As noted by Houses and Holes earlier, the University of Canberra National Centre for Social and Economic Modelling has released new analysis showing that in the absence of tax cuts, the effect of people being pushed into higher tax brackets because of inflation (“bracket creep”) would increase total personal income taxes by 21% or $32.5 billion within a decade.

While such ‘taxation by stealth’ would go a long way to restoring the Federal Budget back to balance, it poses great risks for the Australian economy and the social fabric.

First, as argued by Professor John Freebairn today, the collection of each dollar of personal income tax costs the economy between 30 cents and 40 cents, making it a relatively inefficient tax. An escalation in personal tax collections would, therefore, be a major drag on productivity, reducing Australia’s growth potential and living standards.

Second, allowing personal taxes to rise ahead of other forms of taxation risks creating a nation of working tax slaves, as today’s generation Xers, Ys and Zs are forced to pay more tax (and consume less) in order to fund the growing army of retired Australians, many of whom also enjoy generous taxpayer entitlements.

Clearly, Australia desperately needs fundamental tax reform. But what exactly?

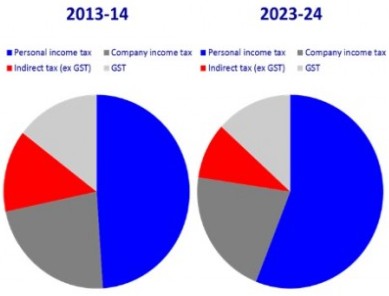

As shown below, the Federal Budget is primarily funded via four forms of taxes:

- Personal taxes, which comprise roughly half of all revenue, and will increase their share without reform;

- Company taxes, which comprise less than a quarter of revenue;

- GST, which comprises around one-sixth of revenue; and

- Indirect taxes, such as fuel excise, whose share is similar to GST, but projected to shrink over time, since it is no longer linked to inflation.

Raising company tax is not a viable option for Australia. As noted yesterday, Australia already has one of the highest reliance on company taxes in the OECD. The Henry Tax Review also found that company taxes are one of the most distorting forms of taxation going around, with a “marginal excess burden” – i.e. the loss in consumer welfare relative to the net gain in government revenue – of 40%, because “it is applied to capital, which is highly mobile” (see next chart).

Clearly, boosting the GST and/or reinstating indexation of fuel excise are good options. Again, according to Professor John Freebairn, both taxes are highly efficient and “changing the tax mix from (income taxes to indirect taxes) brings gains of 20c to 30c in the dollar and beats anything that a major corporation could do on productivity”. The Henry Tax Review supports Freebairn’s claim, with a marginal excess burden arising from the GST of just 8%, because it is broadly applied, is difficult to avoid, and does not significantly distort behaviour.

Unfortunately, the Government has so far shown minimal interest in broadening or raising the GST. During last year’s election campaign, Tony Abbott ruled-out changing the GST, not only for this term but altogether, stating: “The GST will not change. Full stop. End of story”. While nothing is ever set in stone, and the Coalition’s position can always change (just as it did under John Howard), it does make reform less likely. Meanwhile, reinstating the indexation of petrol excise could be even more unpopular, particularly if petrol prices begin to rise as the Australian dollar trends lower.

As noted yesterday, the Government could also look to raise taxes through broad-based land taxes and resource rent taxes. While not shown in the chart above, both taxes would have similar efficiency to the Petroleum Resource Rent Tax (PRRT) and Municipal rates, since they would be applied to a tax base that is completely immobile – land. They are also more equitable than consumption taxes.

A broad-based land tax would also have more favourable distributional impacts than the GST, and would effectively boost land supply and help make infrastructure investment self-financing for governments.

Again, reform in these areas would also be very difficult. Wealthy, well connected, landholders would likely scream blue murder if a land tax was introduced (effectively removing a comfy tax haven), whereas the Government has obviously painted itself into a corner on resource rent taxes, given that it lobbied so hard against “Labor’s great big tax”.

Ultimately, fundamental tax reform is essential if Australia is to achieve the types of productivity reform required to grow living standards as the population ages. But reform won’t be easy, and will require strong political leadership and a retreat from entrenched ideological positions.

unconventionaleconomist@hotmail.com