VOX has published an interesting study challenging the common view that house price appreciation is generally good for an economy, via their positive effect on borrowing and the ‘wealth effect’. Instead, the authors have found that the impacts on the real economy from house price appreciation can often be deleterious, since it tends to ‘crowd-out’ commercial and industrial lending via higher interest rates:

Looking at the period from 1988 to 2006, we find that firms that borrowed from banks located in stronger housing markets paid higher interest rates, received lower loan amounts, and ultimately invested less compared to similar firms that borrowed from banks located in weaker housing markets.

The normative implications for the economy are significant – if monetary policymakers are actively supporting one sector of the economy, such as the housing market, they are causing a detrimental effect for other productive sectors…

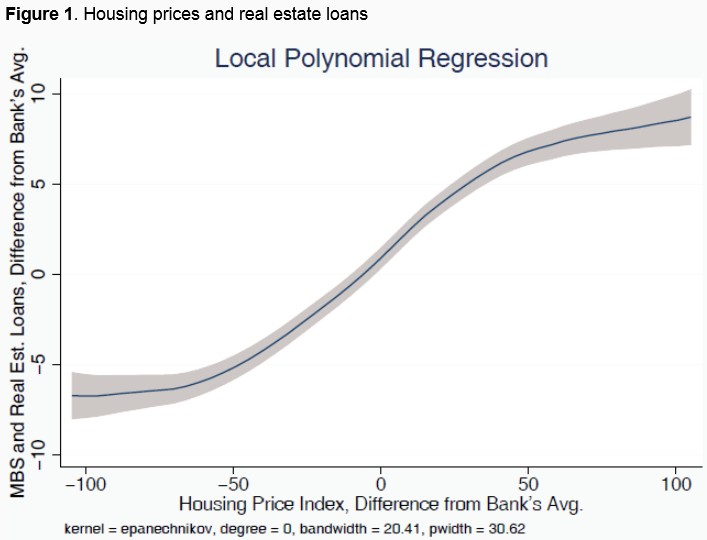

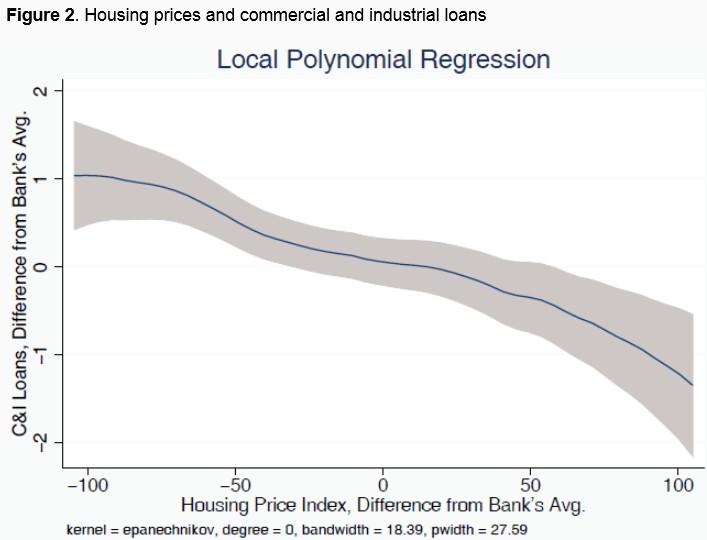

Figures 1 and 2 show the relationships between bank assets and housing prices. Figure 1 shows that as housing prices increase, banks on average invest more in real estate-related loans. However, Figure 2 shows that as housing prices increase, banks on average reduce their commercial and industrial loan portfolios as a percentage of assets. It appears that in reaction to housing-price appreciations, banks increase real estate lending and decrease commercial lending.

