UBS has terrific note today on Gina Rinehart’s Roy Hill, including some estimates on what we’ve all been waiting for, break even cost:

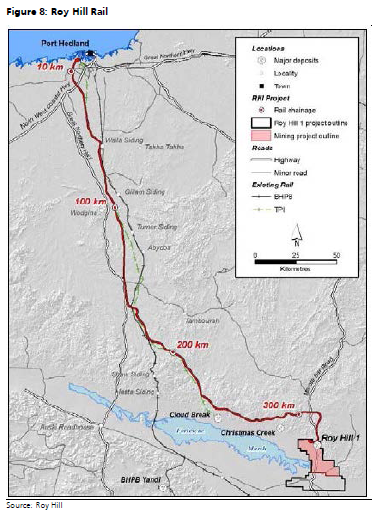

The Roy Hill mine is planned to ship through Port Hedland alongside major producers BHP Billiton and FMG. The Roy Hill mine is located in close proximity to FMG’s Cloudbreak and Chichester mines & has planned production of 55Mtpa to match its Port Hedland capacity allocation. First ore on ship (FOOS) scheduled for Sept 15.

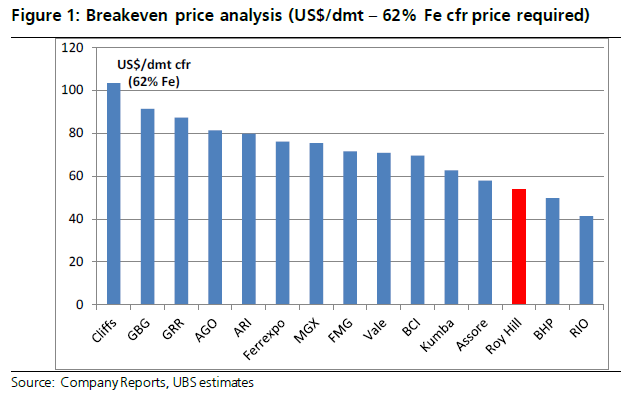

We estimate C1 costs of ~A$30/wmt fob pre royalties. Grade is ~61% Fe (~60% Fe beyond Yr 11) with a product split of 60% fines & 40% lump. Mine life is ~20 years based on reserves of 1Bt, plus there is an additional 1.1B of low grade/detrital ore (not modelled). Based on the UBS price deck for iron ore (7% pa decline from US$126/dmt to LT price of US$89/dmt cfr 62% Fe in 2017) and LT A$ of US$0.85, we estimate an NPV of ~$5.7bn (8% real disc. rate) with a 15% IRR. The break-even price is estimated to be US$54/dmt cfr (62% Fe equiv.).

We understand Roy Hill is prepared to consider 3rd party access/haulage once funding is complete. We believe the benefits to Roy Hill are an additional income stream, redundancy and lower capital intensity. Atlas and Brockman, both of whom have 50Mtpa of combined shipping entitlements are the most likely candidates.

Roy Hill is already in our supply/demand model with 15Mt in 2016 and 55Mt in 2019. Additional tonnage from any new entrants that benefit from Roy Hill is not included, but their possible entry in 2017 is unlikely to materially impact our view given the oversupply we forecast and we are at our LT price of US$89/dmt cfr (62% Fe) in 2017.

So there you have it. Roy Hill is cheap! No wonder it got funded. This flies in the face of commodity economics, which says that the cheapest gets developed first, but maybe Gina’s dream of propriety has delayed it. Based on these figures, the real mystery is not why RH got funded but why it took so long.

Now let’s analyse this with a slightly harder nose.

Advertisement

I don’t agree with the Vale estimate. First, it has many mines, most of which are far cheaper than the aggregated price. Moreover, it has something of a captured indigenous market in South America so many of its more expensive mines can still operate and sell locally at prices that others can’t ship in at. That frees its cheaper material for wider export so it’s nowhere near as vulnerable as this cost curve suggests.

Ferrexpo is an interesting one given its Ukraine exposure, so that could work in Australia’s favour. Others calculate FMG’s real break even at more like $80. I agree.

Given the dynamics at large in the iron ore market, and the clear drive in China to rebalance (albeit on an acceptable glide path) UBS’s iron ore price forecasts are too high. The Goldman Sachs projections of $108 this year and $80 next look right to me and the risk is greater volatility sooner, not the other way around.

The inescapable conclusion is Australia’s iron ore juniors are dead men walking, and FMG is sitting right on the market’s swing production.

Advertisement

Gina is sitting pretty and given the proximity of her assets to those of Andrew, one wonders what she’s got her eye on:

David Llewellyn-Smith is Chief Strategist at the MB Fund and MB Super. David is the founding publisher and editor of MacroBusiness and was the founding publisher and global economy editor of The Diplomat, the Asia Pacific's leading geo-politics and economics portal.

He is also a former gold trader and economic commentator at The Sydney Morning Herald, The Age, the ABC and Business Spectator. He is the co-author of The Great Crash of 2008 with Ross Garnaut and was the editor of the second Garnaut Climate Change Review.