million barrels a day, leaving it at a lower level than in 2008.

China’s fuel demand will grow by 3.1 percent next year to 11.34 million barrels a day, according to the EIA. That compares with an 11 percent jump in 2010 that helped boost crude prices by 15 percent. Annual growth has averaged 5.2 percent in the past 10 years.

Global oil production is set to rise about 95 million barrels a day this year, at least 1 million barrels per day above demand. And the EIA is predicting these levels of overproduction through to the end of 2016.

The recent oil price crash has still not cleared out the high cost extractors in the US either according to Goldman Sachs, from ForexLive:

- The drop in US rig counts is not yet large enough to reduce production

- Especially given that efficiency gains have surprised to the upside

- Well backlogs are building that could quickly add over 250kb/d of production when deployed

- Also not that declines in oil production from the US and non-OPEC sources have been offset by higher production in Saudi Arabia, Iraq and Russia

- GS say they do not expect OECD inventories to decline until 2016

The technical point of view does suggest some rhyming with past events, which is why I suggested awhile back when oil was languishing at $40 something a barrel that a 50% rally was not to be unexpected, but it looks much harder to move higher from here.