Welcome to 2014! It’s good to be back.

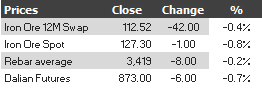

Find below the iron ore price table for January 17, 2014:

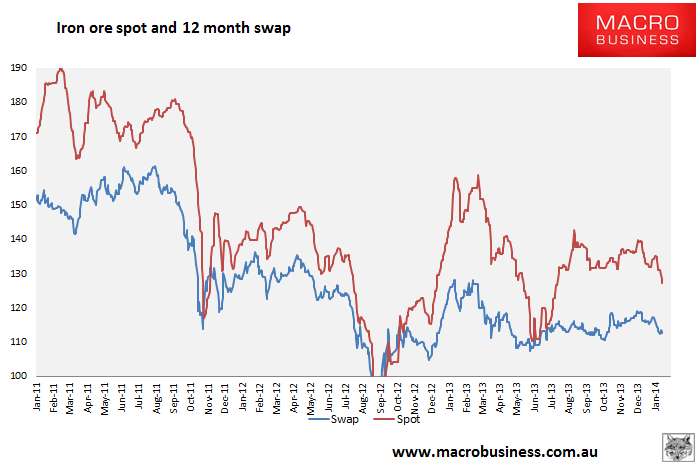

The charts. 12 month swap has broken down but is not yet terribly bearish technically. On the other hand, spot has broken support at $131 and has no obvious support until $110:

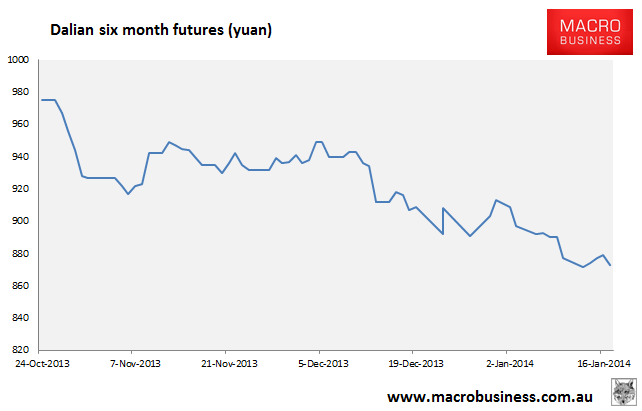

Dalian six month futures are sliding relentlessly, now pricing around $117 in six months, which is consistent with 12 month OREX at $112:

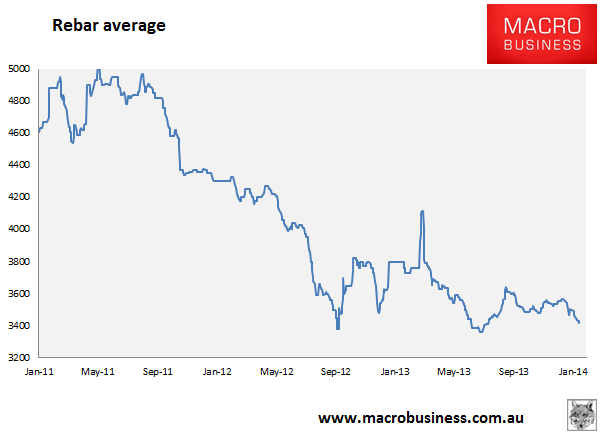

Rebar average is also sliding and is stuck in a deeply unprofitable range for steel mills illustrating serious overcapacity:

Let’s get straight to it. Iron ore is in trouble again. The question is how much trouble? Are we seeing the leading edge of the big price falls long expected on the great supply deluge? Or are we seeing just another Chinese inventory cycle?

My answer is both. The remarkable story of last year’s iron ore strength around an average of $130 was impressive. But one should always recall the long term. Reversing the perspective, despite Chinese steel production jumping a spectacular 9% last year, iron ore is still down $50 from its 2011 highs. This says to me that we are long passed the leading edge of the structural iron ore correction. Cyclical forces look increasingly high risk as well.

