Australians may need to accept real wage cuts or face the prospect that official interest rates have to rise to control inflation even as unemployment rises, business leaders and economists said…

Former Reserve Bank board member Donald McGauchie said the previously high dollar had masked the true rate of inflation over the past few years.

…a falling dollar would only help struggling industries such as manufacturing and tourism if matched by wage restraint…

“Real wages have to come down,” said JPMorgan Australia chief economist Stephen Walters. “If you’re a high-cost economy then real wages need to adjust downwards to regain competitiveness, or have a lower exchange rate, which doesn’t look to be going down”…

“Everyone has got to take a bit of pain here. The economy has to adjust – we’ve had 12 years of a terms-of-trade boom, income gains, house price rises – that all can’t be sustained indefinitely”…

Grattan Institute productivity program director Jim Minifie said with national income dropping because of the falling terms of trade, real wages growth should be lower.

“Otherwise you have a tendency to be inviting slowing labour demand and rising unemployment,” he said.

I agree with these sentiments. The fact remains that Australia’s non-mining economy has lost competitiveness, as evident by the raft of manufacturing closures (e.g. Ford, Holden, Electrolux, etc). In the absence of productivity growth, there are two ways for competitiveness to be restored:

- via a devaluation of the exchange rate, which raises the cost of imports and reduces the real purchasing power of Australian incomes; and/or

- wage rises below the rate of inflation.

It is also true that the ongoing decline of the terms-of-trade will drag on national income growth, pulling down incomes in the process.

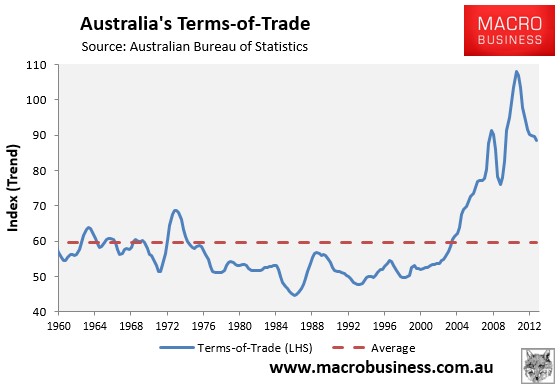

As explained previously, the explosion of commodity prices between 2003 and 2011 caused the terms-of-trade – essentially the price received for Australia’s exports divided by the price paid for imports – to surge to the highest level on record (see next chart).

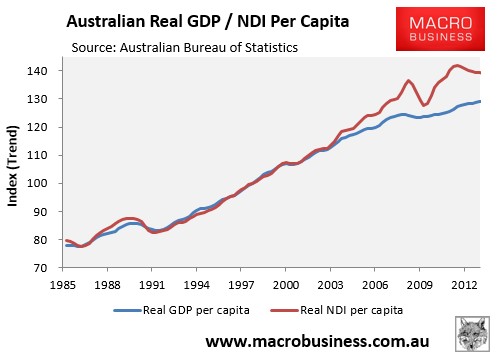

In turn, Australia received a large pay rise, since it could now buy more imports from a given level of exports. This pay-rise meant that Australia’s national disposable income (NDI) grew at a much faster rate than output, as measured by GDP, making Australians much wealthier (see next chart).

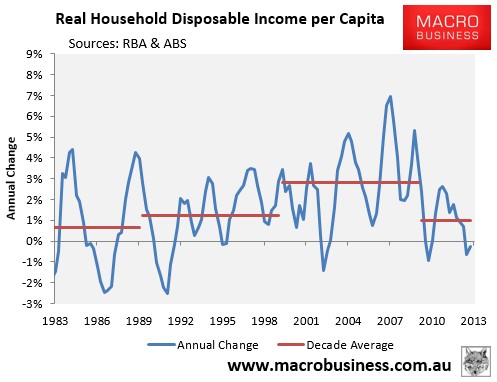

As shown below, this surge in NDI also flowed to Australian households. Real income growth remained relatively stagnant in the 1980s, grew solidly in the 1990s as microeconomic reforms boosted productivity, grew even more strongly over the 2000s as the terms-of-trade boost kicked-in, and have since slowed down over the past three-and-a-half years and the terms-of-trade has retraced:

Looking ahead, income growth will be much slower as the terms-of-trade continues to retrace towards its longer-term average level.

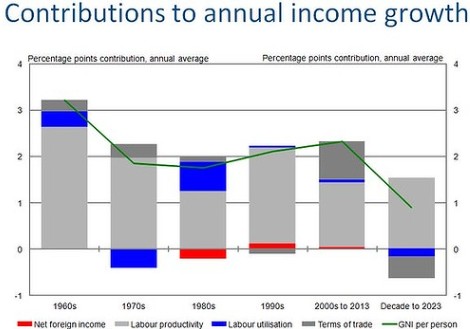

This assessment is supported in the next chart from the Australian Treasury, which estimates that around 40% of the growth in average incomes between 2000 and 2013 was caused by the one-off rise in Australia’s terms-of-trade. It also forecasts that average per capita income growth will halve over the next decade to the lowest rate of growth experienced in 50 year as the terms-of-tra:

In short, the strong real income gains experienced over the past decade were an aberration, juiced by the once-in-a-century surge in Australia’s terms-of-trade, and income growth going forward will be much lower.