Expanding the goods and services tax to include food, education, health and financial products could cut this year’s budget deficit by 34 per cent and propel the Commonwealth’s finances back to surplus within four years.

Tax office revenues would be boosted by more than $16 billion this year alone and by a total of $70 billion through 2016-17…

…since its introduction by the Howard-Costello government 13 years ago, families are spending more on private education…

The Henry Tax Review showed that the GST is relatively efficient, since it is broadly applied, is difficult to avoid, and does not significantly distort behaviour (see next chart).

Broadening the GST would also share the tax burden with the growing share of people no longer in the workforce, so in this sense could help mitigate ageing’s effect on the Budget.

That said, there are obviously potentially negative equity effects from broadening the GST, since the burden of reform would fall most heavily on lower income earners. Moreover, as Deloitte’s Chris Richardson points out in the above AFR story, any expansion to health would be problematic, since “Governments already subsidise health by 70¢ in the dollar, so increasing the cost of health means you raise the cost to government. You’re creating a money round-robin.”

From a purist’s perspective, implementing a broad-based land tax would be a better reform (although obviously difficult to introduce). While not shown above, a broad-based land tax would have similar efficiency to the Petroleum Resource Rent Tax (PRRT) and Municipal rates, since it would be applied to a tax base that is completely immobile – land. In fact, the only loss in efficiency cause by land taxes would come from them being applied non-uniformly to different land users (as occurs with municipal rates), thereby distorting the pattern of land use.

A broad-based land tax would also have more favourable distributional impacts than the GST, and would effectively boost land supply and help make infrastructure investment self-financing for governments.

Regardless, with Australia’s population ageing and facing a Budget squeeze from lower receipts and higher aged-related spending, these reforms on their own would not go far enough.

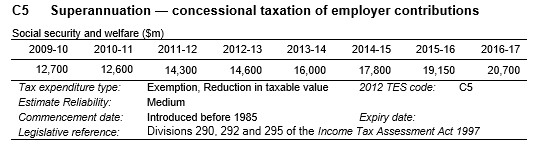

As argued repeatedly, a major failing of Australia’s retirement system is that it directs the lion’s share of superannuation tax concessions to higher income earners – i.e. precisely those whom are least likely to need the pension – instead of sharing concessions more evenly across the income distribution. According to the Treasury, superannuation concessions on employer contributions alone cost the Budget around $16 billion currently, which is expected to increase to nearly $21 billion by 2016-17 (see below table).

The Government could, therefore, make significant Budget savings by replacing the 15% flat tax on super contributions with an flat concession (say 15%), thereby: 1) providing all taxpayers with the same taxation concession and restoring progressiveness to the system; and 2) boosting lower income earners’ super savings and thus reducing their reliance on the aged pension.

Further, access to the pension is currently also distorted by not including the biggest asset most households own – their owner-occupied home – from the assets test. This results in a large number of wealthier households gaining access to taxpayer assistance when they are well placed to look after themselves.

With Australia’s population ageing fast, and the proportion of workers to non-workers set to decline significantly in the decades ahead, the Government will ultimately be forced to scale back entitlements as the tax base shrinks and/or look for new ways to raise taxes. And although there are many options, it is better to begin the reform process now rather than waiting until there is a Budget crisis.

Addendum:

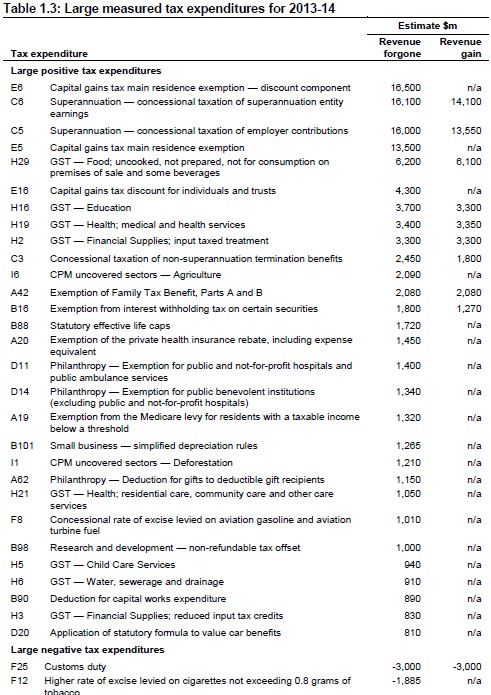

The below Treasury table shows tax concessions by component, which is dominated by capital gains tax (CGT) concessions on owner-occupied dwellings and superannuation concessions:

While I obviously support winding back superannuation concessions, I don’t support levying CGT on one’s principle place of residence, since it would have the same distorting impacts as stamp duties. Instead, a better approach would be to implement a broad-based land tax, for reasons outlined above (and in greater detail here).