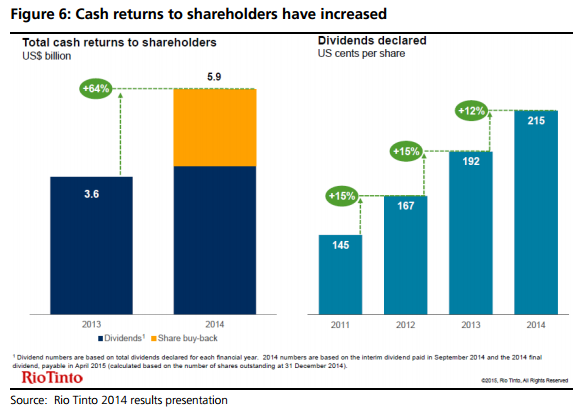

Earnings 4% ahead of consensus at US$9,305m. US$2bn buyback announced

Rio Tinto reported 2014 underlying earnings of US$9,305m, down 9% y/y and in line with our estimate of US$9,274m, and 4% ahead of consensus of US$8,916m and towards the top end of the consensus range of US$7,846-9,389m. The 2014 dividend was US215cps, up 12% y/y, below our estimate of US220cps, and ahead of consensus of US212cps. As promised, Rio announced additional returns to shareholders in the form of a US$2bn buy-back, with A$500m to be conducted by way of an off-market buyback in Ltd shares by April 2015, with US$1.6bn to be purchased on market in plc over the course of 2015. This was broadly in line with market expectations, albeit the form is perhaps different, as we had thought Rio might prefer a special dividend to an off-market buyback as it could further reduce the liquidity of the Ltd line.

Net debt down 31% y/y to US$12.5bn, as cash is released from balance sheet

Rio reported an impressive US$5.5bn or 31% reduction in net debt over the year to US$12.5bn, with the bulk of the reduction (US$3.6bn) coming in H2 14. This compared with our estimate of US$15.4bn and consensus of US$16.2bn. This saw gearing down at 19% at year end, below the target range of 20-30% – hence, we believe, Rio felt confident in its ability to promise a material lift in returns.

Battening down the hatches: ready to weather the storm

CEO Sam Walsh said that the start of the year suggests 2015 will be challenging, with a continuation of the current industry-wide margin compression. Based on our commodity forecasts, we expect Rio’s 2015 earnings to be down 23% to US$7.1bn, driven principally by lower iron ore prices. But with EBITDA of US$16.2bn forecast for 2015, and with 2015 capex cut further to <US$7bn (prev. US$8bn), we feel confident that Rio Tinto is well placed to weather the storm. We do not expect some other companies to be as well positioned – which we expect reporting season to show. Valuation: A$75.12 (DCF, 10% d.r) We are yet to adjust earnings to reflect the 2014 result. Our price target of $67ps (unchanged) is set at 0.9x NPV for market risk.

That is exactly the right read, I think, and represents very bad news for every other iron ore producer on earth, as well as Australia, which will travel through the shakeout with the firm. RIO is not changing course and the iron ore supply tsunami will continue:

Infrastructure for the 360Mtpa expansion is around 80% complete, with all major rail, marine and wharf works in place. Completion of this infrastructure remains on track for delivery by the end of the first half of 2015. As previously announced, approximately 40Mtpa of brownfield expansions are under way to feed the expanded infrastructure capacity at an average mine production capital intensity of around US$9/t. As a result, production from the Pilbara is unchanged and is expected to be 330Mt (100% basis) in 2015.

I only differ in one respect to UBS. They have forecasts for iron ore of $65 this year and $66 next. Mine are $10 lower this year and $20 next year.

Advertisement

With its deleveraging and cost-out drive, RIO is indeed battening down the hatches but its earnings will fall $3 billion and $6 billion short of UBS estimates.

David Llewellyn-Smith is Chief Strategist at the MB Fund and MB Super. David is the founding publisher and editor of MacroBusiness and was the founding publisher and global economy editor of The Diplomat, the Asia Pacific’s leading geo-politics and economics portal.

He is also a former gold trader and economic commentator at The Sydney Morning Herald, The Age, the ABC and Business Spectator. He is the co-author of The Great Crash of 2008 with Ross Garnaut and was the editor of the second Garnaut Climate Change Review.