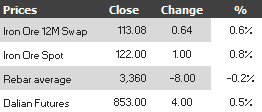

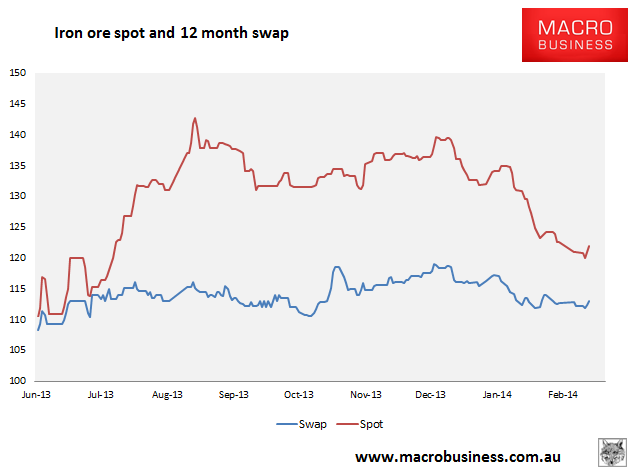

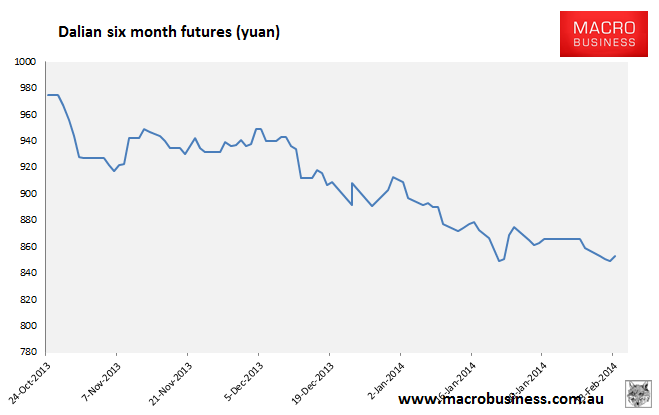

Find below the iron ore price charts for February 13, 2014:

A little reprieve for iron ore but not steel. Some post-holiday demand is reappearing then. To explore what kind, let me bring your attention to a comment by reader Researchtime yesterday on my extra post about the “cash for iron ore” scams that appear to be driving the great Chinese stockpile:

Chinese iron ore traders, without exception, use enormous amounts of debt to finance the transport iron ore, largely on spec. Moreover, they still make up a significant portion of the iron ore market in China, with only the majors have long standing contracts with major steel producers (although in saying that, there is some Robe River spec available apparently). It has been a highly profitable venture for near on a decade with continuing high prices.

The problem is for many of these traders is when the steel mills don’t want their product, they have to file for bankruptcy, given traders don’t have any financial capability to sustain their contractual obligations, particularly with Australian junior I.O. producers. I think the majority of investors have no idea what a precarious industry this is.

If one recalls a year ago, there was quite a sharp drop in iron ore prices– at the time, it appeared that the vast majority of trading houses would simply disappear. Those who took delivery on iron ore shipments, and managed to roll over their debt repayments, were able to sell it at enormous profits (given this is margin expansion business) just several months later as prices jumped from around $90/t to $150/t. Much of this was driven by supply shortages bought on by 100mt of Indian supply just going off-line (the current PM was Resource minister at the time many mining licenses were issued under very dubious circumstances). The Chinese banks also were let of the hook, potentially having enormous amounts of iron ore collateral with no real market.

However, I fear that the wrong lessons have been learnt from that episode, by all concerned. If demand drops and/or Indian and continued growth in Australian (especially from Rio) supplies add pressure to an already slowing construction market – we could see a massive squeeze – from which there will be no future price rebound, or stockpile drop. And I suspect, the banks will continue to finance imports for a while – assuming things will eventually turn around; until even they realise what a catastrophic situation they have created. Then the poo will really hit the fan.

People forget that last year FMG was potentially only a week away from being restructured. Twiggy is no fool – he alone has been the only new major supplier globally (now number four) during this entire decade long mining boom; which is an incredible achievement. And I suspect he ais one of the few who recognises what is just around the corner. How do we know ? Play this game – watch what I do – not what I say… Despite their grandiose talk – FMG finished expansion plans ASAP, on time and budget, knocked all other proposals on the head –THEN – as far as a I am aware, there has never been any faster pay down in history of outstanding debt from a major Australian corporate, which is still ongoing. Make no mistake – Twiggy is a smart (aka wise) cookie. he will not be caught twice !!

Very nicely put and it fits with the current data mix both in terms of market dynamics and company news. It stands to reason that FMG’s mad dash is a significant influence in driving down current prices. Recent surges in Port Hedland shipping data show that FMG must already be approaching its nameplate output of 155 million tonnes of output and there are rumours of growing discounting under contract as well:

FMG uses Platts 62%-Fe Iron Ore Index assessment to price its ore, making a price adjustment for the iron content for each grade, and typically offers its contract customers a discount that depends on market conditions.

For February, the Australian miner sold its flagship product Super Special Fines at a discount of 4% to contractual customers, the same level as in January, sources said.

But for Fortescue Blend Fines, most contractual buyers were offered a discount of 1.5% in February, the same as in January, some major customers were heard to have been given a wider discount of 2%.

A contractual mill customer in central China said that buyers offered a bigger discount for FB fines had probably made an advance payment last year to secure a steady supply of contractual volumes.

