Asia-Pacific Banking & Finance has reported today that the Basel Committee on Banking Supervision (BCBS) has clashed with the Australian Prudential Regulation Authority (APRA) on the treatment of investment property loans, with BCBS claiming that Australian banks are not being required by APRA to hold enough regulatory capital to cover risks against these exposures:

Under Basel III, banks using the internal-ratings based approach (IRB) can treat home loans as lower-risk retail exposures as long as they are for owner-occupiers. However APRA also allows the four major banks and Macquarie that use the IRB approach to include residential investment property loans as retail exposures.

The BCBS noted approximately one-third of the five banks’ home loan portfolios are investment property exposures and, despite APRA’s arguments to the contrary, it isn’t clear how they would perform during an economic downturn like Australia experienced in the 1990s.

“Accordingly, the likely potential risk for capital understatement that could result from APRA’s current treatment of non-owner occupied mortgages was considered material.”

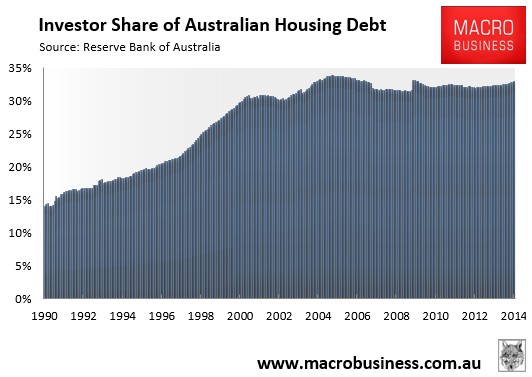

According to the Reserve Bank of Australia, 34% of outstanding residential mortgages were to investors as at January 2014 (see next chart).

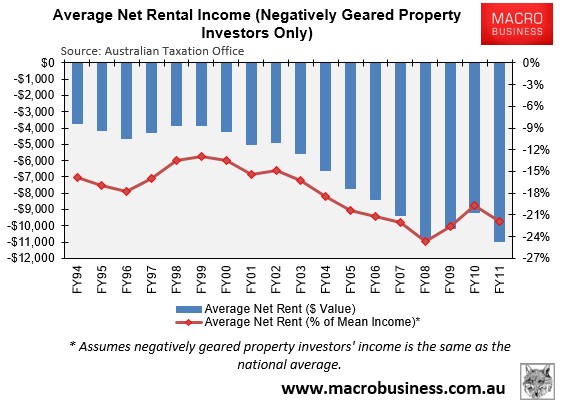

Given that around two-thirds of property investors (circa 1.2 million) are negatively geared, with each negatively geared investor declaring losses on average of $10,900 per annum to the ATO in 2010-11 (see next chart), there is the ever present danger that many property investors could run into trouble in the event that there was a severe economic downturn leading to the widespread loss of jobs.

Combined with Australia’s negative gearing laws, APRA’s lax treatment of investment property loans is likely to have contributed to Australia’s over-investment in property, which apart from raising financial stability risks, has choked-off productive areas of the economy.