Sighhhh. I’ve written about this in detail a few years ago but nothing has changed and the deceit continues. All of Mega Bank’s divisions continue to present to the market deceptive figures about the strength of their balance sheets and the amount of capital Mega Bank holds compared to banks in other parts of the world. Mega Bank asserts that because APRA has harsher rules in some capital calculations under Basel requirements that its capital ratios when compared to banks in other jurisdictions should be higher, thereby representing greater balance sheet strength. Whilst this claim is based on an Australian Banker’s Association report of 6 or 7 years ago, is not only dubious, IMHO its down right deceptive.

In order to substantiate my claims, I refer you to CBA’s latest result presentation for the half year to Dec 2013.

In essence, the CBA presents that it has better capital ratios when compared to banks regulated by regulators in other jurisdictions than APRA insists it calculates and reports under Australian regulation. Whilst generally, jurisdictions that follow Basel Committee rules on capital calculations use the same calculation rules there is some discretion in the hands of local regulators as well as unknown variation within internal models. So differences do exist, which is why there is an international movement for greater transparency in reporting capital calculations which I reported on a few weeks ago.

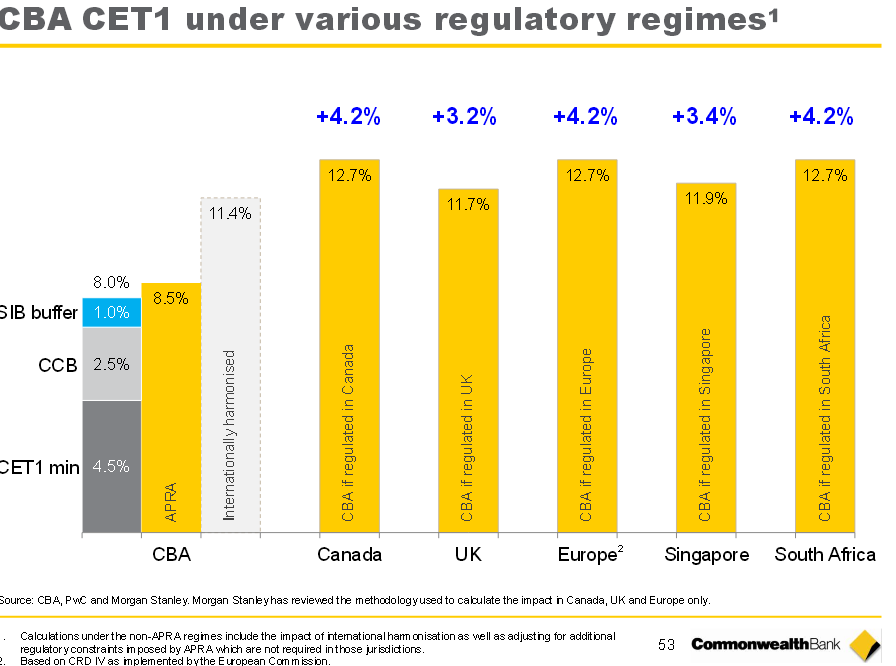

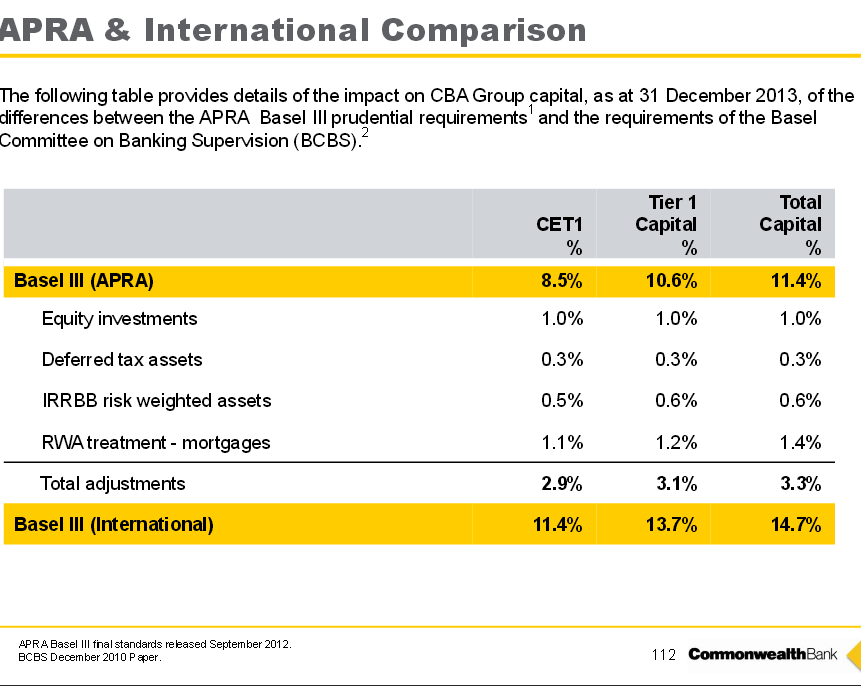

This is not a trivial or minor part of CBA’s reporting. CBA reports that whilst its CET1 ratio by APRA is 8.5% it’s a much more healthy 11.4% under international comparisons. The adjusted CBA capital calculation which gives the impression of a stronger balance sheet is referred to in eleven slides in CBA presentation (Slides 4, 19, 49, 51, 53, 55, 57, 58, 112, 113 and 115). So one can conclude its not a trivial matter for CBA. Slide 53 is reproduced below as just one example of CBA’s own capital adjusted calculation compared to offshore banks. Has APRA approved this calculation or reported it to the market?

So what actually is the problem?

Whilst there are 4 areas where CBA reports favourable adjustments, see below, let’s just look at the adjustment that CBA makes for residential mortgages as this is the largest single adjustment and straight forward to challenge.

CBA reports and presents to the market analysts and its shareholders that due to APRA imposing harsher parameters on the calculation of risk weighted assets for residential mortgages that it can add 1.1% to its capital for an analyst or anyone else to compare its capital ratios to offshore banks. For this to be the case, then the regulator in the other jurisdiction must be forcing its banks to use exactly the same calculation and method to calculate risk weighted assets, except for the different calculation parameter that APRA imposes. Is this the case?

CBA claims, and so does all the other divisions of Mega Bank, that the significant difference between APRA requirements and other regulators is the Loss Given Default (“LGD”) required to be used in the internal risk based (“IRB”) models which are used to calculate minimum capital requirements is 20% for residential mortgages whilst other regulators stipulate 10% (Slide 113). This seems to be a straight forward calculable difference, but as the following demonstrates its neither straight forward nor reliable:

