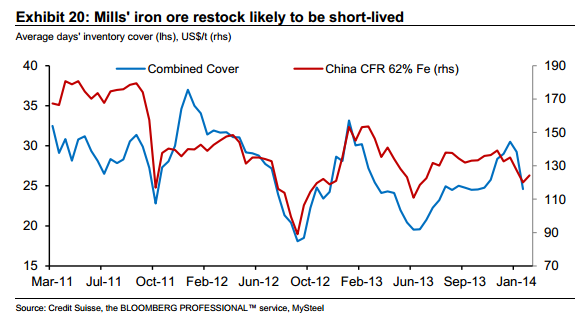

Here is the updated Chinese steel mill iron ore inventory data we’ve been sweating on and the news is good for iron ore producers in the short term. A decent destock has already taken place with days of cover down from 30 to 25. From Credit Suisse:

This should support short term demand as mills replenish these levels or at least maintain them as they go through their own ramp up of production for the first quarter steel inventory build.

However, as I’ve said previously, the ramp up of steel production is facing the combined headwinds of an overhang of 2013 over-production and a waning economy so mills may choose not to restock very far, if at all, and that will trigger further iron ore weakness. The huge port stockpile is another overhang in that event.

Given the destock has already started, a bit of risk analysis based on similar past episodes tells us downside price risks have improved from -$50 to roughly -$35 meaning any destock scenario could bottom around $90 for spot.

Although, if it does happen then I expect the rebound would not take us much past $120 before falling again. Each restocking episode in the past few years has exhibited a lower peak as mills become more confident of abundant supply. Add in little or no new demand growth and there’s no need to carry lot’s of stock to pressure margins.

Goldman’s $110 average price forecast for 2014 is shaping up nicely.