The Bank of International Settlements has warned that contrary to the reassuring words of “analysts” everywhere, emerging markets are vulnerable to a liquidity squeeze and it has identified the mechanism of why:

“The deeper integration of emerging market economies into global debt markets has made emerging market bond markets much more sensitive to bond market developments in the advanced economies…The global long-term interest rate now matters much more for the monetary policy choice facing emerging market economies than a decade ago.”

Although much of this should be captured in the oft-quoted “better than last time” balance of payments defense that this crisis will be limited, the BIS describes how official data is not picking up the big external imbalances:

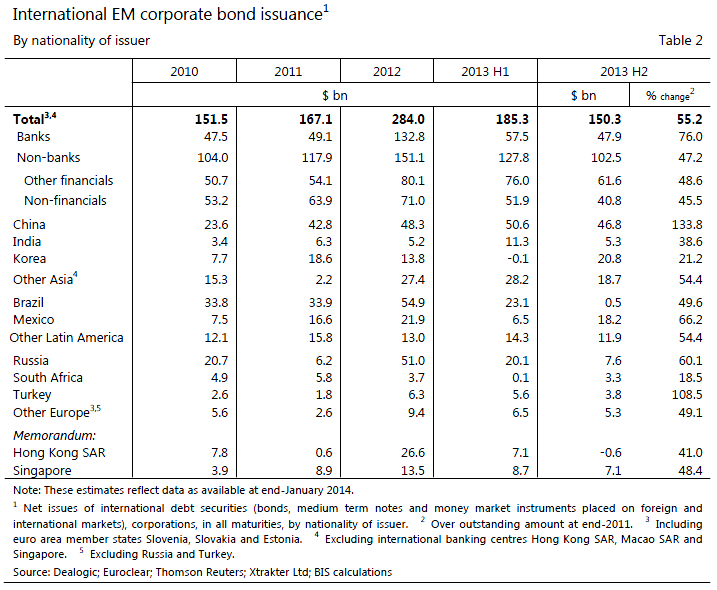

Table 2 summarises international bond issuance excluding government and the central bank – and so corresponds approximately to the corporate sector. Some corporations, however, are wholly or partly owned by government so this is not equivalent to the private sector: some Brazilian and Chinese state-owned enterprises have been prominent issuers. Over the period 2010 to the first half of 2013 inclusive, corporate net issuance on a nationality basis amounted to $788 billion (of which, about $500 billion by non-banks). Despite turbulence in global bond markets from May 2013, net bond issuance remained quite strong in the second half of 2013.

Much of this borrowing was through these companies’ overseas subsidiaries – including their offshore financing vehicles – rather than by entities in the countries where these firms are headquartered. This latter measure (ie residence-based) of bond issuance is shown in Table 3. The total from 2010 to the first half of 2013 amounted to about $410 billion (Table 3). Hence 48% of EME corporate issuance on a nationality definition during this period was through their overseas affiliates. (See the further analysis in McCauley et al, 2013).4 To underline a point made earlier: borrowing through overseas subsidiaries are normally not included in balance-of-payments measures of capital inflows, which capture residence-based transactions.

Advertisement

As international liquidity dries up, these firms needs to refinance locally, which begins to drag in local banks via spiking interest rates, rationing of credit and possible derivative counter-party risks through FX and interest rate hedges.

The crucial point is that this potentially drags in all emerging markets, not just those with obvious balance of payments imbalances.

So much for the borrower. More work has been done on this from the perspective of the lender as well, in a Princeton paper called the Second Phase of Global Liquidity:

Advertisement

Given the elements that have underpinned the Second Phase of Global Liquidity, the crisis dynamics in the emerging economies would then have the following elements:

1. Steepening of local currency yield curve

2. Currency depreciation, corporate distress, and runs of wholesale corporate deposits from the domestic banking system

3. Decline in corporate capital expenditure feeding directly into a slowdown in economic growth

4. Asset managers cutting back positions in EME corporate bonds citing slower growth in the emerging economies

5. Back to Step 1, thereby completing the loop.

The distress dynamics sketched above has some unfamiliar elements. We normally invoke either leverage or maturity mismatch when explaining crises and the usual protagonists in the crisis narrative are banks or other financial intermediaries. In contrast, the scenario sketched above has asset managers at its heart. We find this unsettling, as long-only investors are meant to be benign, not create vulnerability. They are routinely excluded from the list of “systemic” market participants.

However, the distinction between leveraged institutions and long-only investors matters less if they share the same tendency toward procyclicality. Asset managers are answerable to the trustees of the fund that have given them their mandate. In turn, the trustees are themselves agents vis-à-vis the ultimate beneficiaries. In this way, asset managers lie at the end of a chain of principal-agent relationships that may induce restrictions on their discretion to choose their portfolio. Frequently, the trading restrictions are based on measures of risk, used by banks and other leveraged players. As such, their behavior may exhibit the same type of procyclical risk taking that banks are known for. The uncomfortable lesson is that asset managers may not conform to the textbook picture of long-term investors, but instead may have much in common with banks in amplifying shocks.

That’d be ye auld hot money at work. But if central banks crush your yield then what choice have you? Welcome to the Bernanke reckoning.

David Llewellyn-Smith is Chief Strategist at the MB Fund and MB Super. David is the founding publisher and editor of MacroBusiness and was the founding publisher and global economy editor of The Diplomat, the Asia Pacific’s leading geo-politics and economics portal.

He is also a former gold trader and economic commentator at The Sydney Morning Herald, The Age, the ABC and Business Spectator. He is the co-author of The Great Crash of 2008 with Ross Garnaut and was the editor of the second Garnaut Climate Change Review.