FMG has been allocating extra volumes to contract customers as it has increased its production capacity to 155 million mt/year in 2013, from around 120 million mt/year in 2012.

The Tangshan spot billet price, a widely watched gauge of steel fundamentals in China, was Yuan 2,790/mt ($457/mt) on Tuesday. The last time physical billet prices hit this level was on September 4, 2012, and iron ore prices had plummeted to $89/dmt, according to Platts data.

The race is on in earnest. Reserchtime’s commentary continued (and I warn you to grab the scotch at this point):

The collateral provisions would be confidential between the traders and the Chinese banks. But it would be safe to assume that all of the iron ore would be under bank ownership, usually I.O. sales in Australia are done on a FOB basis, with payment made pretty quickly after shipment. There are other provisions for contaminants, (e.g. Al, P – even Fe content, split between fines for sintering and if your lucky, lump). But these are typically later adjustments on a continual basis.

The big losers would be small producers and mining contractors. When (not if) this balloon goes up, iron ore shipments will not just slow down, they will stop – dead. Indefinitely.

There is an historical basis for this. In the run up to 1929, new building techniques allowed (along with the advent of escalators) for the first time massive buildings requiring enormous amounts of steel, especially in the US, at the time amazing building including the Chrysler building, Empire State were completed. As history shows, that peak in iron ore demand was in 1929. From 1929 to 1932, global blast furnace production dropped 50% globally. It didn’t reach its former peak until 1937 (then another market crash), and didn’t then again reach that 1929 level until 1941, several years into WW2. In 1945, it dropped 35% before recovering in late 1948 to 1952, when the Marshall Plan was totally rebuilding Western Europe – coupled with Russia rebuilding as well. Thats a 20 year gap – under some pretty exceptional circumstances.

A couple of unique things about iron ore – its demand actually fuels the growth in demand. What I mean is, take China, it needs rebar for construction. To get more iron ore, it needs additional shipping (that use a lot of steel plate), rail infrastructure (more steel) and blast furnaces (lots more steel), trucks (steel), and building equipment (steel) and associated infrastructure (e.g. cement production – lots more steel). Demand therefore, is self-fulfilling, and it is extremely difficult for the steel producer to discern (assuming they were in the remotest inclined to do so) what is real or underlying demand (lets say for housing) is – compared to what cumulative notional demand suggests, to acquire the necessary infrastructure achieve iron ore supply.

Conversely, that is the simplest explanation I can think of why the steel industry (and by direct relation iron ore industry) always massively over shoots – and there are these enormous demand and supply swings.

So in short, a couple of conclusions:

1 – If China property crashes, a 50% decline in global demand is not unprecedented, and would be my first inclination as a predictor – the affect that would have on the iron ore price, I don’t have a good handle on, that is in the realm of DH at Metalytics – but 50-70% of current price is not unreasonable from a sanguine perspective;

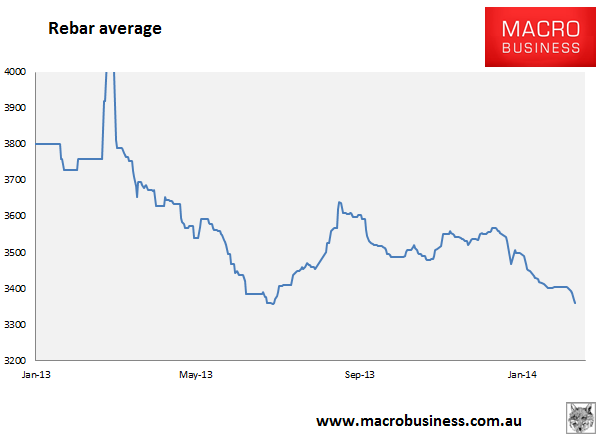

2 – Iron ore prices (although I love looking at them) are in fact a lagging indicator, as are various steel products. Hence macro-businesses obsession with the rebar price (by design or not) is in fact very insightful; and

3 – Realistically, the implications for the Australian mining industry will be nothing short of catastrophic. Remember that Rio’s >75% EBITA is now solely based on Australian IO, a proportion that is continually growing in percentage terms. Rio is no diversified miner – with the amount of current debt and continued expansion – I believe that surely they are a candidate for being restructured (big call I know) – along with every other smaller Australian iron ore producer (bare none) going to the wall. Jim Chanos – I have no doubt, will get the last laugh on this one…

Take it or leave it but you can’t argue with the erudition.

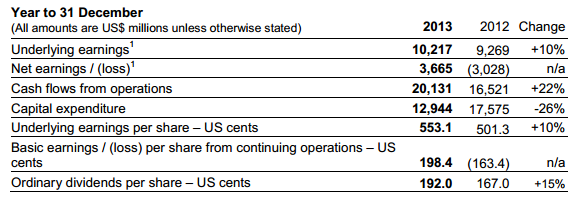

While we’re on the topic, here are Rio’s results:

Above consensus but still an ordinary 3% yield given the risks.

In other news, Sino has struck a blow against our Clive:

…Mineralogy’s argument for having Sino Iron wound-up was based on the non payment of $13.4 million, that Sino Iron allegedly owes Mr Palmer’s company for administrative costs.

…Justice John Gilmour granted Sino Iron an injunction that prevents Mineralogy progressing the wind-up application, until such a time that Mineralogy can prove Sino Iron is insolvent.