Remember that BIS study that found a secret cache of foreign denominated emerging market debt in corporate bonds? Some goods news today from Nomura via FTAlphaville, its not so big:

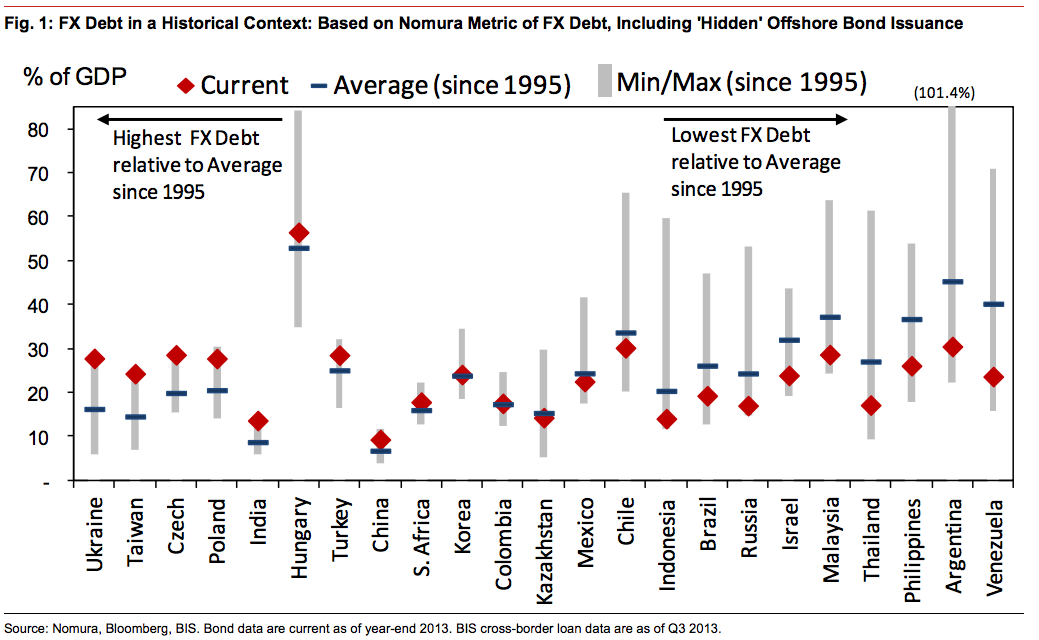

Current levels of hard currency external debt in emerging markets (focusing on bonded debt and bank loans) are not high from a historical perspective. In fact, for the majority of the EM countries in our sample, the hard-currency debt exposures are below the average of the last 20 years.

There are exceptions to this pattern, and they include Ukraine, Taiwan, and the Czech Republic. But for most countries, the foreign currency exposures in themselves do not look problematic. In Taiwan’s case, for example, there are very considerable FX assets on the country’s balance sheet, which means that net FX liabilities are not a real concern. More broadly, we generally do not view the size of FX debts in emerging markets as sufficiently large to create a negative feedback loop from currency weakness into increased debt burden and weak growth.

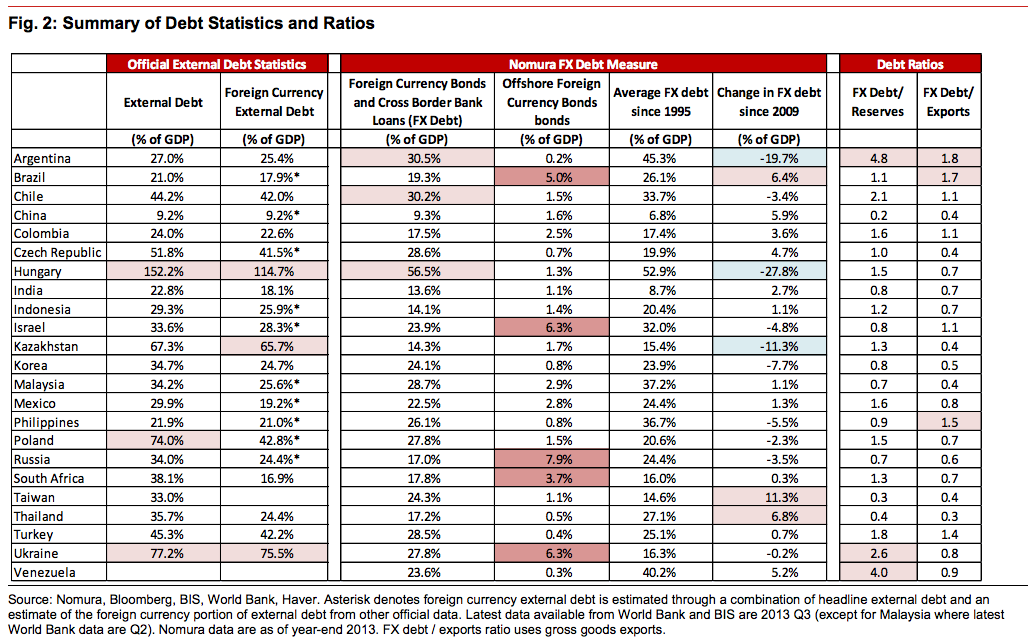

Corporate debt issuance (in foreign currency) has increased substantially in recent years. We estimate that the total outstanding corporate EM debt in hard currency has increased from $596.8bn at the end of 2009 to $1303.1bn at the end of 2013, including offshore issuance. But this has not led to a broad-based increase in FX debt at the macro level. In the many EM countries, the overall level of FX debt as percentage of GDP has actually gone down. One important part of the explanation is that sovereign debt issuance has tended to be concentrated in local currency, and government foreign currency debt has grown more slowly than GDP. This conclusion holds even when including ‘hidden’ debt (i.e., debt issued offshore), which is not necessarily included in traditional residency-based external debt statistics from official sources.

This is no guarantee that EM currencies will not adjust lower over time. Some EM countries are experiencing weakening growth, and a weaker currency may be a natural component of the adjustment process. But having more resilient balance sheets, with moderate amounts of hard currency debt, does mean that the risk of substantial overshooting (for FX and other assets) is fairly low for the majority of emerging markets (or that the cause of the overshooting will come from a different source than the debt exposures themselves- e.g. political risk). Moreover, the negative carry involved in short EMFX positions has increased over the past 12 months and makes it increasingly expensive to trade EM currencies from a bearish stance.

For China the numbers are a likewise manageable $169bn offshore:

This has important implications for how any downturn in the Chinese economy and credit markets will spread globally. It will be much less about portfolio contagion, and more about real economic channels and transmission through regional and global growth, as well as through commodity prices.

Advertisement

Indeed this is good news if true. This was one of the two major financial contagion risks in the event of a Chinese and emerging market meltdown that I track. The other being unexpected linkages between the commodities complex and banks.

Though I’m not completely reassured. A Chinese hard landing would still cause an emerging market recession and likely hit developed market stock markets very hard via falling corporate profits. But it’s better than GFC 2.0!

David Llewellyn-Smith is Chief Strategist at the MB Fund and MB Super. David is the founding publisher and editor of MacroBusiness and was the founding publisher and global economy editor of The Diplomat, the Asia Pacific's leading geo-politics and economics portal.

He is also a former gold trader and economic commentator at The Sydney Morning Herald, The Age, the ABC and Business Spectator. He is the co-author of The Great Crash of 2008 with Ross Garnaut and was the editor of the second Garnaut Climate Change Review.