by Chris Becker

When I first started at MB many moons ago I penned an article about a trading indicator called the “KC Signal”. This was no new invention, but an observation of price action of a security that went “too fast” in its uptrend, overshooting and coming back down to earth.

For all intents and purposes, oil has rallied too far and too fast. As a long term observer and trader of the oil markets I understand that volatility can send prices rallying higher and sinking lower than expected. In particular, investors used to blue chip stocks find it hard to fathom a 50% price decline and subsequent 100% rise in commodity markets, but this is not unusual.

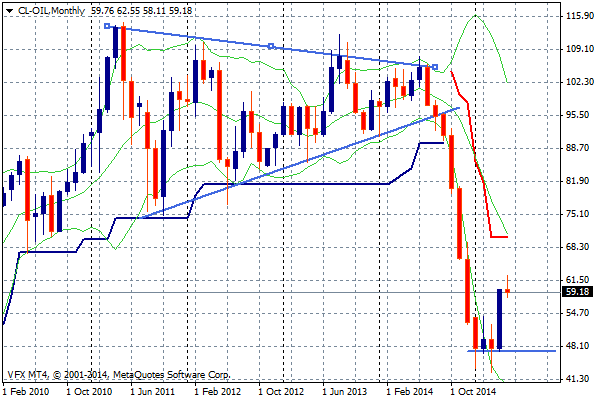

First, a recap of what has happened to oil recently, using the NYMEX WTI marker:

Following a huge glut in production from the US shale gas fields, the multi-month symmetrical triangle in oil, which had been affected by successive runs of QE from the US, finally broke down, falling 50% from $90 to $45 four short months.

The recent rally from its extreme low to high has actually been 50% in magnitude, which I suggested a few months back as not to be unexpected (I get it right from time to time).

Many market commentators call a 20% rise a bull market, but oil remains solidly in a bear market until it can regain its former high, regardless of this short term price rise. Indeed, with all the technical hallmarks of a bear market rally, questioning the physical/futures price disconnect can also be asked.

From Reuters recently:

While oil futures prices rebound with vigor as analysts cite strong demand, the physical crude market tells a much more cautionary tale.

Tens of millions of barrels are struggling to find buyers in Europe with traders of West African, Azeri and North Sea crude blaming poor demand.

The deep disconnect between the oil futures and physical markets looks similar to the events of June 2014 when the physical market weakness became a precursor for a futures price crash.

However, data from OPEC and the International Energy Agency show the world is still pumping 1.5 million barrels per day more crude than it consumes.

However, an increasing number of market watchers agree that the fundamentals point to what should be a more bearish market, at least until either supply is cut or demand increases.

“The top of the current bull mountain might not be close but unless there is a fundamental change in the physical supply/demand balance, the rock might start rolling back down shortly again just like it did in the second half of 2008 and 2014 only for the bulls to start the arduous uphill battle all over again”.

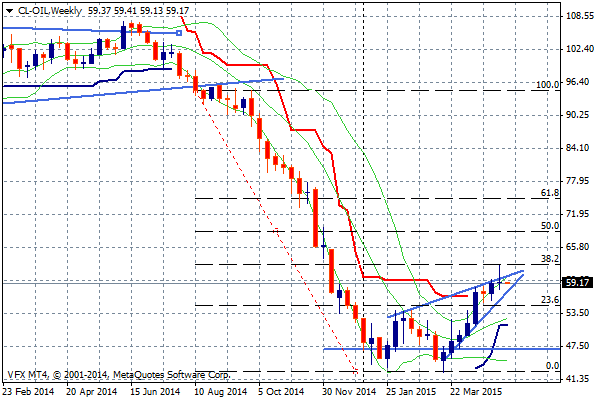

The chaps at ForexLive late last week pointed to a daily technical pattern that was underway, in addition to deteriorating fundamentals:

Iran is a few months from flooding the global market with oil stockpiles and softer global growth has kept demand in check. The (recent) trade, however, is technical. Crude prices have been rebounding for the past six weeks and there was no reason to step in front of the momentum.

A three-candle reversal appears to be underway. If you draw the downtrend from the start of October (I would prefer it from the June highs), then we’re also closing in on the 38.2% retracement. Finally, the modest uptrend since March broke recently

Here’s the Fibonacci sequence from the breakdown of the trend. I’ve displayed a possible bearish rising wedge pattern forming, which correlates with the 38.2% retracement and the three-day reversal pattern stands out as a single “tombstone” weekly candle here as well:

My downside target on a break of the current uptrend is first support, former resistance at $54USD per barrel, and then the long held point of control at approx. $47USD per barrel with the floor only slightly below.

The two big unknowns remain on each side of the supply/demand equation. First, how the shale producers in the US, under huge pricing pressure can come back off the floor from the OPEC headlock amid growing volatility in the Middle East. On the latter, will Chinese strategic demand and furthermore, global demand in the face of lower energy prices, rebound.