Entering 2014, on the structural front, there are two major facts to consider. The first is Chinese steel demand. As diagnosed through the second half of last year, the present round of Chinese growth is not a sustainable private sector growth cycle. Rather it is a lurching sequence of stimulus and tightening measures as imbalances vie with economic mandarins for control of the economy.

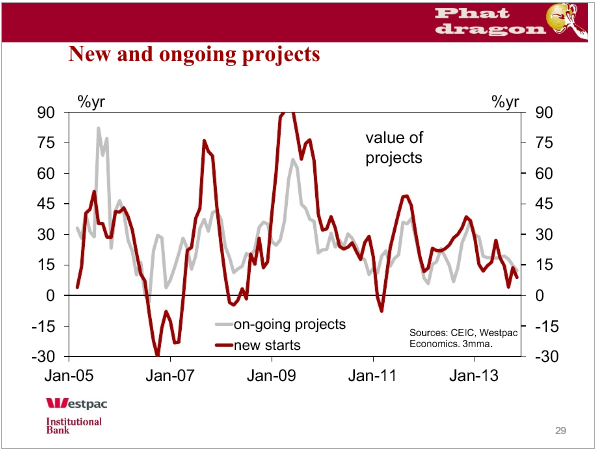

The two trillion yuan stimulus package that rescued growth for much of last year is easing. The infrastructure pipeline is emptying:

The strong surge in real estate sales last year is also abating as various monetary and fiscal nips and tucks add up, though we may see a decent follow through this year in housing starts.

But, basically, the billion dollar question for this year’s steel outlook is: will China’s planned rebalancing be allowed to proceed or will the temptation to kick the can with more stimulus prove irresistible once more? The realists will say ‘inevitably’. And in that event, iron ore will have a better time in the second half of this year than the first is shaping up to be.

The other structural consideration for iron ore is the degree of supply capacity coming online in the next six months. Versus last year, another 100 million tonnes of capacity will be in operation by mid year via completions at BHP’s Jimblebar, Rio’s Pilbara 290 and Fortescue’s Kings expansion.

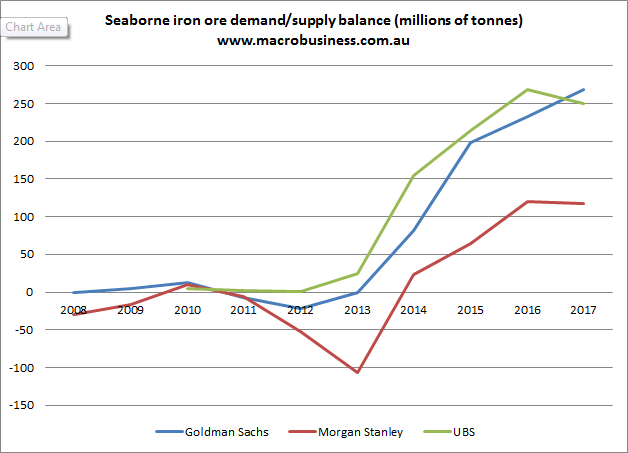

It’s worth revisiting the old supply and demand chart:

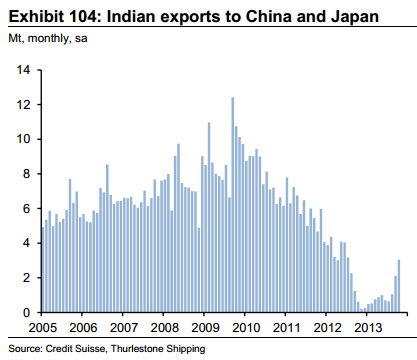

India is also beginning to return, if only slowly. From Credit Suisse:

Moreover, Rio’s plans to move forward on Pilbara 360 will see supply continue to ramp up (it could bring another 30-40 million tonnes to market by year end). God help us, Roy Hill appears to be going ahead as well, with a completion date next year for another 55 million tonnes, though that is very aggressive. Vale also starts to deliver its expansions next year.

There are two mitigating factors. The first is high cost Chinese supply will be displaced in the shakeout. But the process is certain to be more slow and irrational than markets expect, just as it has been in the two coals. The second mitigating factor is the market power of the Pilbara cartel, which is substantial. But with each passing year more supply and suppliers weakens the major Australian suppliers price making power.

