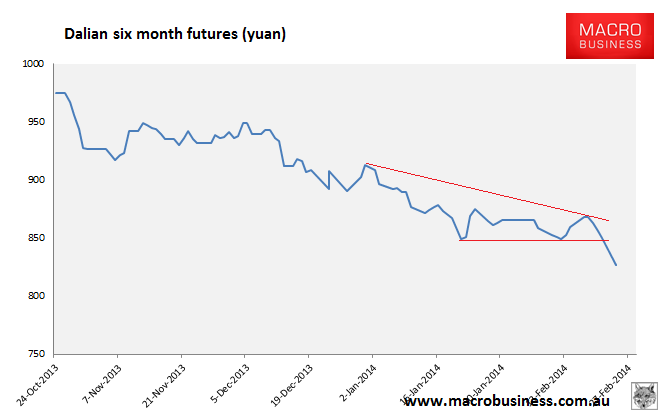

Find below the iron ore charts for February 24, 2013:

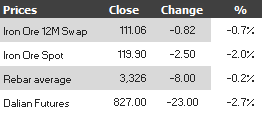

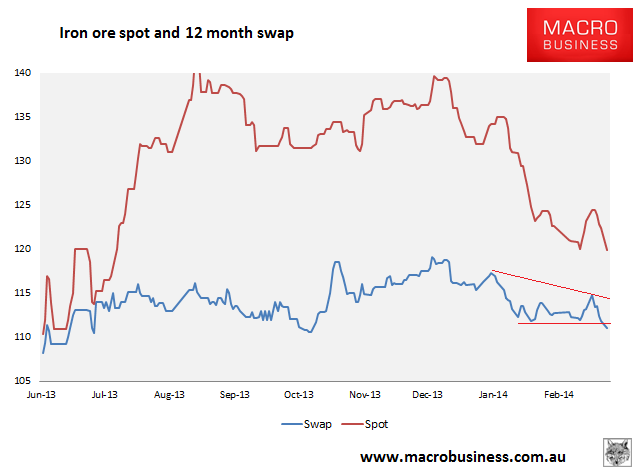

So, the two descending triangles I pointed to yesterday in iron ore paper markets both broke down decisively. I think the 12 month swap is going to take out the $110 support from October last year in short order as well. Iron ore spot also found a marginal new low, which is not so convincing but it’d be a brave man who concluded that it’s not going lower now.

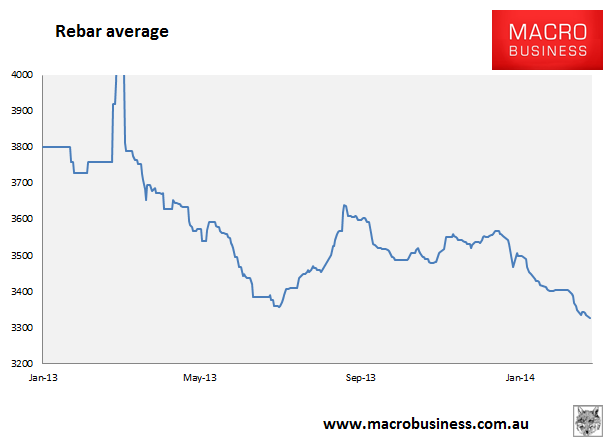

Rebar futures crashed nearly 3% and are now sitting at exactly the same level as physical markets. Backwardation beckons! These markets are increasingly defined by panic.

In news today, Reuters has a nice piece on the rationalisation underway in Chinese steel markets:

Stirred by growing public anger over smog that often spreads to neighboring Beijing, the government summoned Hebei’s leaders to a series of meetings in the capital last year and urged them to draw up plans to slash steel capacity. They eventually agreed on a target of 86 million metric tons, about 35 percent of current capacity, by 2020…last week, Beijing has sent inspection teams to Hebei and elsewhere to see how authorities are responding, and the steel sector is high on their list of targets.

But many mills are already near bankruptcy because of slowing demand, plunging steel prices and a liquidity crisis that would have forced them to shut anyway, experts said.

…On the outskirts of Tangshan, a city of 7 million people that makes more steel a year than the whole of the United States, the hulking cranes and chimneys at the Qingquan Steel mill are frozen in inactivity. Workers unpaid for six months went on strike in October and haven’t returned.

Qingquan Steel is one of dozens of so-called zombie mills in Tangshan, where authorities have been ordered by the provincial government to draw up a list of plants to close so output can be cut by 10.8 million metric tons this year.

“In Tangshan and other parts of Hebei, the private mills are facing the most difficult time in their history,” said Xu. “Profits are poor and producers are all losing money – this has nothing to do with environmental measures: it is the economy.”

…Nevertheless, there has been some resistance.

An industry source said Tangshan had delayed an order to shut down 3 million metric tons of outdated steel production capacity at Tangshan Guofeng Iron and Steel, one of the city’s biggest producers, until next year because it was one of the few firms to make a profit in 2013.

While the Qingquan plant was reprimanded last year by local authorities no longer allowed to overlook environmental violations, orders to install costly new pollution controls would have made little difference to a facility with no access to funds and already incapable of paying its employees.

…”There are many others that have closed even though they haven’t declared bankruptcy. They aren’t formally shut because of the financial implications – they might be in debt and the banks would close in,” said a senior iron ore trader based in Tangshan.

It’s impossible to say how much capacity has and will close but the 30 million tonnes or so flagged in the article represents 4% of China’s 2013 output. For that to transpire, the total loss could probably be offset elsewhere by more efficient producers but the problem is the economic weakness required to bring about the rationalisation will hit all of production if allowed to run.

With Chinese housing slowing as well, it’s on, baby.