One of the first charts APRA published this week was the amount of “common equity tier one capital” held by deposit-takers as a share of “risk-weighted” assets. This is similar to the first-loss equity home owners have invested in their property.

According to APRA, the major banks had 8.6 per cent common equity tier one capital at June 30, 2014…On this basis, the major banks look to be leveraged 11.6 times, which is not absurdly high…But bankers and regulators heroically assume that a certain portion of residential home loan assets are completely risk-free through the application of a concept called the “risk-weighting”…Today the average risk-weight applied by the majors to standard home loans is a stunningly low 15 per cent.

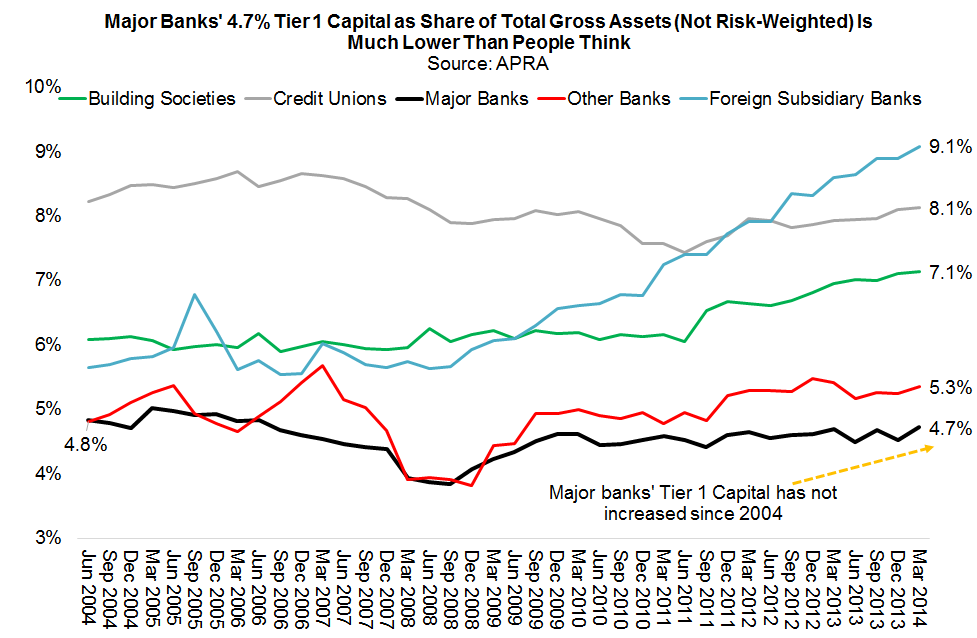

…Our analysis finds that the majors’ tier one capital relative to the dollar value of loan assets has declined from 7.3 per cent in 2004 to 6.9 per cent in 2014.

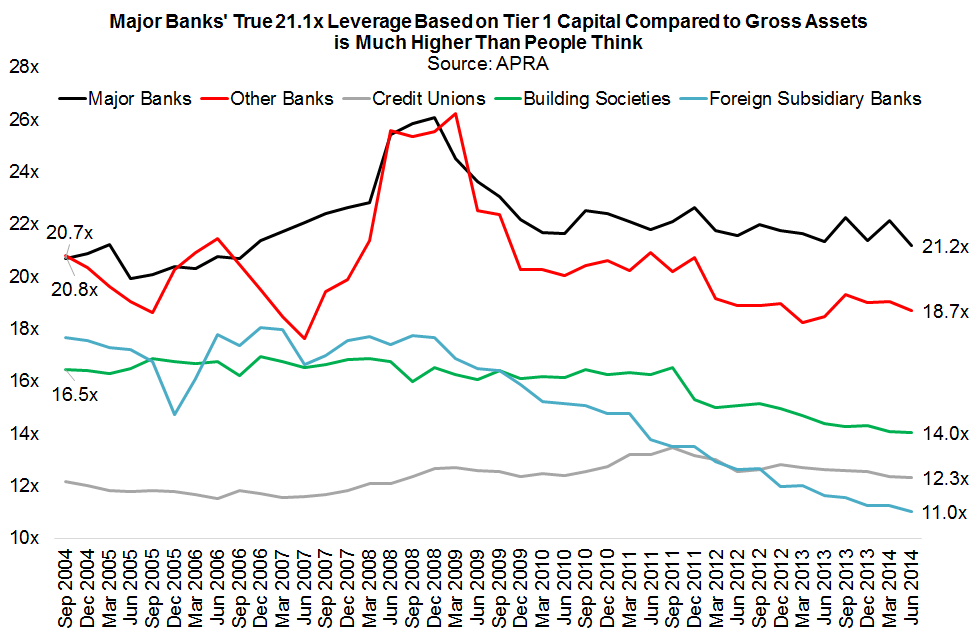

Relative to total assets, tier one capital has gone from 4.8 per cent to 4.7 per cent. Contrary to popular myth, major bank leverage has increased, not decreased, over this period from 20.7 times to 21.1 times.

…The policy answer is not allowing governments to bail out banks by unilaterally converting debts into equity in a crisis. The banks need to hold more equity in the first place, which they will furiously resist.

This is the very heart of the Australian housing bubble. I suggest you read it in full.

Advertisement

Charts republished with permission from the author.

David Llewellyn-Smith is Chief Strategist at the MB Fund and MB Super. David is the founding publisher and editor of MacroBusiness and was the founding publisher and global economy editor of The Diplomat, the Asia Pacific’s leading geo-politics and economics portal.

He is also a former gold trader and economic commentator at The Sydney Morning Herald, The Age, the ABC and Business Spectator. He is the co-author of The Great Crash of 2008 with Ross Garnaut and was the editor of the second Garnaut Climate Change Review.