- IRB models to calculate RWAs are just that, internally generated models and no two are the same. There is currently much debate amongst global regulators about how IRB models produce such widely varying results both across and within jurisdictions. It’s most unreliable to assume that for residential mortgages, banks in other jurisdictions have the same IRB models except for a single LGD parameter.

- To calculate RWAs, an expected loss measure is calculated which is the product of LGD and Probability of Default (“PD”). Unless one knows the PD formula other regulators or banks use in their IRB models, its simply not possible to calculate reliably the effect of a change in LGD.

- The LGD of 10 % set out by the Basel Committee and used by other regulators is a floor or minimum not a maximum. Regulators in other jurisdictions do not simply apply an LGD of 10% to every loan. LGDs, as is sensible are recognized as higher for higher LTV loans eg >90%. It’s actually not unreasonable to assume that the difference in minimum LGD has very little effect across jurisdictions in the calculation of RWAs for residential mortgages. So how can CBA make such a confident claim that a very large difference exists?

- Its not possible to understand how CBA calculates the 1.1% capital comparison pick-up as very little information is supplied. However, I believe I can show the absurdity of the number by a simple analysis of the CBA Pillar 3 disclosures.

- The Pillar 3 disclosures report that the IRB RWA weighting for residential mortgages is 17.6% which when multiplied by the standard 8% capital requirement gives a minimum capital requirement of 1.4% against the actual balance of the mortgage book used in the IRB models. Although this is an impressively small number, its nowhere near as small a number as is assumed that an offshore regulator would calculate for CBA.

- For CBA to make a claim on that there is a comparison pick up of 1.1%, then there must be an assumption that regulators in those jurisdiction outlined above and as cited by CBA, for RWA purposes weight residential mortgages at 5% with minimum capital requirements of just a tiny 0.4%. I’m sure the Prudential Regulatory Authority in the UK would be happy to present the UK’s banks to the world as having such miniscule RWAs for residential mortgages and gearing of 200:1. Of course this is an absurd proposition!

Whilst I’ve kept this post to addressing the residential mortgage comparison, I also believe that the other adjustments above may also have some issues. I cannot believe it’s likely that regulators in other jurisdictions do not require interest rate risk on the banking book (“IRR BB”) to be taken into account in their banks’ IRB models.

What does all or any of APRA, ASIC or the ASX think about reporting such patently incorrect claims of capital strength? Where are the savvy equity analysts in the Australian market that can pick up this misreporting and grill the banks about it?

It’s not just CBA that makes these dubious claims, its all of the Divisions of Mega Bank so this is a serious system transparency problem which must be addressed.