Reserve Bank of India Governor Raghuram Rajan warned Wednesday that the global economy bears an increasing resemblance to its condition in the 1930s, with advanced economies trying to pull out of the Great Recession at each other’s expense.

The difference: competitive monetary policy easing has now taken the place of competitive currency devaluations as the favored tool for playing a zero-sum game that is bound to end in disaster. Now, as then, “demand shifting” has taken the place of “demand creation,” the Indian policymaker said.

As was the case in the 1930s, the lack of coordination between policymakers is producing spillovers that may be difficult to control, and the world’s financial system may soon face fresh turbulence at a time when central banks have yet to repair the damage that the 2008 financial crisis caused to developed economies.

“We are taking a greater chance of having another crash at a time when the world is less capable of bearing the cost,” said Mr. Rajan in an interview with the Central Banking Journal.

Before you write this off as the ramblings of a subaltern crackpot, recall that it was Raghuram Rajan that warned in August 2005 that:

Developments in the financial sector have led to an expansion in its ability to spread risks. The increase in the risk bearing capacity of economies, as well as in actual risk taking, has led to a range of financial transactions that hitherto were not possible, and has created much greater access to finance for firms and households. On net, this has made the world much better off. Concurrently, however, we have also seen the emergence of a whole range of intermediaries, whose size and appetite for risk may expand over the cycle. Not only can these intermediaries accentuate real fluctuations, they can also leave themselves exposed to certain small probability risks that their own collective behavior makes more likely. As a result, under some conditions, economies may be more exposed to financial-sector-induced turmoil than in the past. The paper discusses the implications for monetary policy and prudential supervision. In particular, it suggests market-friendly policies that would reduce the incentive of intermediary managers to take excessive risk.

Advertisement

He issued this warning at the FOMC’s Jackson Hole gathering where he was greeted with genteel jeering and was publicly dressed down by Larry Summers.

Rajan was proven very precisely to be right. Unfortunately he is almost certainly right again this time. The only question is when.

On that I’m on the record arguing that the Chinese property market may trigger the event some time after 2015. But another scenario that is a persuasive alternative is the Jeremy Grantham theory of a 2016 bubble bust for US markets following its Presidential election. On that Goldman today provides a nice trigger:

Advertisement

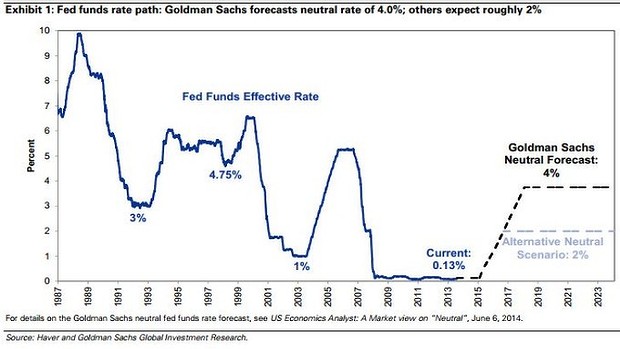

“The S&P 500 will generate an annualised total return of 6 per cent between now and 2018 when Fed funds reach a “neutral” level of 4 per cent…We assume a neutral Fed funds rate will be reached in 2018, and 10-year Treasuries will yield 4.5 per cent. Our baseline scenario implies an annualised total return of 1 per cent on a constant maturity 10-year Treasury note through year-end 2018…Buying a 10-year Treasury note and holding it through 2018 would also generate a nominal annualised return of 1 per cent.”

If we ever reach 4% I will very happily eat my hat.

David Llewellyn-Smith is Chief Strategist at the MB Fund and MB Super. David is the founding publisher and editor of MacroBusiness and was the founding publisher and global economy editor of The Diplomat, the Asia Pacific’s leading geo-politics and economics portal.

He is also a former gold trader and economic commentator at The Sydney Morning Herald, The Age, the ABC and Business Spectator. He is the co-author of The Great Crash of 2008 with Ross Garnaut and was the editor of the second Garnaut Climate Change Review.