Martin Conlon, head of Australian equities at Schroders Investment Management Australia, has delivered a stern warning about the debt-based structure of the economy, which has seen excess credit flow into housing at the expense of productive enterprises. From The AFR:

‘‘The economy remains an action replay of the structure that gave rise to the financial crisis – an ever narrowing economy based on asset price speculation and ever lower interest rates’’…

‘‘Call us sceptical, but without change in structure or incentives, we have an uncomfortable feeling that same policies will eventually give rise to the same problems.’’

Since the financial crisis, banks have been forced to become more cautious about how they lend to businesses and place a higher priority on mortgages.

…‘‘a financial system which continues to grow at rates beyond the income which supports it becomes progressively more unstable’’.

‘‘The unknowable is when this happens and what further extraordinary steps will be taken in attempting to preserve the status quo”…

‘As speculative excess builds, asset prices are rapidly becoming the reason for optimism on future growth rather than an outcome of policies which restore economies to a sustainable footing’’.

Looking at the data, there is truth in Conlon’s claims.

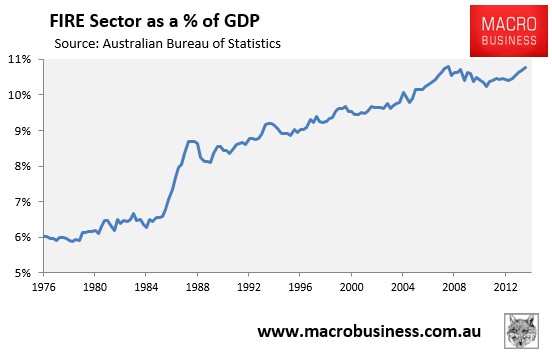

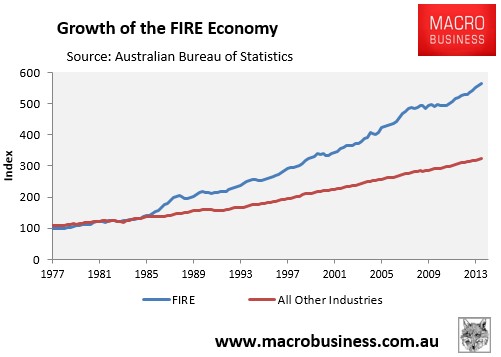

As illustrated last week, Australia’s Finance, Insurance and Rental, Hiring & Real Estate Services industry’s (the “FIRE economy”) hit an equal record high 10.8% share of GDP in December, and have grown at nearly twice the pace of the rest of the economy since financial markets were first deregulated in the mid-1980s (see below charts):

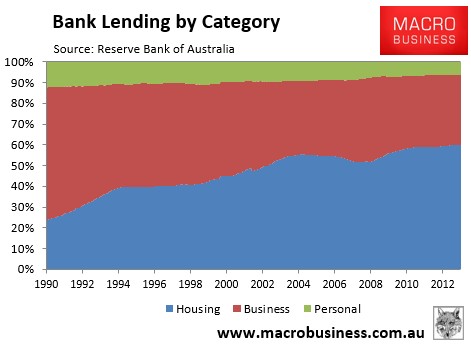

Moreover, housing’s total share of lending hitting a record high 60.2% of in January 2014, just as business’ share hit a record low of 33.4% (see next chart).

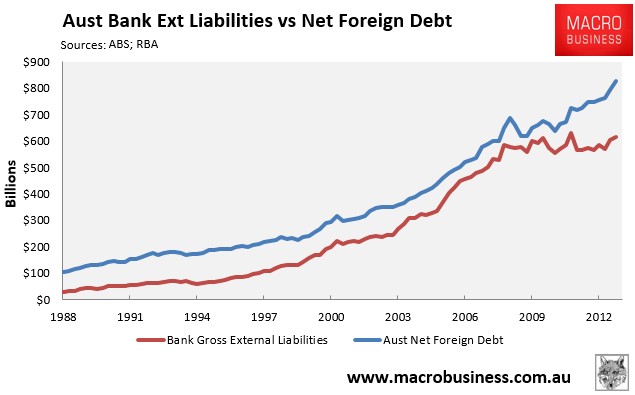

And to add further insult to injury, much of the boom in mortgage lending has been funded by heavy offshore borrowing by Australia’s banks, in turn driving-up Australia’s net foreign debt and the Australian dollar:

So for decades, resource allocation in Australia has been channeled away from the tradable sector and infrastructure investment towards the financial sector, as home buyers have taken on ever-bigger mortgages as they chased house prices higher.

At the heart of the problem is the housing quango operated by the various levels of government.

As argued yesterday, Australia’s tax system makes investment into housing a relatively attractive proposition via a combination of high tax rates on savings, as well as tax generous concessions like negative gearing and capital gains tax discounts. As a result, demand for housing is higher than it otherwise would be.

At the same time, a myriad of constraints on housing supply such as urban consolidation policies, cumbersome planning approval processes, and high taxes and charges on new homes have forced-up the costs of development, impeding the market’s ability to supply affordable housing and significantly dampening the supply response.

The end result is that too much of the nation’s capital is being tied-up in housing, which is chocking-off productive areas of the economy.

The Australian economy would likely be on a far more balanced and sustainable footing if the billions of dollars of excess capital that had been poured into pre-existing housing had instead been funneled into businesses and infrastructure. Instead, we have been left with non-mining companies that are struggling to compete and a gigantic infrastructure deficit, which is crimping both productivity and living standards.

This is why Australia’s tax system requires widespread reform so that it rewards productive investment over speculation, in addition to liberalising the myriad of constraints on land supply and planning that force-up urban land prices, raising business costs and wages.

unconventionaleconomist@hotmail.com