In terms of market structure, then, supply is upon us and will keep coming and the growth drivers of Chinese steel demand are sputtering. I expect long term global demand for seaborne iron ore to keep growing in the low single digits as the global recovery grinds along. But as the consumer of 60% of global iron ore, the critical question is Chinese demand. If the communists stimulate again (delaying rebalancing) we can expect an iron ore average price somewhere between $110-$120 this year. If they do not then knock $20 off.

There are also very clear reasons to be bearish in terms of the near term Chinese stock cycle. Chinese steel mills have largely rebuilt their inventory of imported ore after the two huge rundowns of the past eighteen months. Also from Credit Suisse:

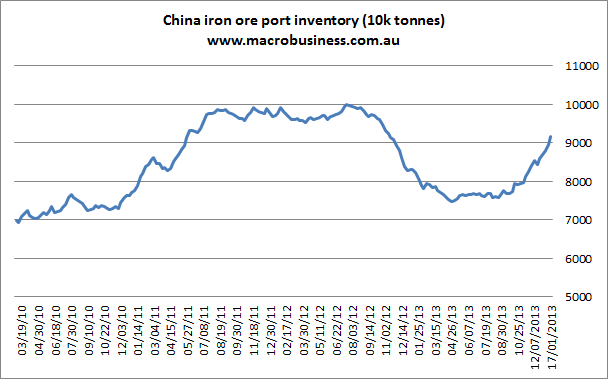

Port inventories are not a direct proxy for demand but do indicate something about the fullness or otherwise of the Chinese iron ore supply chain and the great pile of 2012 has also been significantly rebuilt at 91.6 million tonnes this week:

We remain below previous highs but it’s still an impressive hoard.

In short, we are not far short of the same cyclical surplus of iron ore inventories in China that existed prior to the crash of 2012, and we are facing a similar (if slower moving) emerging crunch in demand.

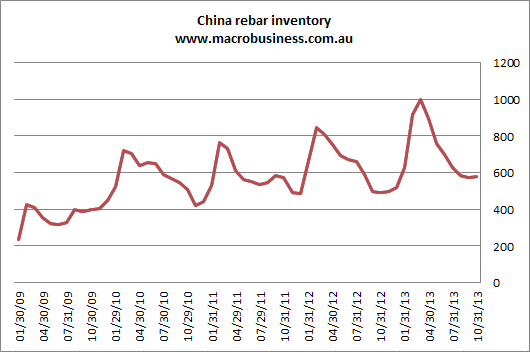

Cyclical factors should keep these bearish settings at bay for a little while. The first quarter is typically a very strong one for iron ore and steel. Mills build a up big inventory of steel as demand slows in the winter and then run it down over the course of the year. Here is the Chinese rebar inventory cycle courtesy of Bloomberg:

As well, the cyclone season means mills rebuild their iron ore stockpiles in Q4 and hold high inventories throughout the season. As we’ve already seen, weather threats boost prices. However, given the slowing economy and depleting infrastructure pipeline, I would not be surprised to see this year’s steel inventory rebuild to be smaller than last year’s, which would be something of a trend break, as you can see.

That the iron ore price is falling at all through this period is quite bearish. There is also the problem that with rebar prices well off the highs of last year, many steel mills are once again losing money. In the past this has triggered iron ore inventory rundowns, which would run counter to, or could overwhelm, the seasonal strength.

As I warned in the later months of last year, whether Q1’14 will be dominated by a typical spurt of iron ore demand as China moves past its new year holiday at the end of January or the current steel price squeeze triggers a deeper inventory rundown is really beside the point. For anyone with a horizon beyond the next few months, the developing settings in the iron ore market are very clearly price bearish. The average price for the miracle commodity is going to fall materially this year and I would go so far as to say that as the market oscillates downwards it will threaten 2012 lows at some point.

It is a simple truth that without further Chinese stimulus, there is an uncomfortable probability that price falls will be deep enough to cause serious dyspepsia for both high cost producers and the Australian economy this year.