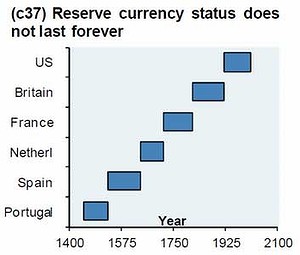

The World Bank’s former chief economist wants to replace the US dollar with a single global super-currency, saying it will create a more stable global financial system, China Daily reports:

‘‘The dominance of the greenback is the root cause of global financial and economic crises,” Justin Yifu Lin told Bruegel, a Brussels-based policy-research think tank. “The solution to this is to replace the national currency with a global currency.

Lin, now a professor at Peking University and a leading adviser to the Chinese government, said expanding the basket of major reserve currencies — the dollar, the euro, the Japanese yen and pound sterling — will not address the consequences of a financial crisis. Internationalising the Chinese currency was not the answer, either, he said.

“China can only play a supporting role in realising the plans,” Lin said. “The urgent thing is for the US and Europe to endorse these plans. And I think the G20 is an ideal platform to discuss the ideas,” he said, referring to the group of finance ministers and central bank governors from 20 major economies.

The concept of a global “super currency” tied to a basket of currencies has been periodically discussed by world leaders as well as endorsed by 2001 Nobel Memorial Prize-winner Joseph Stiglitz. A super currency could also be tied to a single currency, but the interconnectedness of world financial markets and concerns about the volatility that can occur as a result of the system being tied to one currency have made this idea less popular.

Actually, the idea originated with John Maynard Keynes and his notion of the “bancor” put forth at Bretton Woods but he was rolled by America. George Monbiot explains:

At the UN’s Bretton Woods conference in 1944, John Maynard Keynes put forward a much better idea. After it was thrown out, Geoffrey Crowther – then the editor of the Economist magazine – warned that “Lord Keynes was right … the world will bitterly regret the fact that his arguments were rejected.” But the world does not regret it, for almost everyone – the Economist included – has forgotten what he proposed.

One of the reasons for financial crises is the imbalance of trade between nations. Countries accumulate debt partly as a result of sustaining a trade deficit. They can easily become trapped in a vicious spiral: the bigger their debt, the harder it is to generate a trade surplus. International debt wrecks people’s development, trashes the environment and threatens the global system with periodic crises.

As Keynes recognised, there is not much the debtor nations can do. Only the countries that maintain a trade surplus have real agency, so it is they who must be obliged to change their policies. His solution was an ingenious system for persuading the creditor nations to spend their surplus money back into the economies of the debtor nations.

He proposed a global bank, which he called the International Clearing Union. The bank would issue its own currency – the bancor – which was exchangeable with national currencies at fixed rates of exchange. The bancor would become the unit of account between nations, which means it would be used to measure a country’s trade deficit or trade surplus.

Every country would have an overdraft facility in its bancor account at the International Clearing Union, equivalent to half the average value of its trade over a five-year period. To make the system work, the members of the union would need a powerful incentive to clear their bancor accounts by the end of the year: to end up with neither a trade deficit nor a trade surplus. But what would the incentive be?

Keynes proposed that any country racking up a large trade deficit (equating to more than half of its bancor overdraft allowance) would be charged interest on its account. It would also be obliged to reduce the value of its currency and to prevent the export of capital. But – and this was the key to his system – he insisted that the nations with a trade surplus would be subject to similar pressures. Any country with a bancor credit balance that was more than half the size of its overdraft facility would be charged interest, at a rate of 10%. It would also be obliged to increase the value of its currency and to permit the export of capital. If, by the end of the year, its credit balance exceeded the total value of its permitted overdraft, the surplus would be confiscated. The nations with a surplus would have a powerful incentive to get rid of it. In doing so, they would automatically clear other nations’ deficits.

When Keynes began to explain his idea, in papers published in 1942 and 1943, it detonated in the minds of all who read it. The British economist Lionel Robbins reported that “it would be difficult to exaggerate the electrifying effect on thought throughout the whole relevant apparatus of government … nothing so imaginative and so ambitious had ever been discussed”. Economists all over the world saw that Keynes had cracked it. As the Allies prepared for the Bretton Woods conference, Britain adopted Keynes’s solution as its official negotiating position.

But there was one country – at the time the world’s biggest creditor – in which his proposal was less welcome. The head of the American delegation at Bretton Woods, Harry Dexter White, responded to Keynes’s idea thus: “We have been perfectly adamant on that point. We have taken the position of absolutely no.” Instead he proposed an International Stabilisation Fund, which would place the entire burden of maintaining the balance of trade on the deficit nations. It would impose no limits on the surplus that successful exporters could accumulate. He also suggested an International Bank for Reconstruction and Development, which would provide capital for economic reconstruction after the war. White, backed by the financial clout of the US treasury, prevailed. The International Stabilisation Fund became the International Monetary Fund. The International Bank for Reconstruction and Development remains the principal lending arm of the World Bank.

David Llewellyn-Smith is Chief Strategist at the MB Fund and MB Super. David is the founding publisher and editor of MacroBusiness and was the founding publisher and global economy editor of The Diplomat, the Asia Pacific’s leading geo-politics and economics portal.

He is also a former gold trader and economic commentator at The Sydney Morning Herald, The Age, the ABC and Business Spectator. He is the co-author of The Great Crash of 2008 with Ross Garnaut and was the editor of the second Garnaut Climate Change Review.