Standard and Poors has a new report out in which it examines the prospects for iron ore miner debt ratings if the commodity remains at $90:

If iron ore prices stay at current prices of about US$90 per ton through 2015, the key credit metrics of some mining companies might worsen significantly, based on a scenario analysis on 10 major iron ore producers.

• Mining companies that have substantial debt or expensive operations will bear the brunt of the impact.

• The ultimate rating impact depends critically on a mining company’s financial flexibility, such as its ability to defer or delay capital expenditure and conserve cash.

• Diversified mining companies are well placed, as they can then rely on commodities with more resilient prices, such as oil.

• Another important factor is the movement of mining companies’ local currencies, which could affect their costs and revenues.

Pretty obvious stuff. So, who’s at risk and what would trigger a downgrade?

Whether this deterioration triggers a downgrade depends critically on a mining company’s financial flexibility. If a miner can defer its capital expenditure and conserve cash, its credit quality should be able to withstand sliding iron ore prices. In addition, diversified mining companies are well placed, as they can rely on commodities with more resilient prices, such as oil. Another important factor is the movement of mining companies’ local currencies, which could affect their costs and revenues.

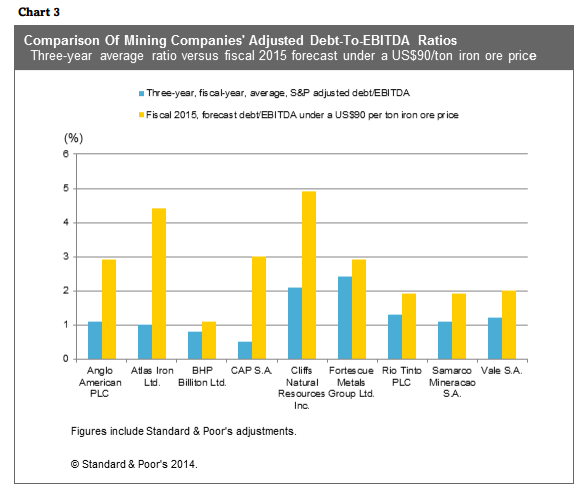

We observed that major players—Australia’s BHP Billiton Ltd. and Rio Tinto PLC, and Brazil’s Vale S.A.–can accommodate declining earnings should iron ore prices stay at US$90 per ton through to the end of 2015 (see table 1). Nevertheless, their rating buffer will reduce under this scenario. As such, they will have less flexibility at the current ratings to undertake debt-funded growth or capital-management initiatives. For example, lower iron ore prices, together with high debt associated with the Brazilian government’s tax could increase Vale’s leverage ratio (measured by adjusted net debt to EBITA) to levels close to our downgrade trigger of 2x in fiscal 2015, from a low 1x in the pastthree years (see chart 3).

Other iron ore miners, Australia’s Fortescue Metals Group Ltd. (FMG) and Brazil’s Samarco Mineracao S.A., too, should have sufficient buffer in their credit metrics to absorb the lower iron ore prices, notwithstanding the moderate impact on their earnings. Despite Samarco’s decrease in earnings, we believe the company’s credit metrics would remain firmly within our expectations for the “intermediate” financial risk profile. Likewise, FMG’s key credit ratio under this pricing threshold remains commensurate with its “aggressive” financial risk profile. The modest rise in its debt-to-EBITDA ratio is not because FMG is more resilient to iron ore price volatility, but because its heavy capital expenditure to expand its capacity affected the three-year ratio average. However, the weaker iron ore prices could slow down its deleveraging.

On the other hand, downward rating pressures could arise for Australia’s Atlas Iron Ltd., U.S.-based Cliffs Natural Resources Inc., and South America’s CAP S.A. Under this hypothetical pricing scenario, Atlas Iron’s earnings could slip steeply. Weaker earnings, together with high debt following the term loan B issuance in 2012, could significantly increase its leverage and pressure its credit metrics in the absence of remedial actions taken by the company. Similarly, Cliffs would also face downward rating pressure. Cliffs’ high cost structure and leverage profile following its acquisition of Consolidated Thompson Iron Mines in 2011 reduced its ability to absorb earnings deterioration at its current rating. We believe near-term leverage measures would fall into the “aggressive” category without further direct action from the company to reduce debt, regardless of its current capital preservation plans. Likewise, CAP’s adjusted debt to EBITDA could rise to more than 2x under this pricing scenario, exerting downward pressure on the rating.

Advertisement

The implications here for equities is obvious. If capital management opportunities like buy-banks dry up then that’s a blow. Reduced capex hurts future growth prospects. The next domino would be dividends. Not a lot to cheer about.

David Llewellyn-Smith is Chief Strategist at the MB Fund and MB Super. David is the founding publisher and editor of MacroBusiness and was the founding publisher and global economy editor of The Diplomat, the Asia Pacific’s leading geo-politics and economics portal.

He is also a former gold trader and economic commentator at The Sydney Morning Herald, The Age, the ABC and Business Spectator. He is the co-author of The Great Crash of 2008 with Ross Garnaut and was the editor of the second Garnaut Climate Change Review.