The Weekend AFR published an article on how the Federal Budget is facing a black hole caused primarily by falling wages growth, which is reducing the personal income tax take:

Wages growth has slowed to the weakest pace since the 2007 financial crisis, slashing the personal income tax take and blowing a further $2.5 billion hole in the federal budget.

The November financial statement, released on Friday by Finance Minister Mathias Cormann shows the deficit was $22.9 billion, almost $3 billion worse than expected.

Tax revenue was $6.02 billion lower than the budget prediction, primarily reflecting lower wages growth, company profitability and lower mining taxes…

The monthly figures show a shift in the budget pain from the slowing mining industry across the economy.

The figures show that the deterioration in the budget bottom line came almost entirely from a lower PAYG tax take on wages falling from $68.58 billion to $66.08 billion or $2.5 billion…

Treasurer Joe Hockey warned in a mid-year economic statement released in December that Australia could face budget deficits and rising debt for at least the next decade, blaming Labor for the budget blowout that will see the deficit balloon from $30 billion to $47.6 billion.

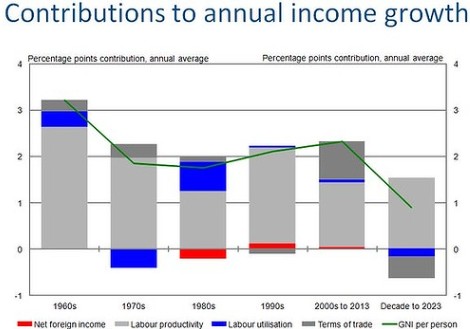

Unfortunately for the Federal Government, the outlook for wages growth remains poor, with the Australian Treasury late last year forecasting that average per capita income growth will halve over the next decade to the lowest rate of growth experienced in 50 years (see next chart).

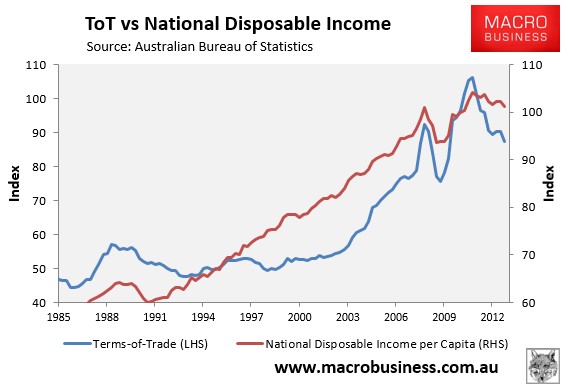

The national accounts data for the September quarter, released late last year by the ABS, also provided a harbinger of things to come, with real per capital national disposable income (NDI) sliding by 1.0% over the quarter and also by 1.0% over the year, pulled down by the falling the terms-of-trade (see next chart).

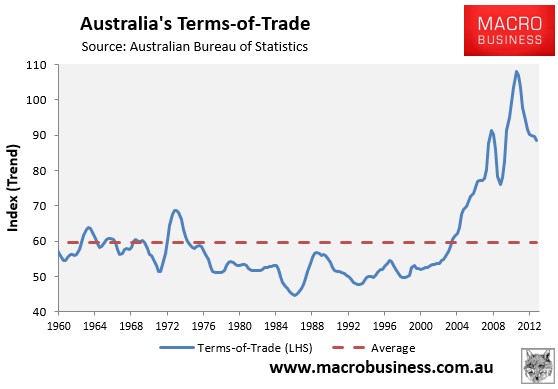

Looking ahead, household income growth will likely weaken further as the terms-of-trade continues to retrace back towards its longer-term average level (see next chart).

Indeed, the latest index of commodity prices, released by the RBA, revealed that commodity prices fell by 1.8% in Special Drawing Rights terms (essentially a measure of prices using a basket of currencies) over the December quarter, suggesting that the terms-of-trade will show another negative result when the year-end national accounts are released.

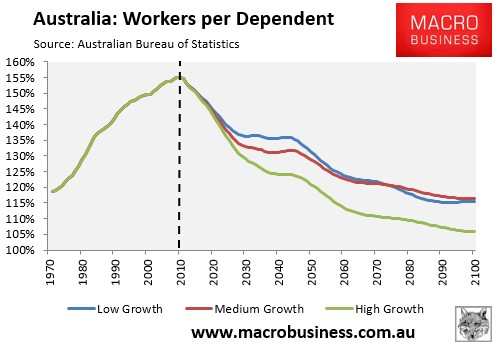

These headwinds will be exacerbated by the ageing of the population, which will result in a rising dependency ratio and a falling share of workers supporting non-workers, even under the ABS’ high population growth scenario (see next chart).

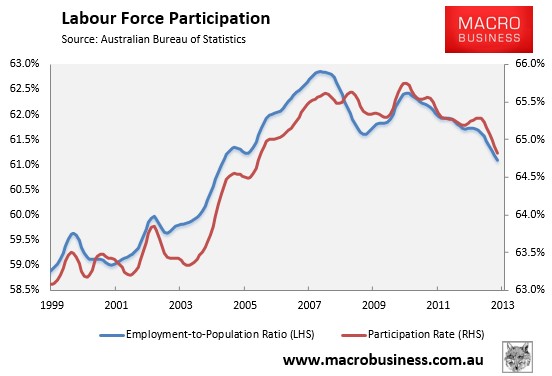

In turn, the labour force participation rate and the employment-to-population ratio is likely to continue trending lower (see next chart), lowering growth in both GDP and national income.

Lower income growth, brought about by these structural headwinds, are the new normal for the Australian economy. Contrary to Hockey’s claim, they have little to do with so-called Labor mis-management.

unconventionaleconomist@hotmail.com