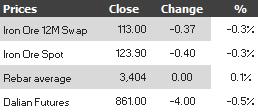

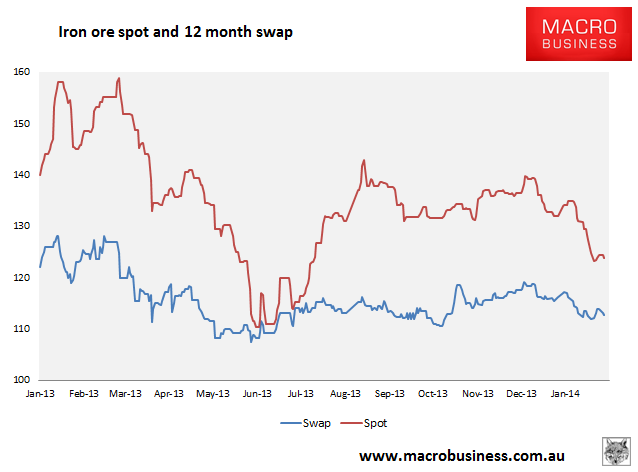

Find below the iron ore charts for January 28, 2014:

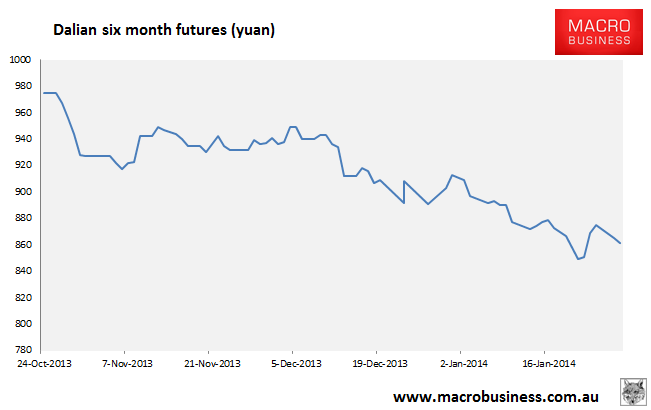

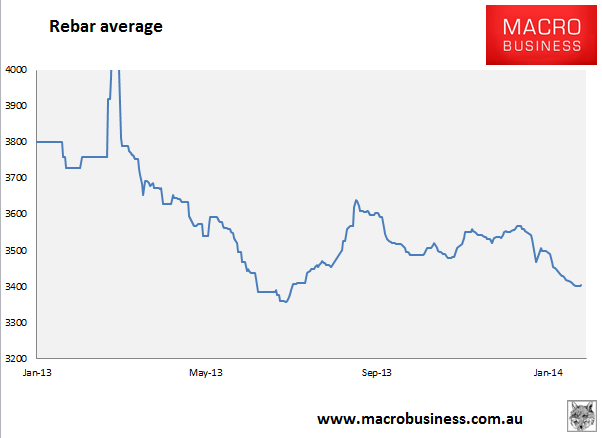

Rebar futures fell towards recent lows.

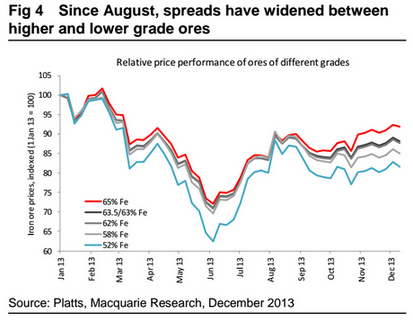

In news, I reported last year a new argument doing the rounds that could help support premium iron ore prices. The FT discovers it today:

Will seaborne supply growth overwhelm Chinese steel production? Or will it manage to keep pace?

These have been key questions facing the iron ore market over the past couple of years. But the story in 2014 has several added levels of complexity. One is Beijing’s war on pollution.

Mills in China’s key steel making provinces of Hebei and Jiangsu are under pressure to lower emissions and comply with new air pollution standards following smog crises last year in several major cities.

As a result, they are buying higher-quality ore, known in the industry as lump, that can be loaded directly into blast furnaces without the need for sintering, a dirty process that is a major source of pollution and sulphur dioxide.

Premiums for lump over the miners’ regular product, fines, are increasing as tougher environmental standards force Chinese steelmakers to use a different mix of raw materials in their furnaces. The same is also true for iron ore pellets.

The price of Australia lump, as assessed by Metal Bulletin, is fetching a premium of between $17 and $18.6 a tonne over fines with 62 per cent iron content – the benchmark iron ore price for financial markets. Six months ago the premium was at $8 a tonne, while pellets with 65 per cent iron ore content are trading at a premium of $40-$42 a tonne to fines, up $10 in the same period.

That is good news for several major mining companies, including BHP Billiton, Rio Tinto and Vale, which are among the top suppliers of high-grade ores.

Here’s the chart from my earlier piece:

I’m under the impression that premium lump is a minority percentage of Rio and BHP output but if someone can clarify I’m all ears.