This decrease in commercial lending is interesting if it is caused by a reduction in the supply of capital, as opposed to a reduction in firms’ demand for capital. We estimate that a one standard-deviation increase in housing prices (about $79,700 in year 2000 dollars) that a bank is exposed to decreases investment by firms related to that bank by almost 6.3 percentage points, which is approximately 12% of a standard deviation for firm investment. Banks also increase the interest rate charged by 9 basis points, reduce outstanding loans by approximately 9%, and reduce loan size by approximately 4.5%. These results are consistent with banks reducing the supply of capital to firms in response to increased housing prices…

Digging deeper, we find that the negative investment effect is stronger for firms that borrow from smaller, more regional banks, and for firms that have limited sources of external financing (e.g. no access to bond markets).

…it is incorrect to assume that an expanding balance sheet leads to positive spillover effects across all sectors of the economy. There is a crowding out effect in which banks divert resources across sectors – in the case studied in our paper, rising real-estate prices lead banks to cut commercial loans and increase real-estate loans.

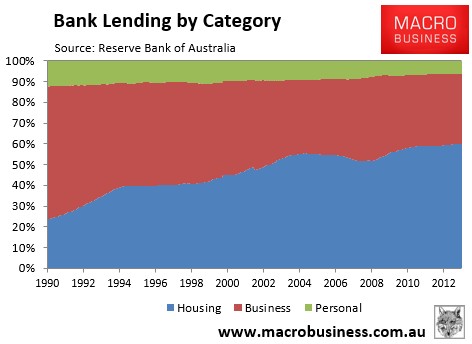

Certainly, similar factors seem to be in play in Australia. As shown by the next chart, the proportion of bank loans to businesses have roughly halved over the past 23 years just as loans for housing have more than doubled:

Advertisement

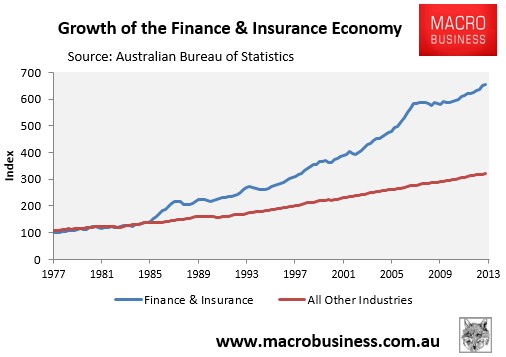

At the same time, yesterday’s national accounts data for the September quarter, released by the Australian Bureau of Statistics (ABS), showed the finance and insurance sector – the part of the economy most exposed to housing – continuing to grow at a faster rate than the overall economy, with the sector also doubling in size relative to the rest of the economy since deregulation, suggesting some ‘crowding-out effect’ (see next chart).

Advertisement

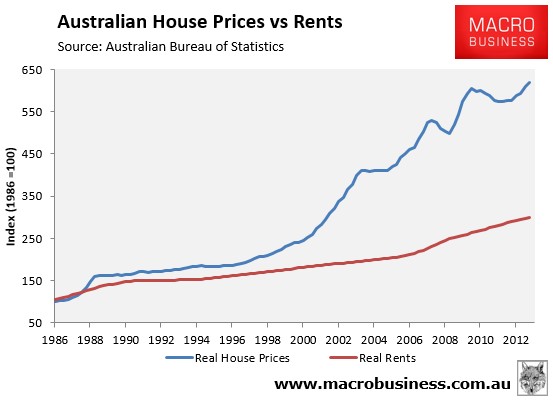

It is also no coincidence that Australian house prices decoupled from rents at roughly the same time as the finance and insurance sector’s growth decoupled from the rest of the economy, as the deregulation of the financial sector ignited credit growth, most of which has been channeled into housing (see next chart).

Like Frankenstein’s monster, it would appear that the financial sector, which once acted merely as an enabler of the productive economy, is now pulling its master’s strings.

Leith van Onselen is Chief Economist at the MB Fund and MB Super. He is also a co-founder of MacroBusiness.

Leith has previously worked at the Australian Treasury, Victorian Treasury and Goldman Sachs.