Daryl Dixon, executive chairman of Dixon Advisory and author of Securing Your Superannuation Future, published a curious article in The Australian over the weekend lamenting the “unfairness” of Australia’s superannuation system under the former Labor Government, which purportedly unfairly penalised higher income earners:

THE previous government’s superannuation policy unfortunately was driven all too often by the hunt for revenue at the cost of basic principles of equity and fairness. Four glaring instances highlight gross inequities and inconsistencies in the decisions taken.

These are: the severe cut-back in the concessional contributions caps, even for older people with limited superannuation; the additional 15 per cent contributions tax surcharge on taxpayers with annual incomes of more than $300,000; the now abandoned 15 per cent tax on annual pension fund income above $100,000; and the penalty tax levied on excess contributions.

Remedial action on all of these decisions would simplify life for the Australian Taxation Office and help restore integrity to the tax system…

This is not an exhaustive catalogue of where change is needed, but these examples do highlight the scope for the new government to make our superannuation system much fairer.

What is extraordinary about Dixon’s article is that he has completely ignored the inherent design flaws in Australia’s retirement system, which have worked to make it both highly inequitable an unsustainable.

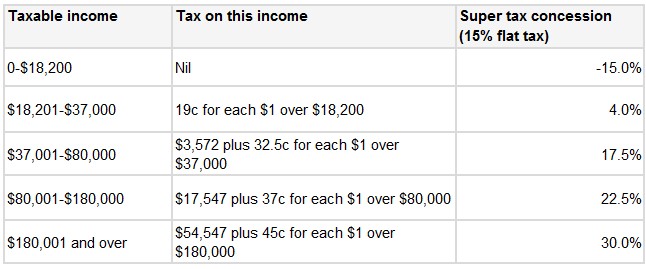

As explained last week, the former Labor Government’s reforms to superannuation were designed to improve the equity and sustainability of the system. Under this system, all employees that contribute compulsorily into super pay a flat 15% contributions tax, which effectively means that the amount of concessions received increases as one moves up the income scale (see below table).

For example, someone that earns in excess of $180,000 per year receives a 30% tax concession for each dollar that they contribute into super (i.e. 45% marginal tax rate less the 15% flat tax). At the other end of the scale, someone that earns less than $18,200 per year in effect gets penalised 15% for each dollar that they contribute into super.

The contributions caps and high income surcharges implemented by Labor, in addition to the recently cancelled Low Income Super Contribution (LISC) – a policy that refunds the 15% tax on super contributions for workers earning less than $37,000 a year – were designed to both limit the overall amount of superannuation concessions (thus improving the system’s sustainability) whilst also ensuring that concessions were shared more evenly across the income scale, rather than being captured primarily by those on the highest marginal tax rate (thus improving system equity).

Given that the main rationale behind superannuation is to both adequately provide for retirement and take pressure off the aged pension, the 15% flat tax system is inherently flawed and designed to fail. By providing massive taxation concessions to those on the highest incomes, the Budget loses billions of dollars of forgone revenue. At the same time, the super system is unlikely to relieve pressure on the aged pension, since those that are most likely to need it – lower and middle income earners – receive minimal (if any) concessions, which both hinders their ability to build-up a retirement nest egg and discourages them from making additional contributions.

A simple reform that would greatly improve the equity and sustainability of the system would be to axe the flat 15% tax on superannuation contributions in favour of a flat 15% concession. This would: 1) provide all taxpayers with the same taxation concession, thereby improving equity; 2) boost lower income earners’ super savings, thereby reducing reliance on the aged pension; and 3) reduce overall costs to the Federal Budget.

That said, the inherent flaws in Australia’s retirement system don’t end with the 15% flat tax. The exclusion of the family home from the assets test for the aged pension, combined with the ability to withdraw one’s super as a lump-sum (instead of an annuity), creates an incentive for households to borrow to purchase an expensive home in the lead-up to retirement, retire at 60, withdraw their super tax-free as a lump sum, use the money to pay-off their mortgage or to fund consumption, and then go on the aged pension from 65 years of age.

In such instances, the taxpayer is left wearing the cost of superannuation concessions throughout the individual’s working life, and then again once that same individual goes on the aged pension. It is a strategy that, while making sense for the individuals concerned, compromises the integrity, fairness and sustainability of the retirement system which, after all, was supposed to relieve pressure on the Budget, not exacerbate it.

It also highlights the need to begin taxing superannuation lump sums, whilst at the same time encouraging retirees to withdraw their savings as a annuity (instead of the pension), as well as including the family home in the assets test.

On the latter point, it is blatantly unfair and absurd that the biggest asset most households retiree with – the family home – is essentially excluded from their capacity to fund their retirement. It is then especially unfair to turn around and expect younger generations, who are already struggling under the weight of expensive housing and high mortgage debts (fostered onto them by their parents’ generation), to bare the full cost of their parents’ retirement.

unconventionaleconomist@hotmail.com