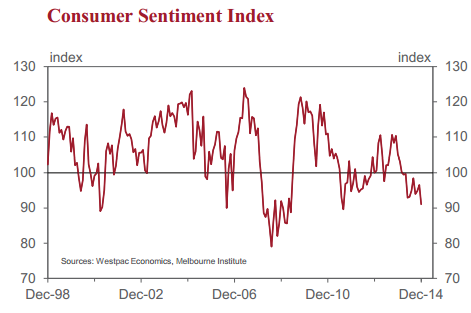

• The Westpac-Melbourne Institute Consumer Sentiment Index fell 5.7% in December from 96.6 in November to 91.1 in December.

This is a very disturbing result. The Index is now at its lowest level since August 2011 when it briefly fell below 90. Prior to that you have to go all the way back May 2009 to see a period when the Index printed consistently below today’s level.

There was consistent weakness in the index during most of the seven day survey period (December 1–7) but the read was significantly weaker on the day of the release of the September quarter national accounts. These showed that the economy had been limping along at a 1.6% annualised growth pace for the last six months, with national incomes declining and overall activity contracting in the quarter in every state except New South Wales.

Respondents may have been particularly unnerved by media references to an ‘income recession’.

Respondents are clearly concerned about the outlook for the economy and job security. In addition there is ongoing disillusionment about the May Budget, six months after it was announced.

The survey provides us with a specific measure of those news categories which most affected respondents and whether they were assessed as favourable or unfavourable. The most recalled news topics were: ‘economic conditions’ (59.2% of respondents); ‘budget and taxation’ (52.7%); ‘international conditions’ (26.3%) and ‘employment’ (19.5%).

Respondents assessed the news to be extremely unfavourable for all of these categories. Of those giving an opinion, 87% viewed news on ‘economic conditions’ as unfavourable; 83% viewed news on ‘budget and taxation’ as unfavourable and 96% viewed ‘employment’ news as unfavourable. These are the most negative responses on news recall since March 2001 on ‘economic conditions’, September 1986 on ‘budget and taxation’, and December 1975 (the beginning of the survey) for ‘employment’. These readings are almost certainly an overreaction but do highlight significant risks to spending, particularly over the course of the next few months.

The individual components of the index are also pointing towards a softening in spending.

With one exception all the components of the index were down: the sub-index tracking views on ‘family finances vs a year ago’ rose 1.6% but ‘family finances, next 12 months’ was down 4%, ‘economic conditions, next 12 months” fell 9.7% and ‘economic conditions, next five years’ was down 1.8%.

Of particular concern was a major collapse in the sub-index tracking assessments of ‘time to buy a major household item’.

This component fell 11.8% from 124.2 to 109.6. It is now 21.4% below its level of a year ago and has reached its lowest level since April 2009.

This is a particularly awkward time for respondents to feel so downbeat about purchasing major items given that it comes in the critical lead up weeks to Christmas.

That said, the decline may well be a reaction to recent sharp falls in the Australian dollar and the impact this is expected to have on the cost of imported goods.

Not surprisingly, respondents have increased their anxiety around the labour market. The Westpac-Melbourne Institute Unemployment Expectations Index increased by 4.4% to 159.5 (recall that a higher level indicates more consumers expect unemployment to rise over the next 12 months). Apart from one higher print in March this year, this is the highest read since June 2009 when respondents were still traumatised by the Global Financial Crisis.

Optimism around the housing market has evaporated. The index tracking assessments of ‘time to buy a dwelling’ fell 10.8% and is now down 19.3% over the year to the weakest level since November 2010.

Consistent with that shift in sentiment, the outlook for house prices has also deteriorated sharply. The Westpac-Melbourne Institute House Price Expectations Index fell 8.3% to be down 22.5% over the year. Despite this clear shift, expectations are still positive overall, implying more consumers expect house prices to rise than fall, and the Index is above its low in June this year and well above readings in 2011-12.

Respondents have become more risk averse in their preferences for their savings. The proportion of respondents nominating ‘bank deposits’ as the wisest place for savings increased from 34.3% in September to 37.0% in December. That is the third highest proportion of respondents favouring bank deposits since 1979.

Those preferring to pay down debt jumped from 13.7% to 17.6% while the proportion favouring real estate fell from 25.7% to 20.0%.

The Reserve Bank Board next meets on February 3. Last week, following the release of the national accounts, Westpac revised its interest rate forecast. We now expect the Board to approve a 0.25% cut in the cash rate at its February meeting with a further 0.25% cut in March. The messages from this survey are certainly consistent with the assessment that the Australian economy needs even lower rates. Overall confidence is weak. Respondents have sharply lowered their assessments of the economic outlook and their spending intentions. They remain extremely nervous about job security while adopting a more cautious attitude towards both their finances and the outlook for housing.

While this survey may prove to be an overreaction to the sobering news from the national accounts and ongoing concern around the Commonwealth Budget, it appears that the messages aroundspending, the labour market and housing are clearly signalling the need for a further boost in the form of lower interest rates.

In a world where other developed economies have near zero interest rates and, accordingly, the Australian dollar is overvalued, Australia should seize the opportunity to provide further interest rate relief to the economy and exert some more downward pressure on the Australian dollar.

David Llewellyn-Smith is Chief Strategist at the MB Fund and MB Super. David is the founding publisher and editor of MacroBusiness and was the founding publisher and global economy editor of The Diplomat, the Asia Pacific’s leading geo-politics and economics portal.

He is also a former gold trader and economic commentator at The Sydney Morning Herald, The Age, the ABC and Business Spectator. He is the co-author of The Great Crash of 2008 with Ross Garnaut and was the editor of the second Garnaut Climate Change Review.